Key Stats for Salesforce Stock

- Past-Week Performance: +3.7%

- 52-Week Range: $174.6 to $296.1

- Current Price: $202.1

What Happened?

Salesforce (CRM), the world’s largest customer relationship management (CRM) software platform, closed its record fiscal 2026 with $41.5B in revenue and a total contract backlog of $72.4B, yet its stock sits at $202 (more than 30% below its 52-week high of $296.05) as Wall Street wrestles with whether its fast-scaling AI agent platform, Agentforce, can reignite durable growth before the broader software sector rout deepens further.

On February 25, CEO Marc Benioff reported Q4 revenue of $11.2B, up 12% year over year, and raised the fiscal 2030 revenue target to $63B, while simultaneously authorizing a $50B share repurchase program and lifting the quarterly dividend to $0.44 per share, a 5.8% increase payable April 23.

Agentforce, Salesforce’s autonomous AI agent platform that lets businesses automate sales, service, and operations without human intervention, surpassed $800M in annual recurring revenue, up 169% year over year, with 29,000 deals closed since launch and production deployments rising nearly 50% quarter over quarter, outpacing every disclosed AI monetization milestone the company has previously reported.

Adding a confirmed strategic layer, Salesforce on February 26 announced more than 180 organizations have adopted Agentforce IT Service in just four months since its October 2025 launch, displacing legacy IT service management providers including ServiceNow at customers such as Sunrun, CoolSys, and Cornerstone, while on March 3 the company extended its multi-year Formula 1 partnership to deploy a fan companion agent reaching 827M global fans.

Chief Financial Officer Robin Washington stated on the Q4 FY2026 earnings call that “our performance makes us even more confident in our path to reaccelerate organic revenue growth in H2 FY27,” a statement anchored by net new annual order value growth outpacing renewal order value in the second half of FY26 for the first time, and by 120 Agentic Enterprise License Agreements closed in Q4 alone.

With FY27 revenue guidance of $45.8B to $46.2B, a $50B buyback authorization representing roughly 25% of current market cap, and Agentforce and Data 360 combined ARR already at $2.9B and climbing, Salesforce is positioning the convergence of its AI agent layer, its proprietary data platform, and its Slack collaboration network as a compounding growth engine targeting $63B in revenue by fiscal 2030.

Wall Street’s Take on CRM Stock

The record $41.5B in FY26 revenue and $72.4B total contract backlog, combined with Agentforce’s 169% ARR growth, confirm that Salesforce’s AI transition is no longer a promise but a measurable revenue engine already reshaping forward estimates.

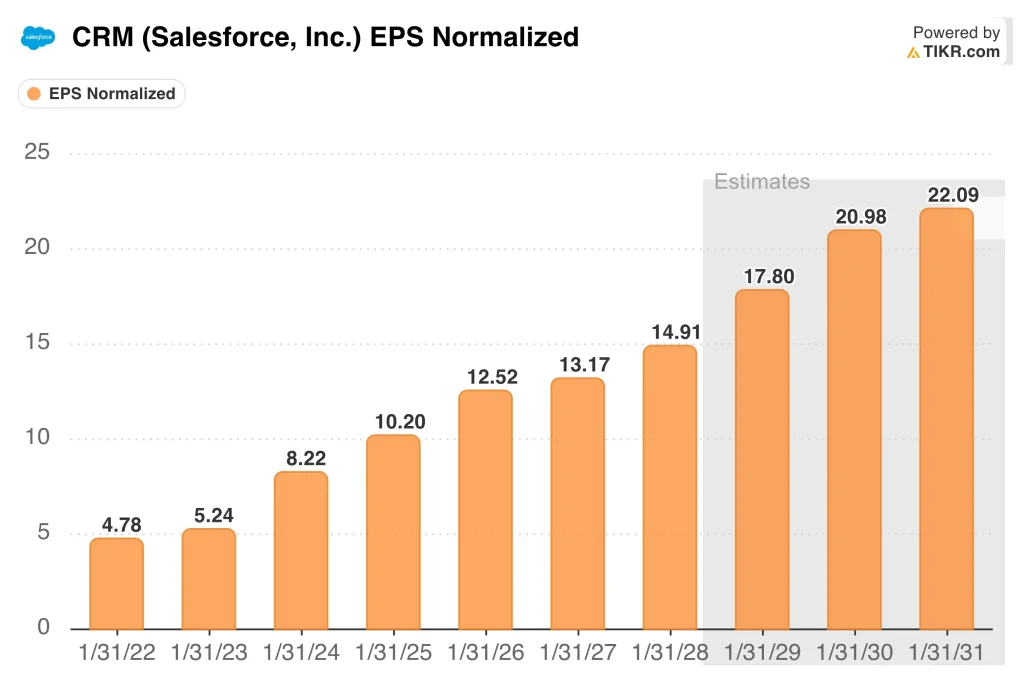

Normalized EPS reached $12.52 in FY26, up 22.7% year over year, accelerating from 24.1% growth the prior year, while EBITDA margins expanded to 38.8% from 37.8%, proving that AI investment is not compressing profitability.

