Key Takeaways for Moody’s Corporation Stock

- Moody’s posted revenue of $2.08 billion in Q1 2026, up 8% year over year, with rated issuance surpassing $2 trillion for the first time in a single quarter.

- Operating margins held at 46% in Q1 2026, as Moody’s Investors Service (MIS) delivered an adjusted segment operating margin of 67%.

- Adjusted diluted EPS of $4.33 came in above the prior-year quarter, with full-year guidance maintained despite geopolitical volatility.

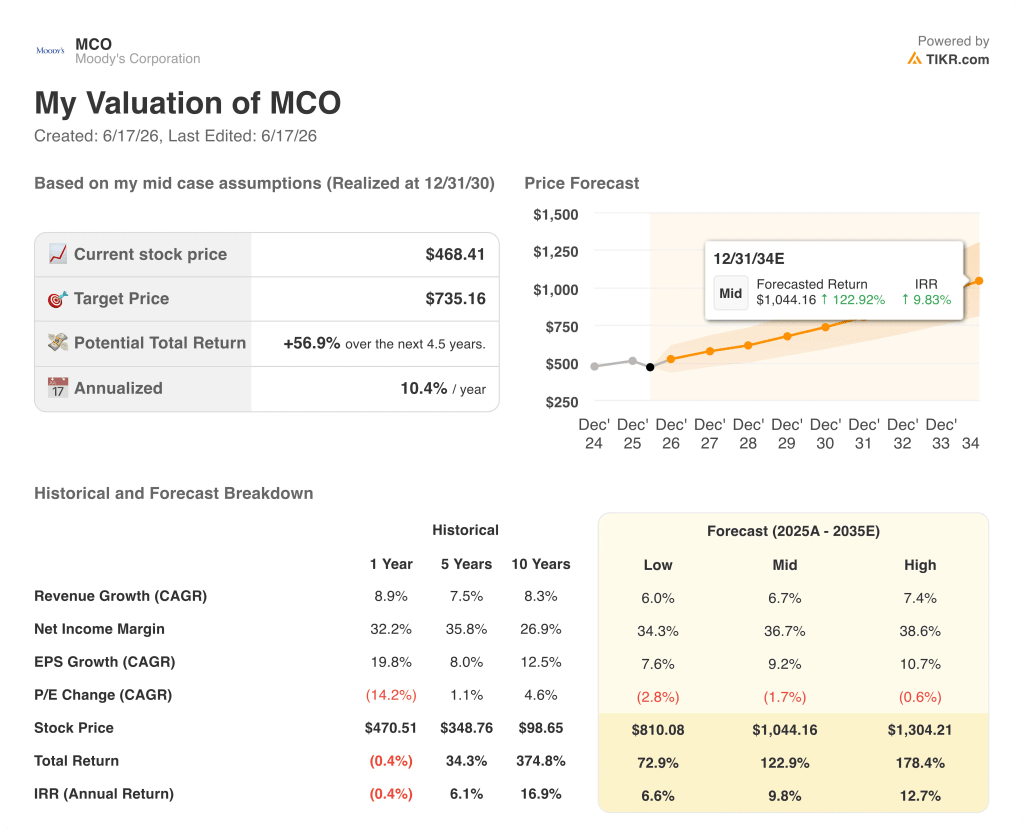

- TIKR’s model values MCO at approximately $735 by the end of 2030, implying around 57% total return from the current price of $468.

Moody’s Corporation Posts Record Issuance Quarter as AI Demand Reshapes the Ratings Business

Moody’s Corporation (MCO) reported Q1 2026 results on April 22, 2026, with revenue reaching $2.08 billion and rated issuance crossing $2 trillion for the first time in a single quarter.

The company operates two businesses: Moody’s Investors Service (MIS), which issues credit ratings on bonds and loans, and Moody’s Analytics (MA), which sells risk data, financial models, and compliance software to banks, insurers, and corporates.

MIS delivered record volume in the quarter, fueled by investment-grade issuance from hyperscalers — the largest cloud computing companies — with CEO Rob Fauber noting that issuance from the top five hyperscalers year-to-date had already exceeded full-year 2025 levels.

Private credit-related revenue within MIS grew more than 80% year over year, driven by investor demand for independent credit assessment as scrutiny of private markets intensified.

