Marvell Technology, Inc. (NASDAQ: MRVL) trades near $89/share, well below its 52-week high of $127. The stock has cooled off in 2025 as investors balance short-term chip cycle softness with long-term growth potential in AI and cloud infrastructure.

Recently, Marvell reported quarterly results that highlighted solid progress in its data center and networking segments, driven by increasing AI-related demand. Management emphasized continued design wins in cloud and optical connectivity, setting the stage for stronger growth as hyperscale customers expand their AI capacity.

This article looks at where Wall Street expects Marvell to trade by 2028, based on consensus forecasts and TIKR’s Guided Valuation Model. These figures reflect analyst estimates, not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

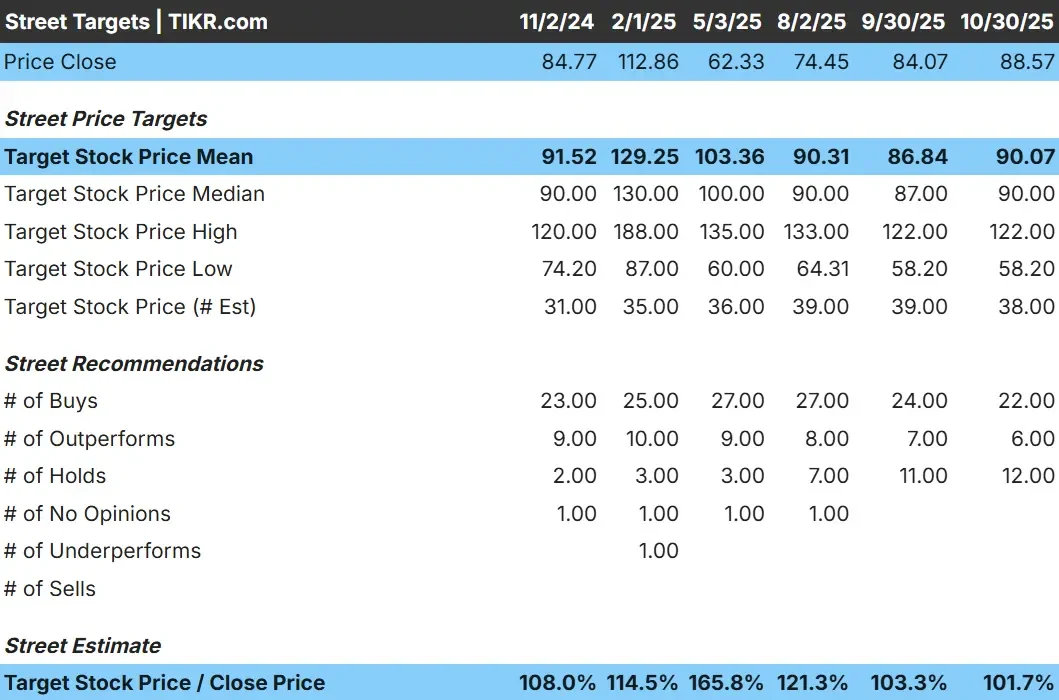

Analyst Price Targets Suggest Fair Value

Marvell trades around $89/share today. The average analyst price target is $90/share, suggesting the stock is fairly priced at current levels. Forecasts show a wide range and highlight mixed sentiment:

- High estimate: ~$122/share

- Low estimate: ~$58/share

- Median target: ~$90/share

- Ratings: 22 Buys, 6 Outperforms, 12 Holds

For investors, this range shows that the near-term upside is limited, but several analysts expect a stronger recovery once AI infrastructure demand picks up again. Marvell’s long-term positioning remains attractive, even if the next few quarters stay uneven.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

