Fairfax Financial (FFH) remains one of Canada’s most distinctive financial institutions, an insurance-led conglomerate built on disciplined underwriting and value-driven investing. Under Chairman and CEO Prem Watsa, the firm operates through a mix of property-and-casualty insurers, reinsurers, and non-insurance subsidiaries spanning dozens of markets.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The strategy is simple but potent: compound book value through two engines, consistent underwriting profits, and long-term investment returns. That model delivered again in 2025, as the company posted net earnings of $1.44 billion ($61.61 per diluted share), a combined ratio of 93.3%, and an underwriting profit of $427 million. Net investment gains reached $952 million, powered by $800 million in equity gains and a sharp uptick in interest income from higher yields.

Book value per basic share climbed to $1,158.47, up 10.8% year-to-date after adjusting for its $15 annual dividend. With nearly $3 billion in holding-company cash and a conservatively positioned $67.8 billion investment portfolio (about 15% in cash and short-term investments), Fairfax continues to balance growth and resilience.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Fairfax’s core property-and-casualty operations showed steady expansion in Q2, with gross premiums written up 2.6% to $9.18 billion and net premiums written up 4.8% to $7.26 billion. That growth was broad-based across reinsurance and casualty lines, supported by modest rate increases and selective underwriting. The combined ratio improved to 93.3% from 93.9%, as lower catastrophe losses and favorable prior-year reserve development offset mild cost inflation.

| Metric | Q2 2025 | Change (YoY) | Notes |

|---|---|---|---|

| Net Earnings | $1.44 B | +57% | Driven by higher investment gains |

| Diluted EPS | $61.61 | +66% | Boosted by equity portfolio performance |

| Gross Premiums Written | $9.18 B | +2.6% | Broad-based growth across lines |

| Net Premiums Written | $7.26 B | +4.8% | Increased retentions and new business |

| Underwriting Profit | $427 M | +15% | Combined ratio improved to 93.3% |

| Net Gains on Investments | $952 M | +293% | Equity gains of $800 M drove results |

| Interest & Dividends | $666 M | +8% | Higher carry from short-duration bonds |

| Book Value per Share | $1,158.47 | +10.8% YTD | After $15 dividend payout |

| Debt-to-Capital | 25.9% | +1.1 pts | Post $900 M note issuance |

Investment income once again proved to be Fairfax’s differentiator. Net gains on investments surged to $952 million, led by equities, while interest and dividend income rose 8% to $666 million, thanks to the tailwind from higher rates. The company’s adjusted operating income from insurance operations was $1.13 billion, essentially flat year over year, underscoring stability amid market volatility.

Leverage remained well controlled at 25.9% debt-to-capital, even after issuing $900 million in new senior notes during the quarter. Book value continued to expand at a mid-teens pace, confirming Fairfax’s ability to convert market strength into tangible shareholder value.

Look up Fairfax Financial’s full financial results & estimates (It’s free) >>>

Broader Market Context

Global P&C pricing remains firm, and reinsurance capacity is tight, a favorable backdrop for Fairfax’s disciplined underwriting approach. The company has leaned into rate adequacy rather than growth at any cost, helping sustain profitability even as inflation lingers.

On the investment side, higher bond yields have been a structural tailwind, allowing Fairfax to earn attractive carry while keeping its duration short. Yet market volatility remains a swing factor: in good quarters, equity exposure boosts book value rapidly; in risk-off periods, it can just as easily reverse.

1. Underwriting Discipline Still Showing Up

Fairfax’s underwriting results demonstrate its commitment to steady, profitable growth. The group produced a $427 million underwriting profit across its property-and-casualty book, with strength in reinsurance and specialty lines offsetting softer commercial volumes in North America.

Favorable reserve development of $163 million and reduced catastrophe losses of $140 million reinforced the quarter’s profitability. Fairfax’s decision to maintain tight pricing and risk selection continues to pay off, the company isn’t chasing market share, just underwriting precision. That discipline has kept its combined ratio consistently below 95%, giving it a margin of safety most insurers would envy.

2. The Investment Engine Keeps Compounding

Fairfax’s investment portfolio remains its defining edge. With $67.8 billion in insurance portfolios and 70% of its fixed-income holdings in U.S. Treasuries and government bonds, the company is well-positioned to benefit from high short-term yields without stretching for risk.

At the same time, the firm’s selective equity positions add torque. The $800 million in realized and unrealized stock gains this quarter show the potential upside of its value-oriented investment style. The same approach has historically driven Fairfax’s book value growth. Watsa’s strategy of deploying patient capital into misunderstood assets continues to set Fairfax apart from its more passive peers.

Value stocks like Fairfax Financial in less than 60 seconds with TIKR (It’s free) >>>

3. Capital Deployment and Strategic Investments

Fairfax remains active in reshaping its portfolio for long-term compounding. During the quarter, it acquired a 33% stake in Albingia, a French specialty insurer, and advanced a deal to acquire The Keg Royalties Fund for $151 million. It also consolidated newer subsidiaries like Sleep Country and Peak Achievement under its growing non-insurance umbrella.

