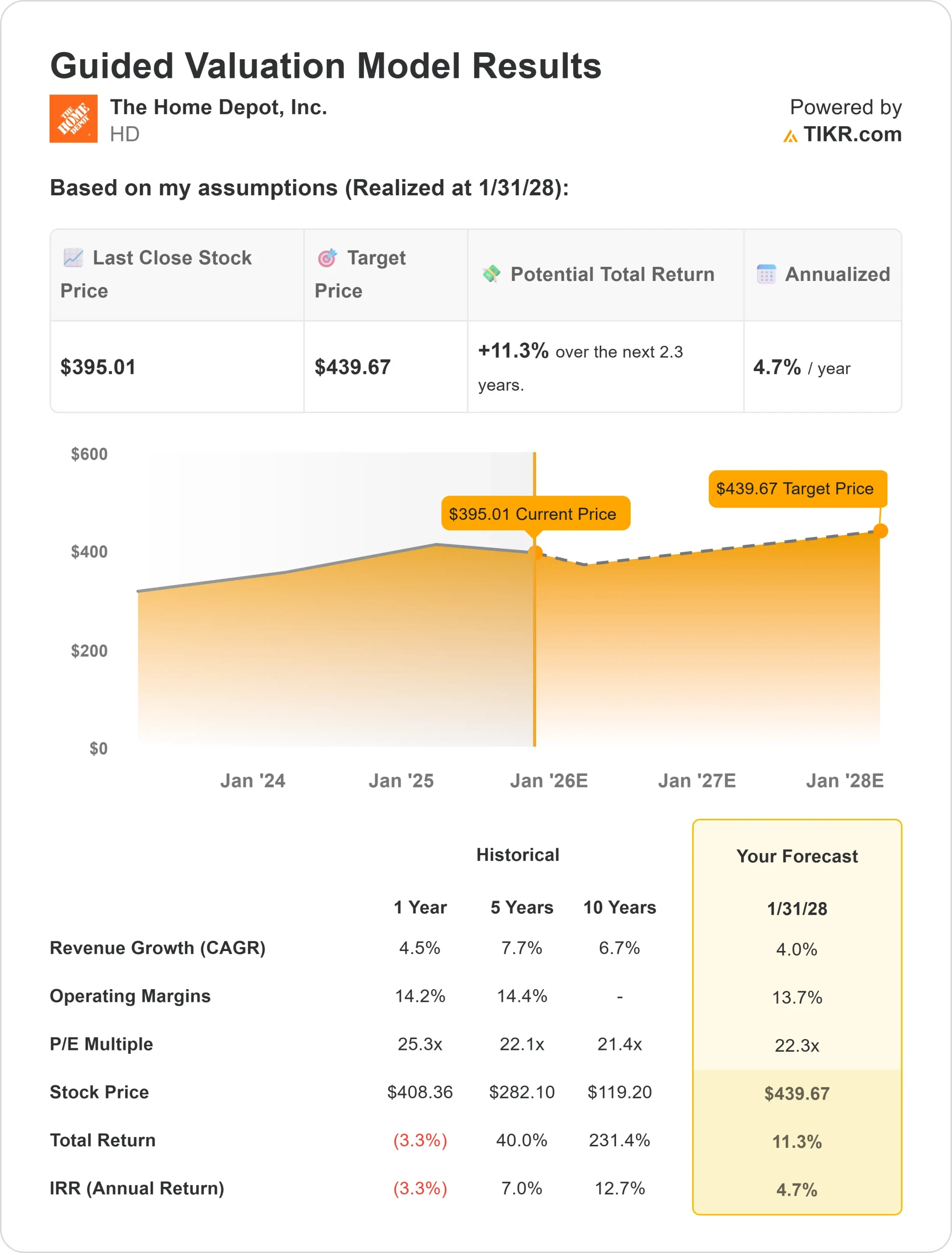

Home Depot (NYSE: HD) has long been a bellwether for U.S. housing and consumer spending. The stock trades near $395/share, down about 4% over the past year as higher interest rates and slower housing activity weighed on results. Despite these challenges, Home Depot’s scale, brand recognition, and strong pro-customer relationships remain key strengths. The question for investors is whether modest growth will be enough to support the stock at current valuation levels.

Recently, Home Depot has doubled down on digital innovation and professional customer services. The company rolled out a new Project Planning tool for contractors, aimed at simplifying material orders and crew coordination, while also reporting more than 10% growth in online sales last quarter. These initiatives highlight how Home Depot is adapting beyond traditional retail to strengthen its long-term competitive edge.

This article explores where Wall Street analysts see Home Depot trading by 2028. We have pulled together consensus price targets, growth forecasts, and valuation models to outline the stock’s potential trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Limited Upside

Home Depot trades at about $395/share today. The average analyst price target is $438/share, which suggests around 11% upside. Forecasts reflect a wide range of outcomes:

- High estimate: ~$497/share

- Low estimate: ~$335/share

- Median target: ~$450/share

- Ratings: mix of Buys, Holds, and a few Sells

The spread from $335 to nearly $500 highlights the uncertainty around future performance. For investors, the takeaway is that upside looks modest and closely tied to the health of the housing market.

See analysts’ growth forecasts and price targets for Home Depot (It’s free!) >>>

Home Depot: Growth Outlook and Valuation

The company’s fundamentals suggest stability rather than rapid growth:

- Revenue is projected to grow about ~4% annually through 2028

- Operating margins expected to remain near ~14%

- Shares trade at ~25x forward earnings, above the 10-year average of ~21–22x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 22x forward P/E suggests ~$440/share by 2028

- That implies ~11% upside, or about 5% annualized returns

These forecasts indicate Home Depot is a dependable operator, but already fairly valued for its slower pace of growth. For investors, this means the stock is more of a steady compounder than a high-upside opportunity unless fundamentals improve beyond current expectations.

Value stocks like Home Depot in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Home Depot benefits from a strong brand, a large base of professional customers, and supply chain efficiencies that help protect profitability. Longer-term housing and remodeling demand also provide a steady backdrop.

For investors, this is why bulls see the company as a dependable compounder. The optimism is less about rapid growth and more about resilience and consistency in delivering results.

Bear Case: Valuation and Competition

Even with these strengths, valuation leaves little margin for error. The stock trades at a premium relative to historical norms, while competition from Lowe’s and online retailers continues to pressure pricing. Rising labor and supply costs also remain risks to profitability.

For investors, the bear case is that the stock’s defensive appeal is already reflected in the price. If housing demand softens further or margins slip, shares could reset lower.

Outlook for 2028: What Could Home Depot Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 22x forward P/E suggests Home Depot could trade near $440/share by 2028. That would represent about an 11% gain from today’s level, or roughly 5% annualized returns.

For investors, this outcome highlights Home Depot as a stable long-term holding, but not one positioned for outsized gains. Stronger housing demand or improved efficiencies would be needed to push returns meaningfully higher.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.