Marks & Spencer Group plc (MKS) has staged one of the most notable turnarounds in UK retail. Once viewed as a legacy brand in decline, the 140-year-old retailer has rebuilt its foundation on efficiency, quality, and customer trust. The result is a revitalized business that blends its heritage of dependability with a modern operating mindset, capable of delivering consistent profitability across food, fashion, and home categories.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)

The company’s transformation under CEO Stuart Machin has centered on simplicity, greater pricing transparency, tighter inventory management, and streamlined sourcing. Food remains its anchor, but the resurgence of Clothing & Home has been the clearest signal that M&S’s recovery runs deeper than cost-cutting. By upgrading stores, accelerating e-commerce integration, and emphasizing “trusted value” rather than discounting, the company has regained market share and re-energized its brand perception.

Today, M&S stands as a case study in how disciplined execution can restore both margins and investor confidence. Its renewed focus on capital allocation, digital expansion, and product innovation has created a platform for sustainable growth heading into 2026. What was once a short-term turnaround now looks increasingly like a long-term reinvention, one built to withstand shifting consumer habits and competitive pressures alike.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

For the fiscal year ended March 30, 2025, Marks & Spencer reported a 22% rise in operating profit to £1.07 billion, up from £875 million a year earlier. Group revenue climbed 9% year-on-year to £13.1 billion, marking the third straight year of growth across both Food and Clothing & Home. Net profit reached £819 million, up from £654 million, as gross margin expansion in clothing and ongoing volume gains in food offset inflationary headwinds.

| Metric | FY 2025 | Change (YoY) | Notes |

|---|---|---|---|

| Revenue | £13.1 B | +9% | Third consecutive year of growth |

| Operating Profit | £1.07 B | +22% | Driven by margin improvement |

| Net Profit | £819 M | +25% | Strong contribution from Clothing & Home |

| Food Sales | £8.4 B | +8% | Higher volumes and premium mix |

| Clothing & Home Sales | £4.7 B | +9% | Increased full-price sales |

| Return on Equity (IFRS) | 20.6% | +4 pts | Highest in a decade |

| Solvency II ROE | 16.7% | +2 pts | Reflects a leaner balance sheet |

| Interim Dividend | 13.1 p | +10% | Third straight increase |

| Net Debt | £2.1 B | −12% | Supported by cash flow growth |

M&S’s Food division remained the cornerstone of growth, delivering an 8% increase in sales and higher basket sizes despite cautious consumer spending. Its Clothing & Home division, historically the brand’s Achilles’ heel, posted a 9% rise in sales and a 60-basis-point improvement in margin, reflecting stronger full-price sell-through and more precise inventory management.

The company’s Solvency II return on equity rose to 16.7%, while IFRS return on equity reached 20.6%, underscoring better capital efficiency and cash conversion.

Management also declared a 10% increase in the interim dividend to 13.1p per share, the third consecutive hike since reinstating payouts. While the acquisition of Direct Line was completed in July and has not yet been consolidated into results, the deal signals M&S’s intent to diversify earnings and capture more lifestyle-adjacent markets over time.

Look up Marks & Spencer’s full financial results & estimates (It’s free) >>>

Broader Market Context

UK retail has weathered an unusually volatile cycle, from pandemic closures to inflation peaks and now a fragile recovery. Yet amid the turbulence, M&S has managed to gain share in both grocery and apparel. Consumers are selectively trading up, prioritizing quality and trusted brands over low-cost volume. M&S’s focus on “trusted value,” offering premium quality at affordable prices, has hit that sweet spot.

Digitally, the brand is making quiet but meaningful progress. Online now accounts for roughly 40% of Clothing & Home sales, aided by improved logistics and faster delivery windows. Its joint venture with Ocado in online grocery continues to mature, giving M&S exposure to one of the UK’s few scalable digital food platforms. Combined, these shifts position the company to capture a more balanced mix of store and e-commerce growth through 2026.

1. Clothing & Home Find Its Footing

After years of decline, M&S’s clothing segment is finally back in fashion, literally and figuratively. The business reported 9% sales growth and improved margins as it embraced a sharper brand identity, curated assortments, and better price architecture. Its new approach to womenswear and active lines helped reduce markdown dependency while lifting customer retention.

Store modernization has also been critical. New-format stores in Leeds, Liverpool, and Manchester are outperforming legacy locations by double digits, proving that refreshed layouts can drive cross-category spending. This shift is turning M&S’s once-stale clothing arm into a profit driver again, with management hinting at further margin upside if cost discipline continues.

2. Food Keeps Feeding the Growth

M&S Food remains the company’s competitive anchor, delivering consistent mid-single-digit growth even as rivals struggle with volume erosion. Its strategy of blending everyday essentials with premium ready-to-eat offerings has struck a chord with inflation-weary consumers looking for affordable indulgence.

The company has expanded its in-store footprint for fresh and convenience items while leveraging Ocado’s digital platform to reach new customers online. With basket sizes and frequency both rising, M&S is proving it can win on both quality and convenience. Management sees room for further growth in suburban and travel hubs, where M&S’s smaller store formats can outperform peers on return per square foot.

Value stocks like Marks & Spencer in less than 60 seconds with TIKR (It’s free) >>>

3. Execution, Efficiency, and Expansion

Beyond sales growth, the quiet story at M&S is execution. Supply-chain efficiency and data-driven replenishment have improved product availability and reduced markdowns. Inventory days have been cut significantly, freeing up capital and improving margins.

