AT&T Inc. (NYSE: T) remains one of the market’s most dependable dividend names. Shares trade near $25/share, with analysts expecting steady returns as the company focuses on improving margins and paying down debt.

Recently, AT&T reported third-quarter results that showed steady progress in its core wireless and fiber businesses. The company continued to grow its subscriber base and generate strong cash flow, reaffirming its full-year outlook and commitment to reducing debt despite a slight revenue miss.

This article explores where Wall Street analysts think AT&T could trade by 2027. We have pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

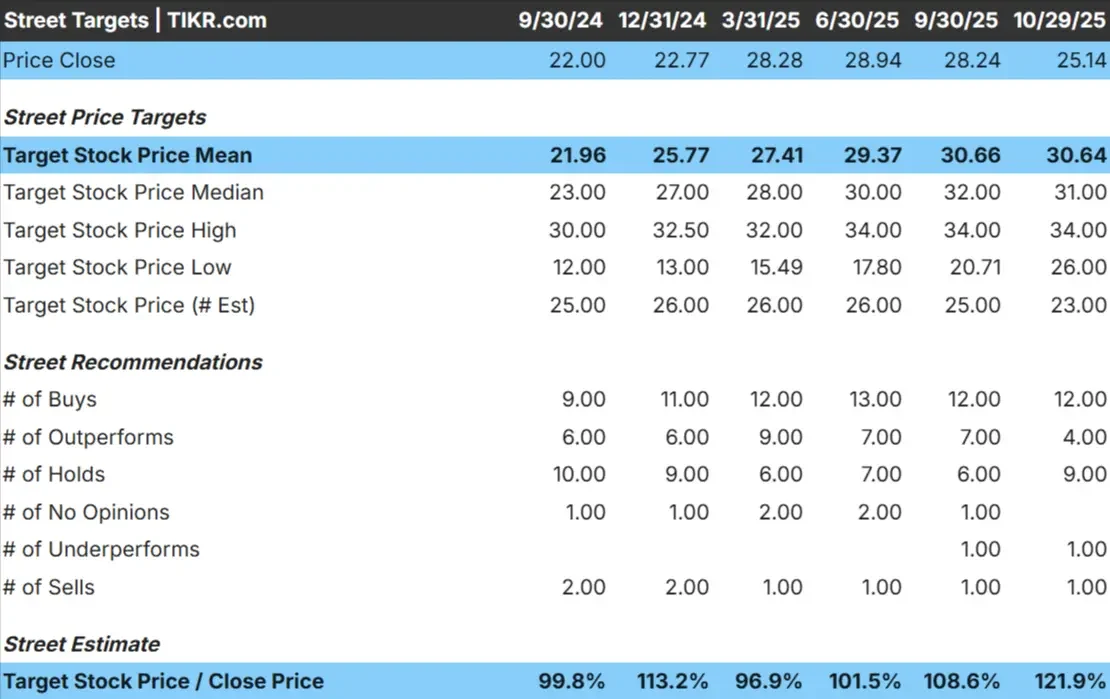

AT&T trades at about $25/share today. The average analyst price target is $31/share, which points to roughly 24% upside. Forecasts show a relatively tight range and reflect cautious optimism from Wall Street:

- High estimate: ~$34/share

- Low estimate: ~$26/share

- Median target: ~$31/share

- Ratings: 12 Buys, 4 Outperforms, 9 Holds, 1 Underperform, 1 Sell

Most analysts view AT&T as fairly valued but stable. For investors, that means the stock could deliver small but steady gains, supported by consistent cash flow and one of the most dependable dividend payouts in the market.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

AT&T: Growth Outlook and Valuation

The company’s fundamentals appear steady, though not particularly strong:

- Revenue is projected to grow about 2% annually through 2027

- Operating margins are expected to stay near 21%

- Shares trade at roughly 11x forward earnings, slightly below peers

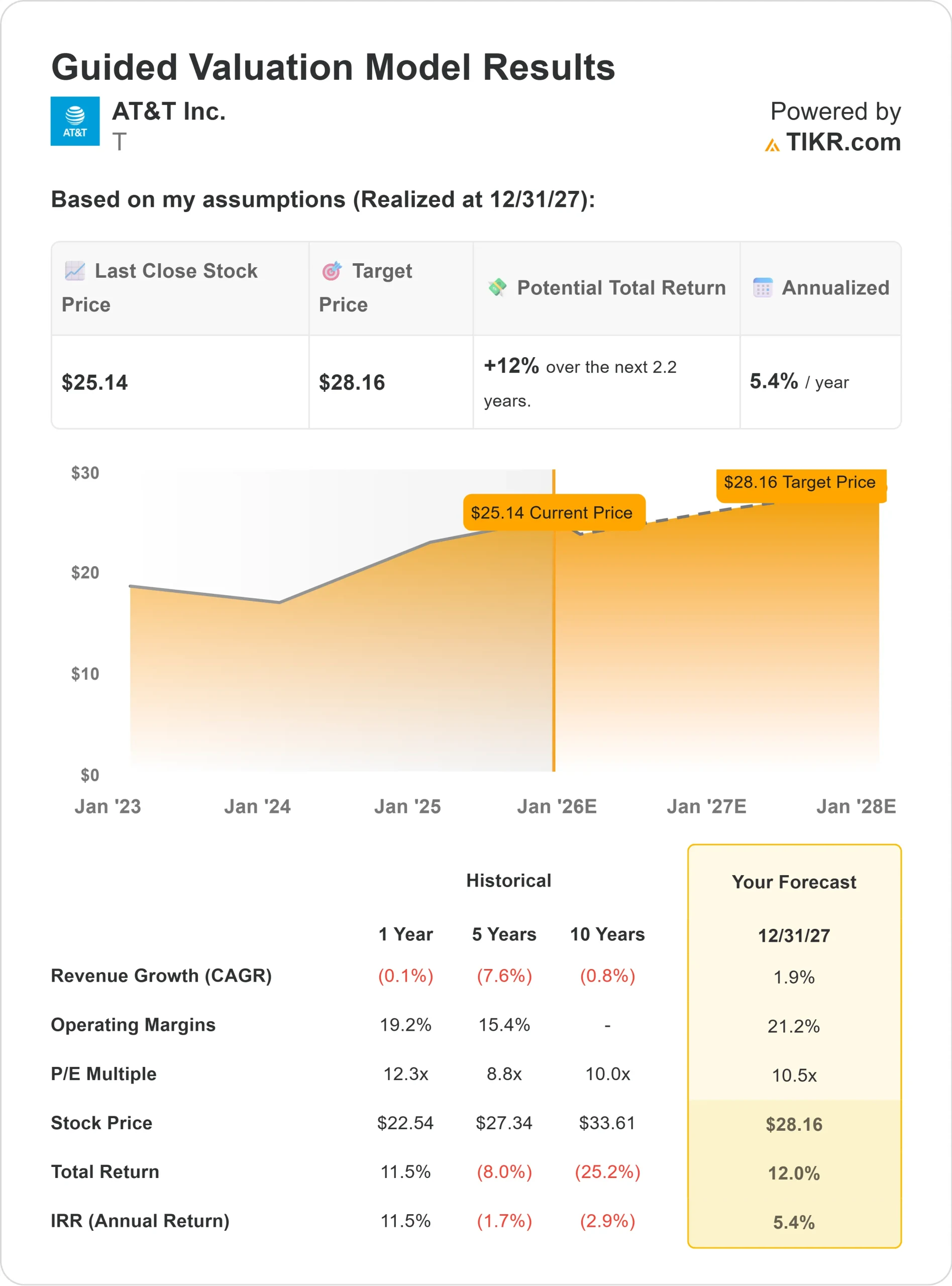

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 10.5x forward P/E suggests ~$28/share by 2027

- That implies about 12% total returns, or roughly 5% annualized

These figures suggest AT&T can deliver consistent returns, but not rapid growth. The stock looks fairly valued for a mature business, meaning upside depends on continued margin improvement and disciplined cash flow execution.

For investors, AT&T stands out as a stable income play with limited downside, supported by reliable free cash flow and steady dividend payouts.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

AT&T’s transformation strategy is starting to show results. The company continues to invest in 5G and fiber infrastructure, strengthening its recurring revenue base. Management’s focus on efficiency and cash generation supports ongoing debt reduction and dividend stability.

For investors, these strengths point to a leaner and more predictable business. The upside may not be dramatic, but AT&T’s consistent execution and improving financial flexibility make it a solid choice for income-focused portfolios.

Bear Case: Growth Constraints and Valuation

Even with improving execution, growth remains limited. Revenue is expected to rise modestly, and competition across telecom could pressure pricing. The stock currently trades near 11x forward earnings, a level that already reflects its slow but steady profile.

For investors, this means expectations should stay measured. If subscriber momentum slows or costs rise faster than expected, returns could flatten. AT&T’s reliability comes at the cost of big upside potential, making it best suited for steady dividend income rather than capital appreciation.

Outlook for 2027: What Could AT&T Be Worth?

Based on analysts’ average estimates and valuation models, AT&T could trade near $28/share by 2027, representing about 12% total returns or roughly 5% annualized gains.

For investors, this supports a long-term “steady compounding” outlook. AT&T’s strong free cash flow, healthy dividend, and improving balance sheet make it a dependable income stock, but not a high-growth opportunity.

Those seeking reliability and yield are likely to find AT&T a solid long-term hold within a diversified portfolio.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>