MA revenue grew 8% in the quarter, with Annual Recurring Revenue (ARR — the annualized value of active subscription contracts) reaching $3.6 billion.

MA’s adjusted operating margin expanded 250 basis points year over year to 33%, as the segment moves toward management’s guided range of 34% to 35% for the full year.

Fauber even addressed on Q1 earnings call: “when our intelligence is embedded directly into customer decision-making, we see tangible outcomes, higher retention, expanding relationships and more durable recurring revenue.”

MA announced an MCP (Model Context Protocol) application with Anthropic, which Fauber described as the first of its kind — enabling Moody’s credit and compliance agents to run natively inside the Claude interface.

New Moody’s Analytics CEO Cristina Kosmowski joins in June, bringing a background at Salesforce and Slack focused on enterprise go-to-market and customer success at scale.

Full-year guidance was unchanged, with management citing structural demand tied to AI infrastructure, energy transition, private credit, and M&A as durable multi-year drivers.

How Operating Leverage Is Widening Moody’s Margins While Expenses Stay Controlled

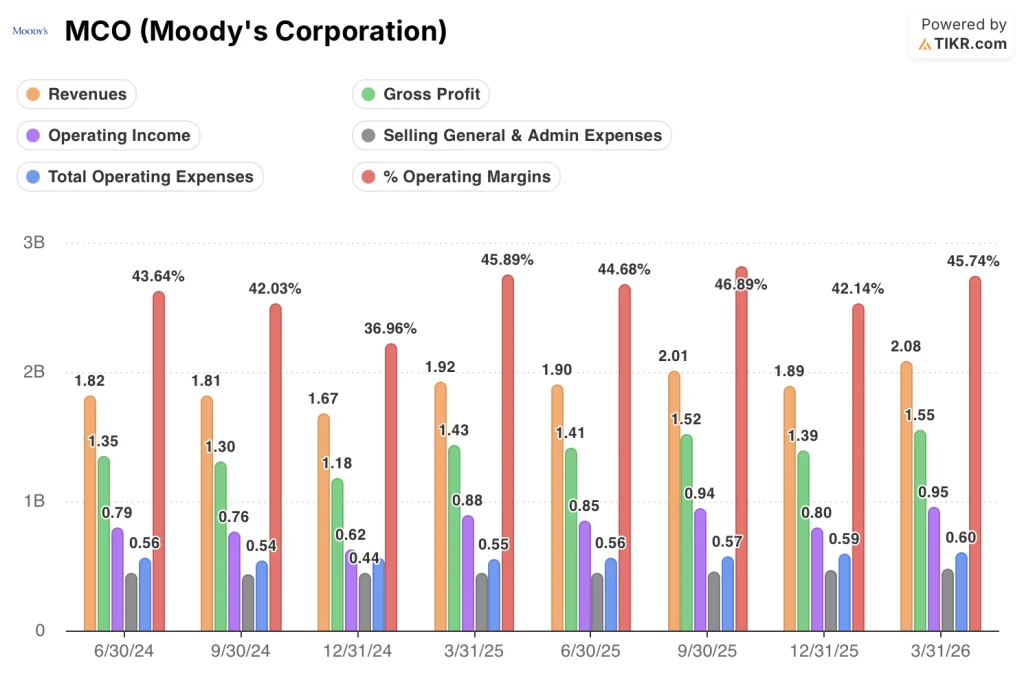

Moody’s revenue grew 8% year over year to $2.08 billion in Q1 2026, continuing a multi-quarter expansion trajectory.

Gross profit reached $1.55 billion in the quarter, with gross margins holding at 75%.

Gross profit grew 8% year over year, matching the pace of top-line growth and confirming that cost of goods sold is not outrunning revenue.

Operating income came in at $0.95 billion for the quarter, up 8% year over year.

Operating margins reached 46% in Q1 2026, consistent with the 46% delivered in Q1 2025 and above the 42% posted in Q4 2025.

SG&A for the quarter was $0.48 billion, a modest increase from $0.44 billion in the same period a year ago.

Total operating expenses were $0.60 billion in Q1 2026, essentially flat with the $0.55 billion in Q1 2025 — the gap between gross profit growth and operating expense growth is where the operating leverage lives.

The MIS segment delivered an adjusted operating margin of 67%, with management attributing the performance to technology investments in workflow automation and AI-enabled efficiency in analyst processes — including automating roughly 25% of pre-ratings-committee checks.