Internationally, M&S is expanding more cautiously but effectively, entering joint ventures in markets like India and the Middle East, where its brand equity is strong and local partners share the risk. With debt down and cash generation solid, M&S now has optionality to reinvest in digital, accelerate store refreshes, and maintain shareholder returns without over-levering the balance sheet.

The TIKR Takeaway

Marks & Spencer’s turnaround is no longer theoretical, it’s showing up in the numbers. The combination of margin expansion, digital scale, and a leaner balance sheet suggests that the transformation has entered a sustainable phase. Book value and free cash flow are both trending higher, and management’s focus on “trusted value” remains a durable moat in an unpredictable consumer market.

For investors, the 2025 results validate the recovery thesis but also raise the bar for what comes next. Execution will determine whether M&S can transition from turnaround to compounder status. If cost control and digital momentum hold through 2026, a rerating toward mid-teens earnings multiples seems justified.

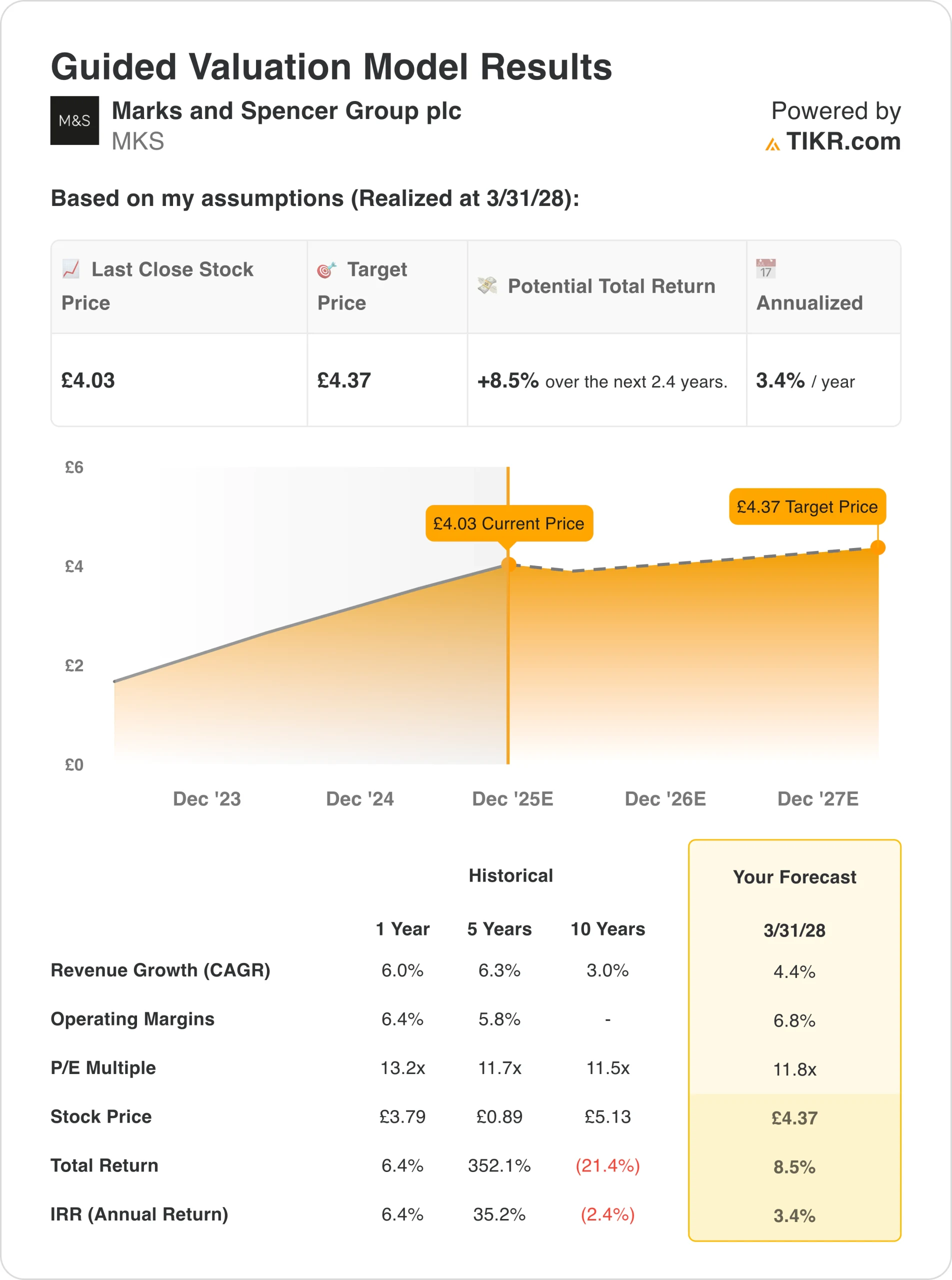

Should You Buy, Sell, or Hold Marks & Spencer Stock in 2025?

M&S shares have rallied over 30% in the past year, pricing in much of the near-term turnaround success. But with structural tailwinds in both food and fashion and a disciplined management team steering toward sustainable margins, long-term investors may still find room for further upside as the story shifts from recovery to reinvestment.

How Much Upside Does Marks & Spencer Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!