Okta Inc. (NASDAQ: OKTA) has been on a volatile ride. The stock now trades near $92/share, down from a 52-week high of $128. Slowing revenue growth, heavy competition, and past execution missteps have weighed on performance. At the same time, improving profitability, strong gross margins, and rising demand for identity security are giving investors reasons to stay interested.

Recently, Okta has doubled down on product innovation and expansion. At its 2025 Oktane conference, the company introduced a new Identity Security Fabric and unveiled Cross App Access (XAA), an open protocol designed to manage agent-to-app and app-to-app connections. It also announced the acquisition of Axiom Security for about $100 million, a move that strengthens Okta’s Privileged Access Management (PAM) tools to secure high-risk credentials across cloud, SaaS, and database environments. These investments highlight Okta’s push to expand its platform in the age of AI and defend its leadership in enterprise identity management.

This article explores where Wall Street analysts think Okta could trade by 2028. We have pulled together consensus targets, growth forecasts, and valuation models to get a sense of the stock’s possible trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Moderate Upside

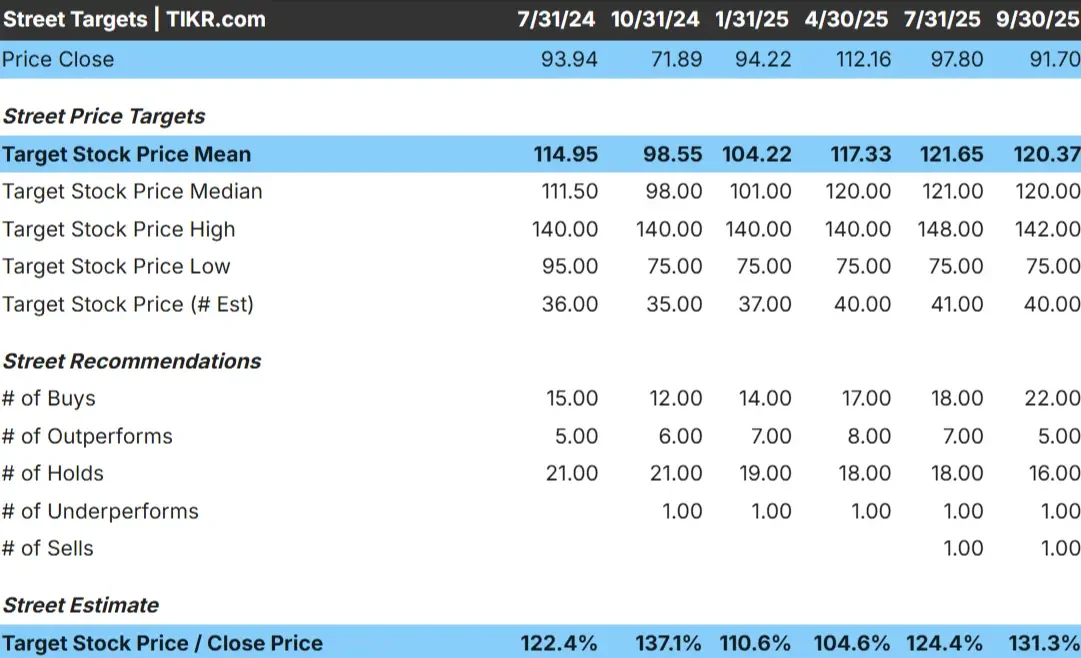

Okta trades at about $92/share today. The average analyst price target is $120/share, which points to roughly 31% upside. Forecasts vary widely, showing just how split analysts are on the company’s future:

- High estimate: ~$142/share

- Low estimate: ~$75/share

- Median target: ~$120/share

- Ratings: 22 Buys, 5 Outperforms, 16 Holds, 1 Sell

It looks like analysts see room for gains, but conviction is not strong. Some expect Okta to rebound as margins scale, while others think growth could continue to slow. The takeaway is that expectations are still muted, and Okta will need consistent execution to climb higher.

Upside exists, but the stock is better treated as a rebound candidate than a sure-fire winner. Investors should factor in both the growth potential and the risk of further setbacks.

See analysts’ growth forecasts and price targets for Okta (It’s free!) >>>

Okta: Growth Outlook and Valuation

Okta’s financial outlook points to steady growth and improving profitability:

- Revenue projected to grow about 10% annually through early 2028

- Operating margins expected to reach 26%

- Shares valued at around 27x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model points to ~$112/share by January 2028

- That implies about 22% total upside, or roughly 9% annualized returns

These forecasts show Okta is shifting from rapid expansion to sustainable growth. Profitability is improving, and valuation assumptions look reasonable for a company entering a more mature phase. For investors, Okta offers a balanced setup with moderate but consistent return potential if it delivers on these expectations.

Value stocks like Okta in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Okta’s improving profitability and steady demand for identity security are giving analysts confidence in its recovery story. The company continues to benefit from enterprise clients consolidating multiple vendors into a single platform, where Okta already has strong recognition.

Its latest product launches, including the Identity Security Fabric, Cross App Access, and the acquisition of Axiom Security, also strengthen its position in fast-growing areas like AI-enabled identity protection and privileged access management. These developments show Okta is staying proactive in adapting to the next phase of cybersecurity, which could support long-term growth and margin stability.

For investors, Okta’s push into AI-driven security and platform consolidation offers a credible path for steady compounding, provided it continues executing well.

Bear Case: Valuation and Execution Risks

The main concern is that Okta’s growth has slowed while competition has intensified. Larger players such as Microsoft continue to bundle identity services, making it harder for Okta to expand market share at the same pace as before.

There is also the question of consistency. The company’s turnaround depends on sustaining profitability while reigniting growth, a balance that’s difficult in a crowded market. If progress slows or adoption of new products lags, sentiment could weaken and limit upside potential.

For investors, the stock’s valuation already prices in much of the improvement story. Any stumble in execution could make Okta’s recovery take longer than the market expects.

Outlook for 2028: What Could Okta Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Okta could trade near $112/share by early 2028. That would represent about a 22% gain from today’s level, or roughly 9% annualized returns.

This scenario assumes steady revenue growth and gradual margin expansion. While this would mark solid performance, it already reflects a fair amount of optimism. To deliver stronger upside, Okta would likely need to beat forecasts either through faster customer adoption or greater operating leverage.

For investors, Okta now looks like a steady compounder in the cybersecurity space. It may not deliver dramatic returns, but with consistent execution, it could provide moderate, reliable growth in a sector that remains essential.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.