KLA Corporation (NASDAQ: KLAC) has been one of the biggest winners in the semiconductor equipment space, climbing more than 80% in the past year as AI-driven chip demand lifted the entire sector. The stock trades near $1,235/share, close to its all-time high. Weakness in valuation upside has caught investor attention, though KLA’s strong profitability and leadership in process control still give analysts reasons for optimism.

Recently, KLA posted quarterly results that topped expectations, driven by strong demand for wafer inspection and metrology systems used in AI and advanced logic chips. According to its fiscal Q1 2026 earnings report, filed on October 29, 2025, management announced a 12% dividend increase and expanded its share repurchase program, signaling confidence in long-term cash generation and shareholder returns. These updates reflect KLA’s continued ability to maintain growth momentum even as the broader chip cycle stabilizes.

This article explores where Wall Street analysts think KLA could trade by 2028. We have pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest the Stock Is Fully Valued

KLA trades near $1,235/share, and analysts have an average price target of $1,051/share, indicating no upside potential at current levels. Forecasts show a tight range that reflects cautious sentiment across Wall Street:

- High estimate: ~$1,300/share

- Low estimate: ~$745/share

- Median target: ~$1,070/share

- Ratings: 8 Buys, 4 Outperforms, 14 Holds, 1 Underperform

For investors, this means analysts believe KLA is already fully valued after its sharp rally. The stock’s strong 2024 performance has likely priced in much of its growth tied to AI and semiconductor demand. Unless earnings outperform expectations or chipmakers ramp up new capital spending, further gains appear limited in the near term.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

KLA: Growth Outlook and Valuation

The company’s fundamentals remain best-in-class, but valuation looks full after a major run-up:

