Norfolk Southern Corporation (NYSE: NSC) has recovered from a tough stretch marked by network disruptions and cost pressures. The stock trades near $285/share, up around 10% in the past year, as investors grow more confident in its margin improvement and service reliability.

Recently, the company reaffirmed its commitment to steady shareholder returns with another quarterly dividend and announced a new intermodal partnership with Union Pacific aimed at improving freight efficiency and expanding network capacity. These steps highlight how Norfolk Southern is moving beyond stabilization and positioning for long-term growth.

This article explores where Wall Street analysts think Norfolk Southern could trade by 2027. We have compiled consensus price targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

Norfolk Southern trades near $285/share today. The average analyst price target is $313/share, which points to about 8% upside over the next year. Forecasts are fairly tight, showing moderate confidence in the outlook:

- High estimate: ~$367/share

- Low estimate: ~$285/share

- Median target: ~$303/share

- Ratings: 6 Buys, 1 Outperform, 16 Holds

With roughly 8% upside implied, analysts see modest potential from current levels. For investors, this means the recent recovery is mostly reflected in the stock price. Norfolk Southern could outperform if freight volumes rebound faster or if ongoing cost initiatives deliver stronger-than-expected earnings momentum.

See analysts’ growth forecasts and price targets for Norfolk Southern (It’s free!) >>>

Norfolk Southern: Growth Outlook and Valuation

The company’s fundamentals look stable and improving:

- Revenue growth: projected at ~3% annually through 2027

- Operating margin: expected to reach about 37%

- Forward P/E: around 18–19x, near its long-term average

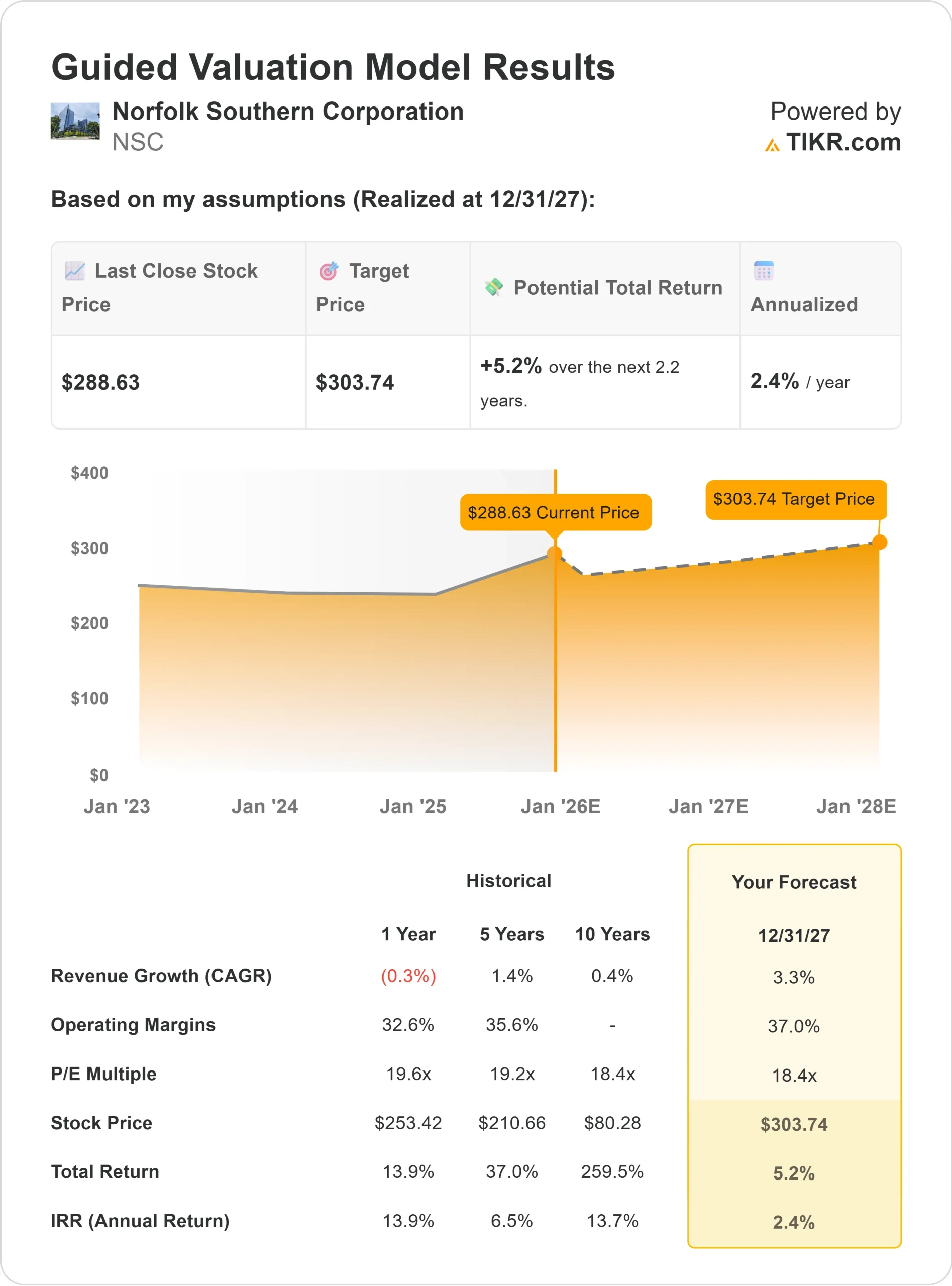

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 18x forward P/E suggests around $304/share by 2027, implying roughly 5% total upside or 2% annualized returns

These estimates indicate that Norfolk Southern’s valuation already captures much of its expected improvement. For investors, this positions the stock as a steady compounder supported by consistent cash flow and dividends, rather than a high-growth opportunity.

Value stocks like Norfolk Southern in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Norfolk Southern continues to make operational progress after several challenging years. The company recently reopened the Howard Street Tunnel ahead of schedule, expanding intermodal capacity and improving train velocity across the East Coast.

Management’s focus on cost control, pricing discipline, and service reliability has also strengthened margins despite softer freight demand. These ongoing improvements support a more efficient and dependable network.

For investors, these actions suggest a more resilient Norfolk Southern built for long-term stability. The company’s strong cash generation and disciplined capital spending provide a solid foundation for consistent compounding.

Bear Case: Demand and Cost Pressure

Growth catalysts remain limited. Freight demand is cyclical and closely tied to industrial production, which has yet to fully rebound. Rising labor and maintenance costs could also limit margin expansion, especially if volume growth remains sluggish.

For investors, this means Norfolk Southern’s earnings growth could plateau if macro conditions weaken. The stock’s valuation, near historical averages, leaves limited room for disappointment should pricing power or efficiency gains fade.

Outlook for 2027: What Could Norfolk Southern Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 18x forward P/E suggests around $304/share by 2027, implying about 5% total upside or roughly 2% annualized returns from current levels.

While this forecast reflects modest growth, it already assumes steady cost discipline and continued efficiency gains. To unlock stronger upside, Norfolk Southern would need a sharper recovery in freight volumes or additional operating leverage from automation and network optimization.

For investors, Norfolk Southern stands out as a reliable long-term compounder built on efficiency, cash flow, and dividend stability. It offers limited near-term upside but remains attractive for portfolios focused on steady income and capital preservation.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.