Of the 53 analysts covering CRM as of March 6, 34 rate it a Buy, 7 Outperform, and 11 Hold, with a mean price target of $276.36 implying 37% upside from the current $202.11 price against a 52-week high of $296.05.

The analyst target range spans $190 on the low end to $475 on the high end, where the bear case hinges on Agentforce monetization stalling and continued weakness in Marketing, Commerce, and Tableau, while the bull case prices in the full H2 FY27 organic revenue re-acceleration already guided by management.

What Does the Valuation Model Say?

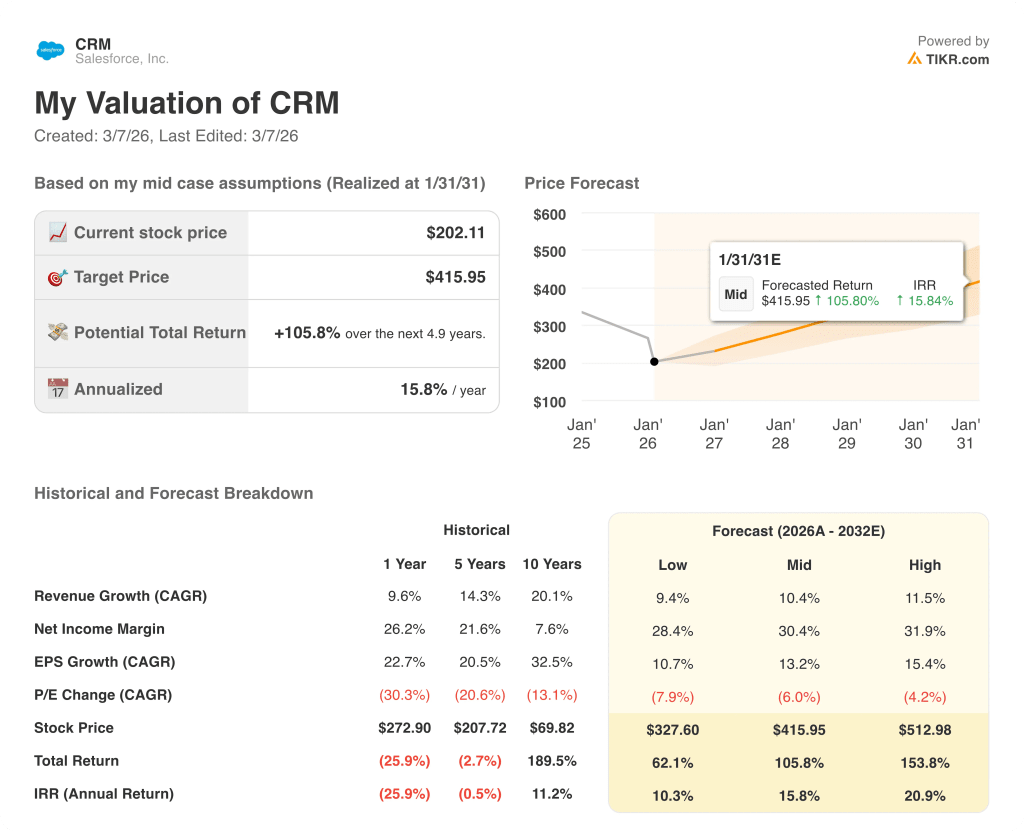

The TIKR mid-case valuation model prices CRM at $415.95 per share by January 2031, implying a 105.8% total return and a 15.8% annualized IRR, driven by a 10.4% revenue CAGR and net income margins expanding to 30.4% as Agentforce consumption scales and token costs commoditize.

The market is treating CRM as a legacy SaaS name caught in a sector rout, yet 29,000 Agentforce deals closed and $2.9B in combined Agentforce and Data 360 ARR signal a fundamentally different business than existed 18 months ago.

At $202.11, CRM trades at a 37% discount to the analyst mean target while generating $14.4B in free cash flow annually and deploying a $50B buyback authorization that management explicitly called an investment in “some low prices.”

The one signal to watch is whether net new annual order value continues to outpace renewal order value in Q1 FY27, the specific metric management tied directly to the H2 revenue re-acceleration thesis confirmed on the February 25 earnings call.

Persistent weakness in Marketing, Commerce, and Tableau, which management flagged as ongoing offsets to Agentforce strength, could delay the H2 FY27 re-acceleration and suppress the multiple re-rating the $276.36 mean analyst target already prices in.

The Q1 FY27 earnings release, with cRPO growth guided at approximately 14% year over year, will either validate or challenge the organic acceleration thesis that 34 Buy-rated analysts are already pricing into a $276.36 mean target.

Salesforce is a $41.5B revenue compounder with $14.4B in annual free cash flow, 169% Agentforce ARR growth, and a $50B buyback authorization trading 32% below its 52-week high.

Watch the H2 FY27 organic revenue inflection.

Should You Invest in Salesforce, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Salesforce, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CRM stock on TIKR for Free →