- Revenue is expected to grow about 8% annually through 2028

- Operating margins are projected to stay near 43%

- Shares trade around 24x forward earnings, above peer averages

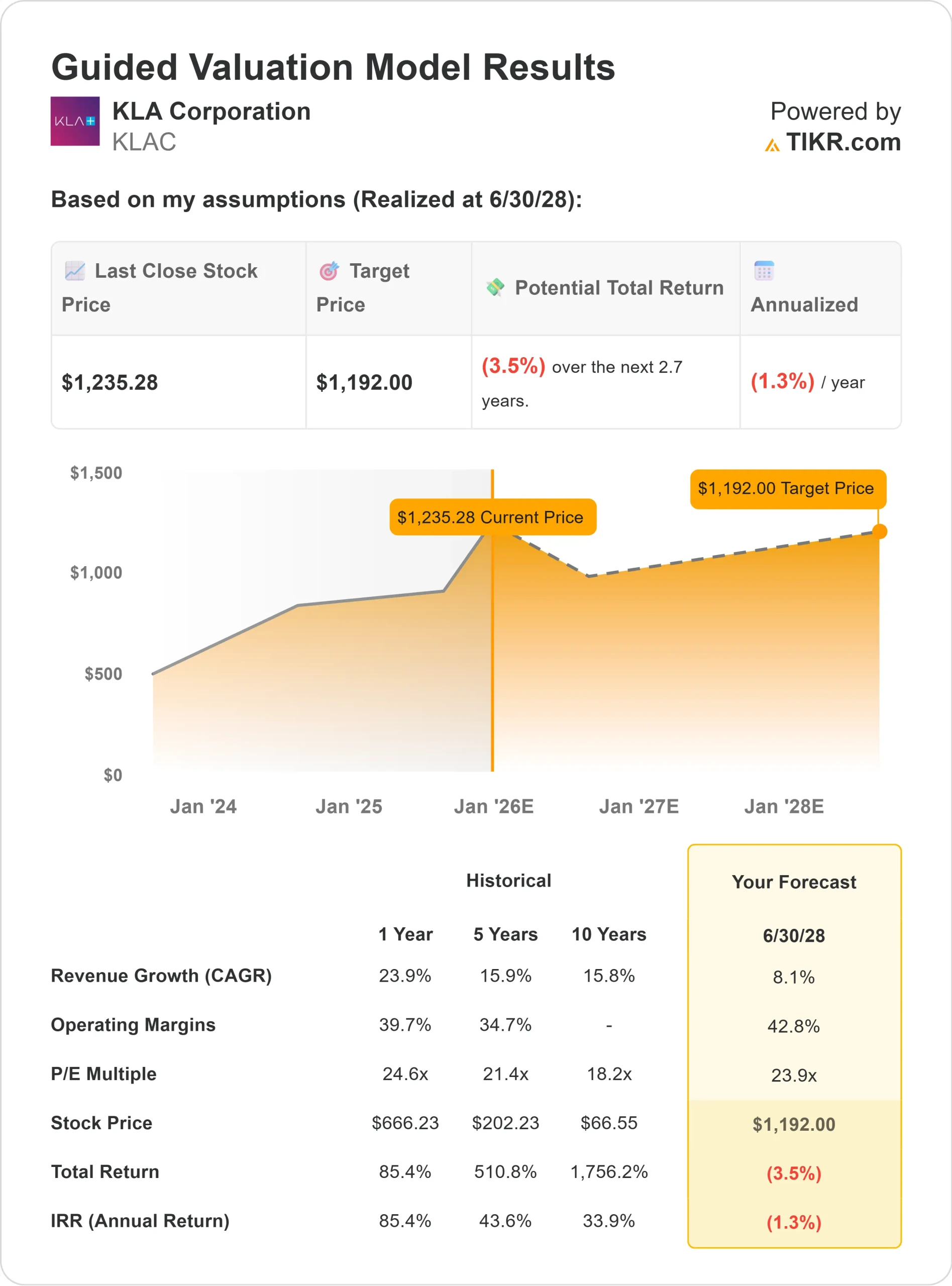

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23.9x forward P/E suggests ~$1,192/share by mid-2028.

- That implies about a 3% total decline, or roughly flat annualized returns from current prices.

For investors, this means KLA now fits the mold of a high-quality compounder rather than a high-upside growth story. The business continues to generate exceptional free cash flow and maintains deep partnerships with leading chipmakers, but with margins and valuations near peak levels, the stock looks more like a steady long-term hold than a near-term opportunity.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

KLA remains a core supplier in the semiconductor manufacturing chain, specializing in process control and inspection systems that ensure chip yield and quality. As AI, cloud computing, and high-performance logic chips drive wafer complexity, KLA’s equipment has become even more critical to chipmakers like TSMC, Samsung, and Intel.

Management continues to invest heavily in R&D to maintain its technology lead, while expanding its services and software business to create more recurring revenue. Free cash flow remains strong, supporting both dividend growth and buybacks.

For investors, these strengths suggest KLA is well positioned to sustain high margins and consistent earnings even as industry spending cycles fluctuate.

Bear Case: Valuation and Market Cycles

Even with these positives, valuation remains a concern. The stock trades near record highs and at a premium to peers after an extended rally. If wafer fab equipment spending cools or AI-related demand normalizes, KLA’s earnings growth could flatten.

Competition from Applied Materials and Lam Research is also intensifying, particularly in inspection and metrology tools where technology cycles move quickly. Any slowdown in customer orders or pricing pressure could weigh on results.

For investors, the risk is that even a small pullback in demand could pressure the stock’s premium multiple, limiting near-term returns.

Outlook for 2028: What Could KLA Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23.9x forward P/E suggests KLA could trade near $1,192/share by mid-2028. That represents roughly a 3% total decline, or about flat returns over the next few years.

While the company’s profitability and market leadership remain exceptional, much of that strength already appears priced in. For stronger upside, KLA would need to outperform expectations through new inspection technologies or a broader rebound in semiconductor capital spending.

For investors, KLA looks like a dependable long-term compounder built on steady cash flow and operational excellence, but with limited room for multiple expansion in the near term.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>