FedEx Corporation (NYSE: FDX) has faced a challenging year as weaker shipping demand and inflation pressures weighed on margins. The stock trades near $236/share, down about 11% over the past 12 months. Still, analysts see potential for recovery as cost-cutting and efficiency initiatives begin to strengthen profitability.

Recently, FedEx reported better-than-expected quarterly results, showing progress in its ongoing cost reduction and transformation efforts. Management highlighted improvements in efficiency and profitability, along with continued work on restructuring parts of the business to simplify operations and strengthen long-term growth. These updates underscore FedEx’s focus on becoming a leaner, more adaptable company as global shipping demand remains uneven.

This article explores where Wall Street analysts expect FedEx’s stock to trade by 2028. We’ve compiled consensus targets and valuation models to outline the company’s potential path ahead. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

FedEx trades at about $236/share today. The average analyst price target is $266/share, which points to around 13% upside over the next year. Forecasts remain fairly tight:

- High estimate: ~$320/share

- Low estimate: ~$200/share

- Median target: ~$271/share

- Ratings: 16 Buys, 3 Outperforms, 10 Holds, 2 Sells

Analysts see room for modest gains as FedEx’s cost-cutting and efficiency programs take hold. For investors, this suggests steady recovery potential, though not a major breakout. If management keeps margins stable and shipping volumes recover, the stock could gradually rebuild momentum from here.

See analysts’ growth forecasts and price targets for FedEx (It’s free!) >>>

FedEx: Growth Outlook and Valuation

The company’s fundamentals appear stable, with gradual improvement expected over the next few years:

- Revenue is projected to grow about 3.9% annually through 2028

- Operating margins are expected to hold near 7.1%

- Shares trade at roughly 12.3× forward earnings, close to historical averages

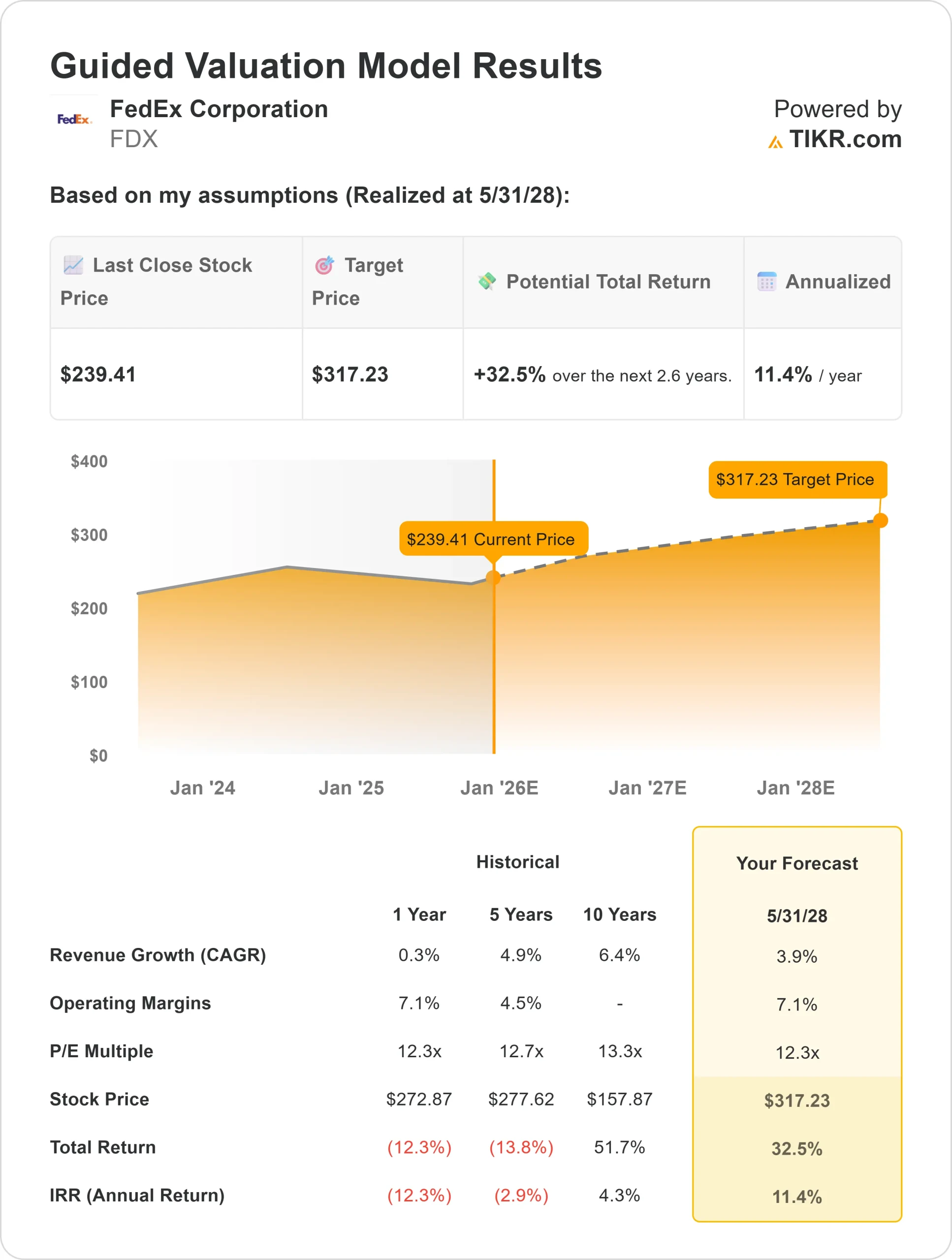

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 12.3× forward P/E suggests around $317/share by 2028

- That implies about 33% total upside, or roughly 11% annualized returns

These figures suggest FedEx can compound steadily as efficiency gains strengthen margins and cost initiatives take hold. For investors, the stock appears reasonably valued today, offering a mix of stability and moderate growth potential as global demand gradually recovers.

Value stocks like FedEx in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

FedEx’s transformation plan, known as DRIVE, continues to support gradual improvement in profitability. The initiative aims to cut costs through network optimization, automation, and better capacity utilization. Management has already begun simplifying operations, with early signs showing margin stability even in a softer freight environment.

Digital investments are also paying off. FedEx’s use of AI routing tools and capacity forecasting has helped improve delivery times and reduce fuel costs. For investors, these changes indicate a more agile and cost-efficient business that could drive stronger earnings recovery as global shipping volumes stabilize.

Bear Case: Competition and Volume Risk

Despite progress, FedEx still faces an uneven demand backdrop. Slower e-commerce growth and lingering weakness in international freight remain challenges. Competition from UPS and Amazon’s expanding logistics network could pressure pricing power and market share.

For investors, this means earnings growth may stay limited if volumes do not fully rebound. While cost discipline has strengthened the bottom line, FedEx’s top-line performance will need to improve before the stock can meaningfully re-rate higher.

Outlook for 2028: What Could FedEx Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 12.3× forward P/E suggests roughly $317/share by 2028. That represents about 33% total upside, or roughly 11% annualized returns from current levels.

For investors, this outlook points to a steady recovery story rather than explosive growth. FedEx’s leaner cost structure and improving cash flow make it a dependable value play, but upside depends on whether global trade and parcel demand return to pre-2023 levels.

In short, FedEx looks well-positioned for gradual compounding if its cost efficiencies hold, but a sustained rally will require reacceleration in shipping volumes and consistent execution on its DRIVE goals.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.