Microchip Technology Incorporated (NASDAQ: MCHP) has faced a challenging stretch as the semiconductor industry cycles through weaker demand. Revenue has softened across industrial and consumer segments, and the stock trades near $62/share, well below its 2024 highs. Still, analysts see encouraging signs of recovery as Microchip leans into higher-growth markets like automotive, data center, and connectivity.

Recently, the company announced plans to ramp investments in next-generation microcontrollers and automotive chips, positioning itself to capture demand from electric vehicles and industrial automation. Management also reaffirmed its focus on cost discipline and strong free cash flow, signaling confidence that margins can hold steady despite softer near-term sales. These moves reflect a company preparing for the next upcycle rather than simply waiting for it.

This article explores where Wall Street analysts think Microchip Technology could trade by 2028. We have pulled together consensus price targets and valuation models to outline the stock’s potential path. These figures reflect analyst expectations and not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

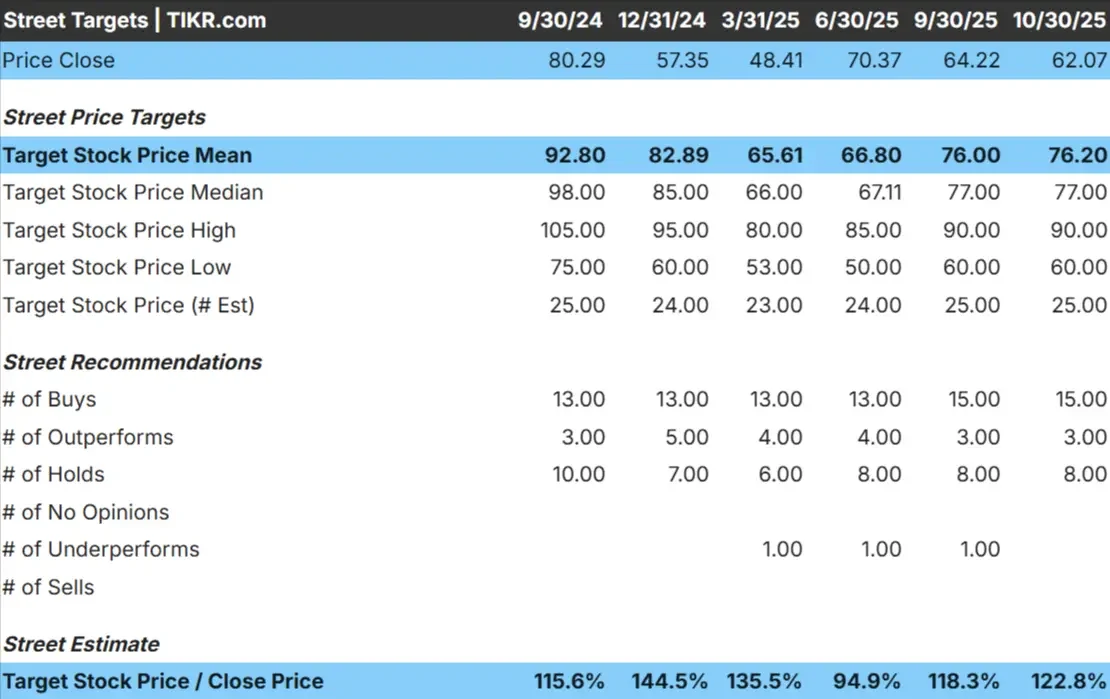

Microchip trades near $62/share today. The average analyst price target is $76/share, suggesting about 23% potential upside. Forecasts show a moderate spread that reflects measured optimism among analysts:

- High estimate: ~$90/share

- Low estimate: ~$60/share

- Median target: ~$77/share

- Ratings: 15 Buys, 3 Outperforms, 8 Holds

For investors, this points to modest upside potential. Analysts generally agree that Microchip’s fundamentals remain strong, but the expected rebound in demand may already be partially reflected in the current share price. The takeaway is that while the stock could outperform if end-markets recover faster than expected, near-term gains are likely to be gradual rather than explosive.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Microchip: Growth Outlook and Valuation

The company’s financial outlook remains solid, supported by strong execution and exposure to long-term growth drivers:

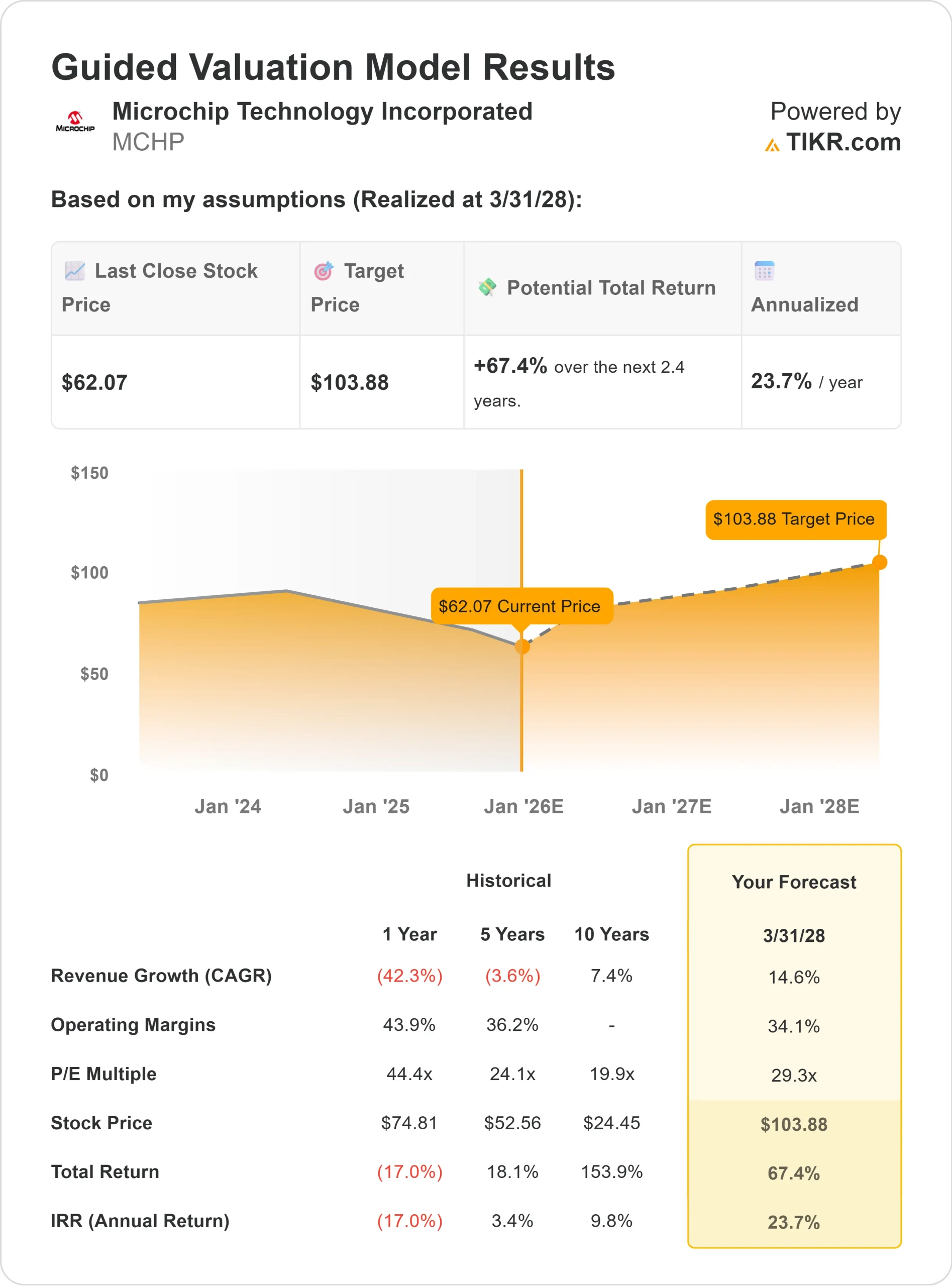

- Revenue growth: ~14.6% CAGR through 2028

- Operating margin: ~34.1% forecast

- Forward P/E: ~29x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 29x forward P/E suggests around $104/share by 2028

- That implies roughly 67% total return, or about 24% annualized

For investors, these projections suggest a steady compounder rather than a high-flyer. Microchip’s disciplined capital allocation, efficient cash conversion, and focus on automotive and industrial applications position it well for sustainable value creation. If global chip demand stabilizes, the company could see both earnings and valuation multiple expansion over the next few years.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Microchip continues to strengthen its position in high-value markets like automotive, industrial, and data center connectivity. These segments tend to offer more stable demand than consumer electronics, helping smooth out the company’s exposure to economic swings.

Management’s focus on innovation in microcontrollers and analog solutions keeps Microchip at the core of the smart device ecosystem. Its steady design wins across electric vehicles and embedded control systems show that the company’s technology remains essential to next-generation manufacturing and automation.

For investors, these trends suggest a business that is gradually shifting toward more predictable growth. Microchip’s consistent free cash flow, cost discipline, and shareholder returns point to a company that is prepared for recovery rather than waiting for it.

Bear Case: Cyclicality and Valuation

Even with these strengths, Microchip is still tied to the broader semiconductor cycle. If end-market demand remains soft or customers continue to reduce inventories, near-term earnings may stay under pressure.

The stock’s current valuation also reflects some recovery expectations. Trading around 29x forward earnings, Microchip is not cheap by historical standards, especially with revenue growth still normalizing.

For investors, the risk is timing. A delayed rebound could limit returns in the next year or two, even if the long-term thesis stays intact. Patience will likely be key to realizing the full upside potential.

Outlook for 2028: What Could Microchip Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Microchip could trade near $104/share by 2028. That represents about 67% upside, or roughly 24% annualized returns from current levels.

While that outcome assumes a healthy recovery, it is not overly aggressive. To deliver stronger gains, Microchip would need faster demand acceleration across automotive and industrial markets, along with margin expansion from higher-value chips.

For investors, Microchip looks like a steady compounder rather than a speculative play. Its fundamentals and execution quality make it appealing for those willing to hold through the cycle and capture long-term compounding once the market stabilizes.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>