Samsara Inc. (NYSE: IOT) trades near $38/share, down over the past year as growth stocks broadly reset. Even with the pullback, Samsara continues gaining traction in connected operations software, supported by strong gross margins and a rapidly expanding customer base.

Recently, Samsara reported solid momentum in large enterprise wins and growing multi-product adoption, with more customers using its safety, telematics, and workflow automation tools together. The company also noted continued strength in its recurring revenue model, which remains a key advantage as customers integrate Samsara more deeply across their operations. These developments show the business remains resilient despite share price volatility.

This article explores where analysts believe the stock could trade by 2028. We have pulled together consensus price targets and valuation models to outline Samsara’s potential path. These estimates reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

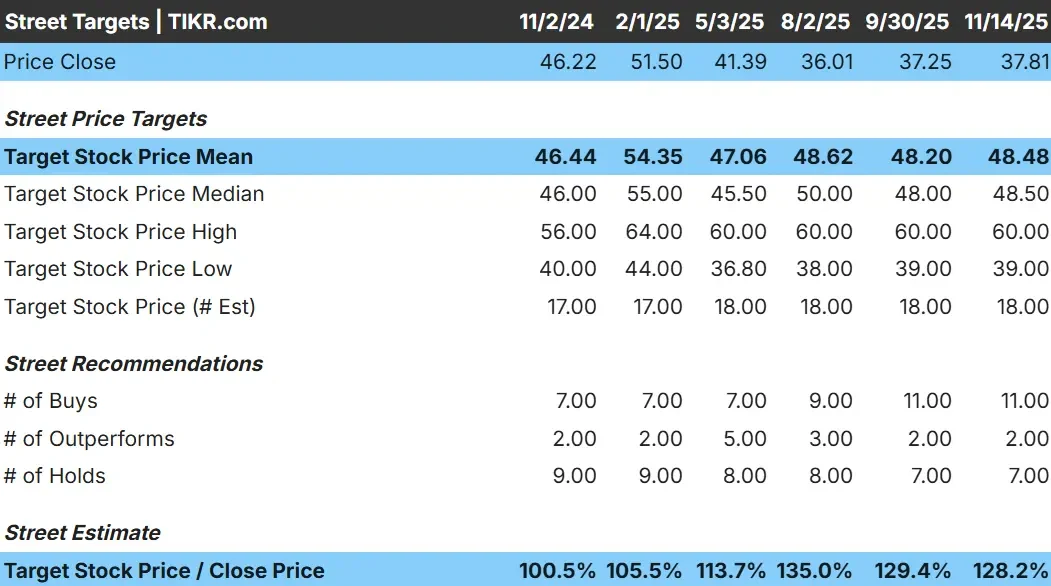

Samsara trades near $38/share today. The latest analyst price targets point to a mean estimate of $48/share, suggesting meaningful upside of more than 25% from current levels. Forecasts show a broad range, reflecting differing views on how quickly the company can scale.

- High estimate: $60/share

- Low estimate: $39/share

- Median target: $49/share

- Ratings: 11 Buys, 2 Outperforms, 7 Holds

Analysts are generally optimistic, but the spread between targets shows that conviction varies. For investors, this means the stock may respond strongly to quarterly updates, especially around customer additions and progress on profitability.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Samsara: Growth Outlook and Valuation

The company’s fundamentals appear strong based on the inputs shown in the valuation model:

- Revenue growth forecast: 22.5%

- Operating margins: 16.3%

- Shares trade at a 74.6x forward P E

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 74.6x forward P E suggests $60/share by 2028

- That implies about 59% upside, or roughly 23% annualized returns

These figures highlight Samsara’s solid recurring revenue base and high gross margin structure, which support its potential to compound over time. While the valuation is elevated, analysts expect continued growth and steady margin improvement to help justify the premium.

For investors, Samsara represents a fast-growing platform with the potential for meaningful long-term returns, provided the company continues executing well and scaling profitability.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Samsara is benefiting from rising demand for connected operations technology. Large organizations are adopting more modules across the platform, using Samsara for fleet management, safety insights, equipment monitoring, and workflow automation. This deeper integration strengthens customer retention and expands the company’s overall revenue base.

The platform continues to evolve with new features, automation tools, and analytics that help customers lower costs and improve operational efficiency. For investors, these strengths suggest the company is building a durable long-term growth engine supported by consistent product innovation and expanding customer usage.

Bear Case: Profitability and Valuation Risk

Despite strong momentum, Samsara still has risks. The company is early in its profitability journey, and the stock trades at a premium valuation that relies on sustained high growth. Any slowdown in customer additions or softer enterprise spending could pressure the share price.

Competition is also increasing as traditional telematics providers and newer software entrants invest heavily in similar capabilities. If Samsara cannot maintain its pace of innovation or customer expansion, revenue growth could moderate. For investors, these challenges mean the stock has limited margin for error.

Outlook for 2028: What Could Samsara Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Samsara could trade near $60/share by 2028. That would represent about 59% upside from today’s price and roughly 23% annualized returns.

This outlook assumes Samsara can maintain revenue growth above 20%, expand margins, and continue deepening adoption across large enterprise customers. While these expectations are achievable, they already reflect steady execution.

For investors, Samsara offers an appealing long-term story driven by recurring revenue, expanding product usage, and strong customer engagement. The potential for meaningful outperformance is there, but it depends on the company sustaining its growth momentum and improving profitability over time.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>