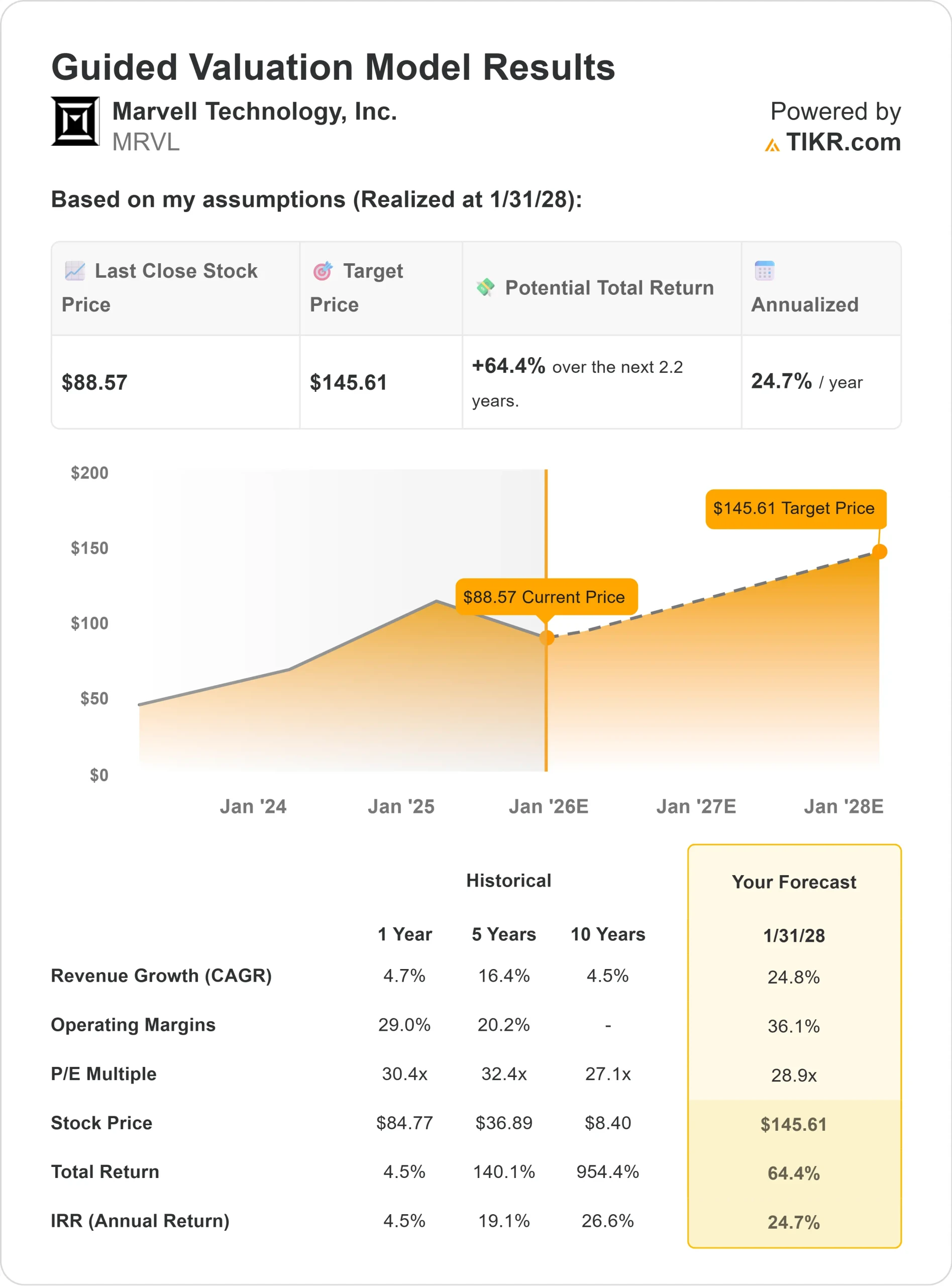

Marvell Technology: Growth Outlook and Valuation

Marvell’s fundamentals point to healthy long-term compounding potential:

- Revenue growth: ~25% annually through 2028

- Operating margins: ~36%

- Forward P/E: ~29x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 29x forward P/E suggests ~$146/share by 2028.

- That implies about 64% total returns, or roughly 25% annualized.

For investors, this outlook signals that Marvell could be one of the more promising AI infrastructure plays. Its deep partnerships with hyperscale cloud providers and leadership in custom silicon make it a credible compounder as AI adoption accelerates.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Marvell plays a key role in enabling AI and cloud computing. Its chips handle the fast data transfer and connectivity that power hyperscale data centers. As companies like Amazon, Microsoft, and Google expand their AI workloads, Marvell’s design wins continue to grow.

The company’s product mix is shifting toward higher-margin AI and optical networking solutions, which boosts profitability. Management’s commitment to innovation and its long-term customer relationships also add visibility.

For investors, this combination of growth, execution, and structural demand gives Marvell strong potential to compound earnings steadily over the next several years.

Bear Case: Cyclicality and Competition

Even with its strengths, Marvell remains tied to the broader semiconductor cycle. Periods of weaker capital spending or slower enterprise demand could affect results.

The stock’s valuation near 29x forward earnings assumes consistent execution. Competition from Broadcom, Nvidia, and AMD remains intense as each pursues the same high-growth markets. Any slowdown in AI orders or pricing pressure could limit near-term returns.

For investors, the main risk is timing. Marvell’s long-term story is solid, but quarterly volatility should be expected as chip spending normalizes.

Outlook for 2028: What Could Marvell Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 29x forward P/E suggests Marvell could reach around $146/share by 2028.

That represents about 64% total returns, or roughly 25% annualized.

While this forecast already includes some optimism, Marvell’s position in AI data centers and custom silicon provides a credible path to those returns. If management continues expanding design wins and improving profitability, the stock could outperform current expectations.

For investors, Marvell looks like a high-quality semiconductor compounder with meaningful long-term potential. Short-term noise aside, its exposure to AI and cloud infrastructure makes it one of the more compelling growth opportunities heading into 2028.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>