Dollar General Corp. (NYSE: DG) has faced pressure from weaker sales trends and rising costs, but the stock has managed to rebound from a 52-week low of $66/share. It now trades near $100/share as investors weigh the potential for a slow but steady recovery. With its discount model and large footprint, the company remains a key player in U.S. retail, but analysts remain cautious about how much upside is left.

Recently, management has taken steps to improve performance by closing underperforming stores, remodeling existing locations, and investing in its DG Media Network, which grew sales more than 25% in the last quarter. The company is also leaning more on digital efforts, with online sales expected to grow meaningfully in 2025. These moves show that Dollar General is not just relying on cost discipline, but also trying to expand into higher-margin areas and strengthen its long-term positioning.

This article explores where Wall Street analysts think Dollar General could trade by 2028. We have pulled together consensus targets, growth forecasts, and valuation models to map out the stock’s possible trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Moderate Upside

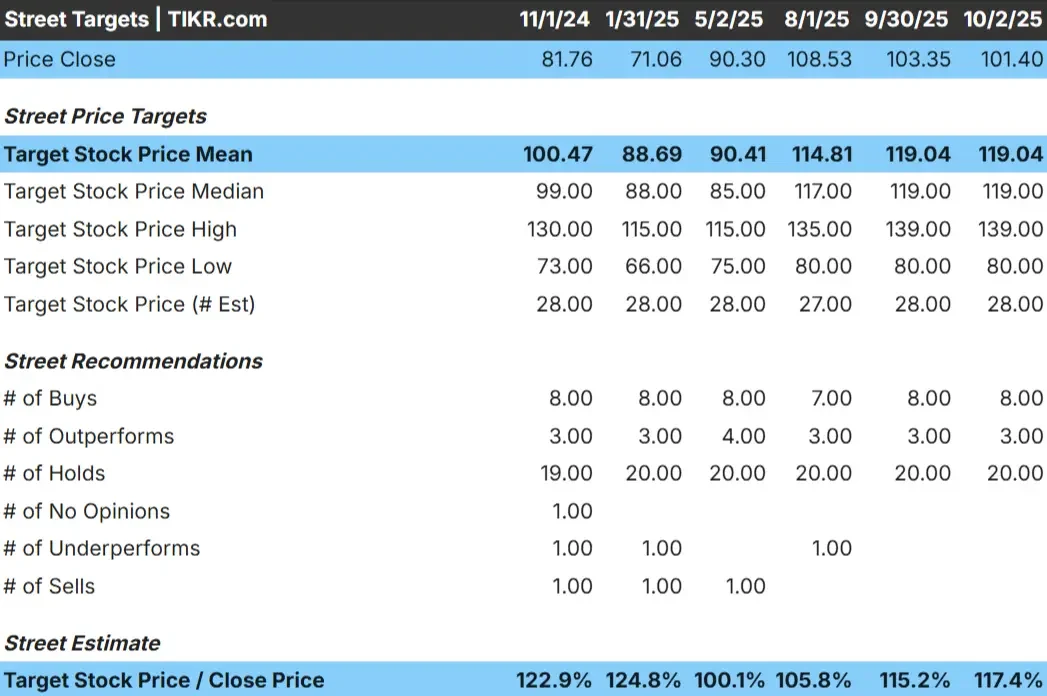

Dollar General trades at about $100/share today. The average analyst price target is $119/share, which points to roughly 19% upside. Forecasts show a narrower spread compared to peers:

- High estimate: ~$139/share

- Low estimate: ~$80/share

- Median target: ~$119/share

- Ratings: Mostly Holds, with some Buys and a few Sells

It looks like analysts see some recovery potential, but the mix of ratings suggests conviction is limited. Most expect the stock to improve from its lows, but few see a return to its prior highs anytime soon.

For investors, the potential 17% upside positions Dollar General as more of a steady recovery play than a growth story. Stability is the theme, not momentum.

See analysts’ growth forecasts and price targets for Dollar General (It’s free!) >>>

Dollar General: Growth Outlook and Valuation

The company’s fundamentals point to steady, not rapid, growth:

- Revenue projected to grow ~4% annually through 2028

- Operating margins expected near 5%

- Shares trade at ~16x forward earnings, close to historical averages

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 15.4x forward P/E suggests ~$128/share by 2028

- That implies ~26% upside, or about 10% annualized returns

These forecasts suggest Dollar General is fairly valued relative to its growth profile. The stock is set up for consistent but unspectacular compounding.

For investors, Dollar General looks like a defensive value holding. Long-term returns are likely to be moderate, making execution on cost control and expansion plans critical to achieving upside.

Value stocks like Dollar General in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Dollar General continues to benefit from its position as a discount leader during periods of tight consumer spending. When shoppers trade down, the company often captures higher store traffic. Expansion in underserved rural areas adds another growth lever, while efficiency initiatives in logistics and labor provide margin support.

The combination of trade-down demand, broad footprint, and operational improvements gives bulls confidence that Dollar General can maintain steady earnings power.

For investors, the optimistic case is that Dollar General’s defensive qualities and efficiency gains keep it a reliable compounder, even if revenue growth stays modest.

Bear Case: Valuation and Competition

Despite these positives, Dollar General faces intense competition from Walmart, Dollar Tree, and grocery chains. Rising wages and supply chain costs pose risks to already thin margins. If shoppers shift spending or rivals capture more share, growth could disappoint.

The concern is that the recent rebound may have already priced in much of the near-term recovery. Without stronger growth drivers, the stock could remain stuck in a lower valuation range.

For investors, the bear case is that Dollar General’s upside is capped and that weak consumer demand or rising costs could stall progress, leaving returns underwhelming.

Outlook for 2028: What Could Dollar General Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 15.4x forward P/E suggests ~$128/share by 2028. That would represent about a 26% gain from today’s level, or roughly 10% annualized returns.

This outcome assumes revenue grows around 4% annually and margins hold steady near 5%. While this would mark a healthy recovery from recent lows, it already reflects a fair amount of optimism. To deliver stronger upside, the company would likely need to outperform expectations on efficiency, sales recovery, or market share gains.

For investors, Dollar General looks like a stable long-term compounder, but not a stock set up for dramatic gains. Upside depends on disciplined execution and resilience in a competitive landscape.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.