Shareholder returns remain generous but disciplined: the company paid its $15 annual dividend, repurchased 257,000 shares, and still held over $3 billion in parent-level liquidity. With debt manageable and access to a $2 billion credit facility extended to 2030, Fairfax enters 2026 from a position of financial strength. The firm’s capital flexibility ensures it can keep compounding even in less forgiving markets.

The TIKR Takeaway

Fairfax continues to execute on both sides of its playbook: strong underwriting discipline and high-yielding investment income. The firm’s YTD book-value growth of 10.8% underscores its ability to deliver double-digit compounding even in a mixed macro backdrop.

Heading into 2026, the outlook hinges on three levers: underwriting margins below 95%, sustained investment income from higher rates, and controlled equity volatility. If those stay aligned, Fairfax’s book value could keep compounding in the mid-teens range. Investors who understand its cyclical rhythm know that patience here often pays exponentially when markets normalize.

Should You Buy, Sell, or Hold Fairfax Financial Stock in 2025?

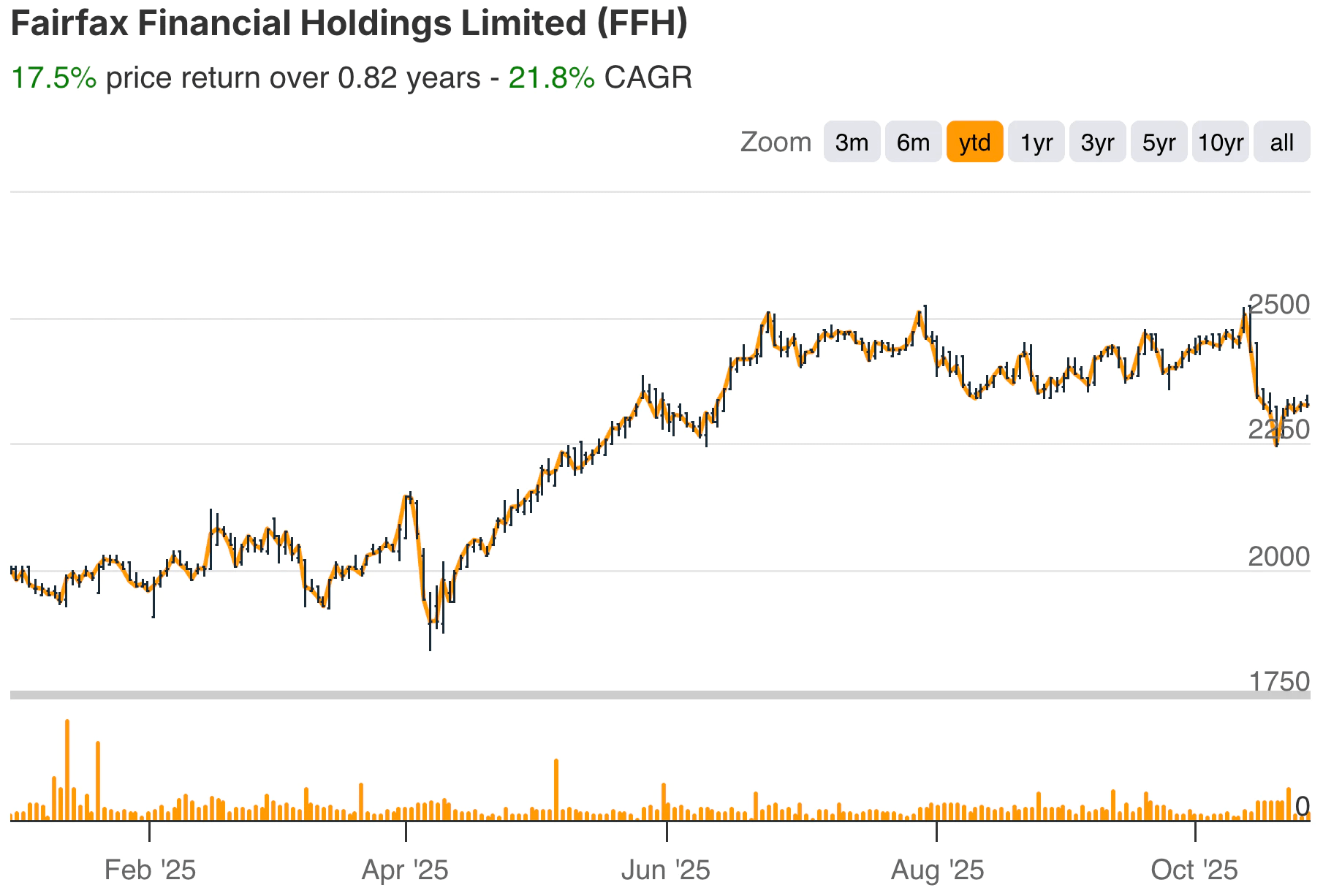

Shares have gained ~17% YTD, reflecting confidence in the company’s resilience. While valuation has approached book value, Fairfax’s disciplined underwriting, strong liquidity, and proven investment framework make it a steady compounder. Investors seeking exposure to insurance plus long-term value investing could still find Fairfax a compelling core holding.

How Much Upside Does Fairfax Financial Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!