Key Stats for Lululemon Stock

- Past-Week Performance: -8%

- 52-Week Range: $159.3 to $348.5

- Current Price: $170.1

What Happened?

What was once the undisputed premium athletic apparel category leader, Lululemon, now trades at $170.13, more than 50% below its 52-week high of $348.50, as a U.S. sales slump, a CEO departure, a proxy fight, and a $320 million tariff headwind converge ahead of March 17 earnings.

On December 11, founder Chip Wilson escalated a boardroom proxy battle by calling for more than three director replacements, while lululemon simultaneously guided Q4 EPS of $4.66 to $4.76 against $6.14 a year ago, a 23% collapse driven by 410 basis points of combined tariff and de minimis headwind.

China Mainland revenue surged 46% in Q3 and the international business now grows at nearly 20% in constant currency, but that momentum cannot yet offset a U.S. segment posting negative 3% comps while rivals Alo Yoga and Vuori visibly take share from the brand’s core younger and affluent customer base.

On March 3, lululemon launched ShowZero, a new yarn-based sweat-concealing fabric technology developed with tennis ambassador Frances Tiafoe for his BNP Paribas Open kit, providing the first tangible evidence of the product innovation pipeline management has promised since Calvin McDonald’s January 31 departure.

With $1.6 billion in buyback capacity, a CEO search underway targeting a leader with growth and transformation experience, a three-pillar product reset targeting 35% new style penetration by spring, and Q4 earnings confirmed for March 17, lululemon enters its most consequential quarter in years with the turnaround thesis entirely unproven.

Wall Street’s Take on LULU Stock

The March 17 Q4 earnings release is now the single most consequential near-term event for LULU, as it will provide the first read on whether the three-pillar product reset is actually moving U.S. comparable sales back toward positive territory.

FY2026 estimates show revenue growing just 4.3% to $11 billion while EBITDA margins compress from 27.9% to 24.4%, confirming the Street has already priced in a difficult transition year before any product cycle recovery takes hold.

EPS normalized is expected to fall from $14.64 in FY2025 to $13.04 in FY2026, a 10.9% decline, making this the first back-to-back year of EPS contraction lululemon has posted since going public, which explains the $1.6 billion buyback authorization management deployed as a confidence signal.

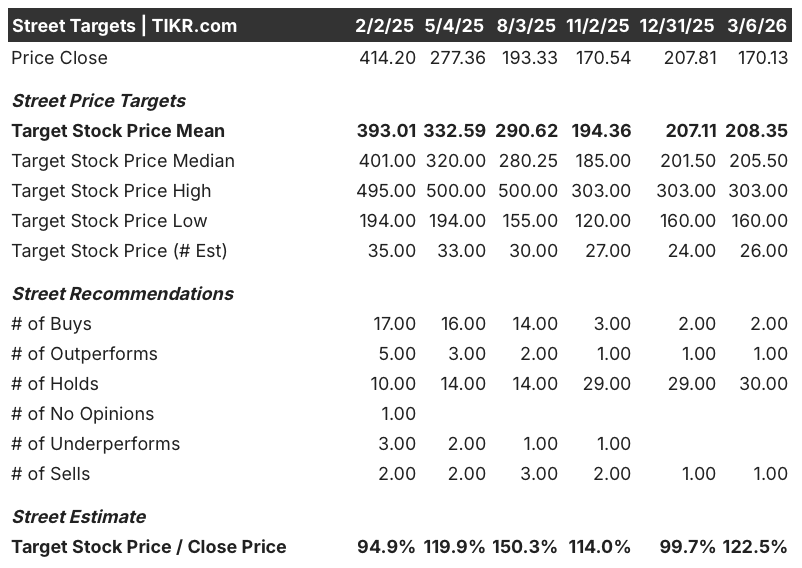

Wall Street has turned decisively cautious, with just 2 buys, 1 outperform, 30 holds, and 1 sell among 34 analysts, yet the mean price target of $208.35 still implies 22.5% upside from the current $170.13, suggesting the base case is a muddling recovery rather than a structural breakdown.

The $160 low target and $303 high target reflect a binary setup: bears anchor to the proxy fight disruption and continued U.S. share losses to Alo Yoga and Vuori, while bulls price in the spring 2026 product reset hitting 35% new style penetration and China Mainland sustaining 20%-plus growth.

What Does the Valuation Model Say?

TIKR’s mid-case fair value of $224.06 implies 31.7% total return over 3.9 years at a 7.3% annualized IRR, built on a modest 4.6% revenue CAGR and a net income margin recovery from 14.1% back to 12.7% through 2030.

The model assumes 12.5% annual P/E compression through 2030, meaning the entire return depends on EPS growing faster than the multiple shrinks — a tight margin for error if the U.S. turnaround stalls beyond FY2026.

The market prices lululemon as a structurally impaired brand, but China Mainland at 46% growth and international at nearly 20% constant currency confirm the platform remains globally intact and underpenetrated.

The $1.6 billion buyback capacity against a $170 stock, combined with $1 billion in cash and zero debt, signals management views the current price as a dislocation rather than a new baseline for the business.

The proxy fight is the risk that derails the timeline: a contested board at the March 2026 annual meeting would freeze strategic decision-making precisely when the new CEO search and product reset require unified leadership and speed.

March 17 Q4 earnings is the catalyst to watch — specifically U.S. comparable sales direction and any Q1 FY2026 gross margin guidance, which will confirm whether the tariff mitigation progress management cited is actually showing up in the numbers.

Should You Invest in Lululemon Athletica Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LULU stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lululemon Athletica Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LULU stock on TIKR for Free →