MA’s margin expansion from 30% to 33% year over year indicates the restructuring and portfolio rationalization actions are translating to the income statement.

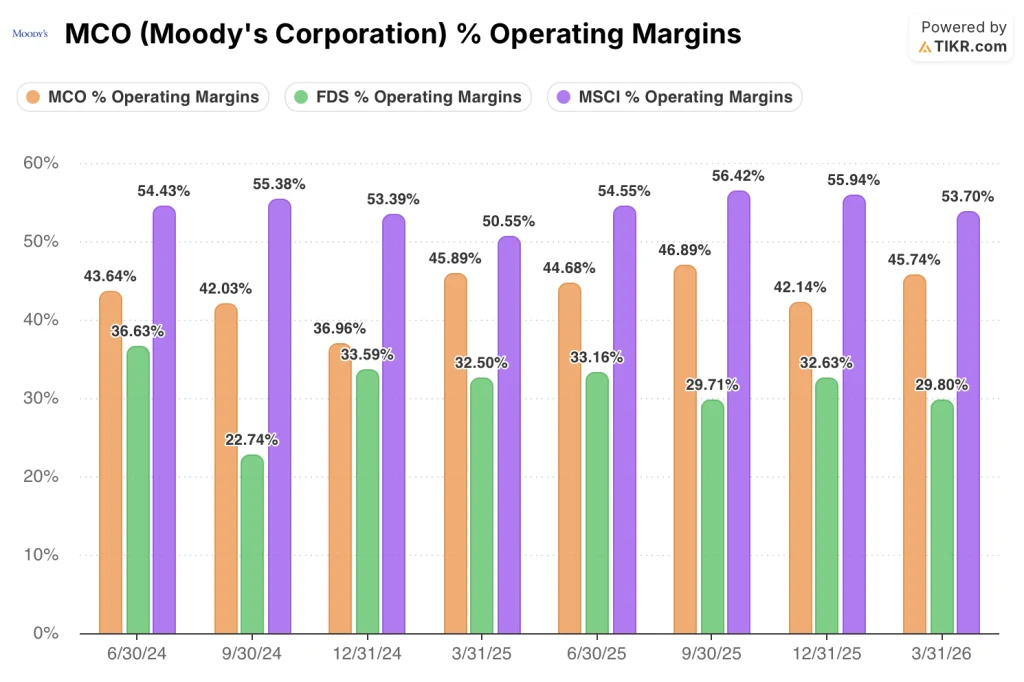

MSCI Leads the Peer Group on Operating Margins While Moody’s Closes the Gap on FactSet

MSCI Inc. (MSCI) held a 54% operating margin in Q1 2026, roughly 8 points above Moody’s 46% in the same period.

FactSet Research (FDS) posted a 30% operating margin in Q1 2026, sitting 16 points below Moody’s and confirming that the operating leverage thesis is not a peer-wide phenomenon.

The gap between Moody’s and MSCI has been structurally consistent across eight quarters, with MSCI ranging from 51% to 56% while Moody’s has ranged from 37% to 47%.

Moody’s margin has recovered from the 37% trough posted in Q4 2024, and the Q1 2026 reading of 46% is the strongest in three quarters — the trajectory the TIKR target depends on is already visible in the sequential data.

Is Moody’s Stock Undervalued in 2026? TIKR’s $735 Model Implies 57% Upside

TIKR’s model values Moody’s at approximately $735 by December 2030, implying around 57% total return from the current price of approximately $468, or roughly 10% per year.

The target rests on the same operating leverage mechanism the income statement already demonstrates: gross margins holding above 74% while operating expenses grow slowly enough to let operating income compound.

MIS margin durability at approximately 67% provides the earnings floor — if record issuance activity moderates, the segment still converts revenue at a rate that supports the long-term target.

The MA margin expansion trajectory, moving from 33% toward the guided 34% to 35% this year and mid-to-high 30s by end of 2027, adds the second compounding layer that makes the annualized return credible.

Should You Invest in Moody’s Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Moody’s Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Moody’s Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MCO stock on TIKR for Free →

What did Moody’s say about its AI strategy?

Moody’s described a three-pillar GenAI strategy built on connected intelligence, agentic workflows, and partner distribution — with active partnerships with Anthropic, Microsoft, AWS, and OpenAI — positioning proprietary data as a required context layer for enterprise AI decisions.