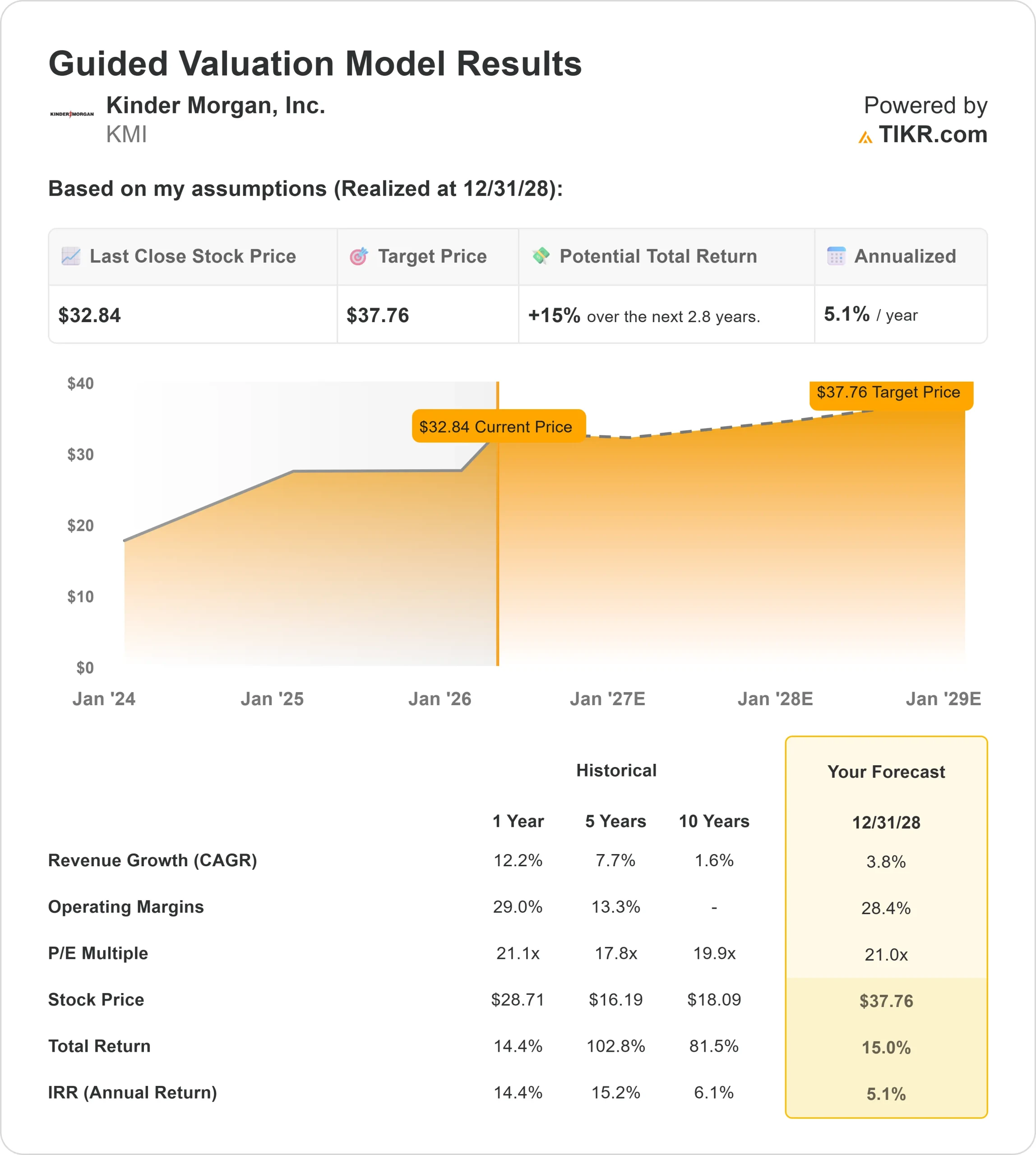

Key Stats for KMI Stock

- Year-to-Date Performance: 23%

- 52-Week Range: $24 to $34

- Valuation Model Target Price: $38

- Implied Upside: 15%

Analyze your favorite stocks like Kinder Morgan with TIKR (It’s free) >>>

What Happened?

Kinder Morgan stock is up about 23% year to date, recently trading near $34 per share, as investors increasingly focus on a major shift in U.S. energy demand.

The market narrative has centered on rising natural gas consumption driven by LNG exports, electricity demand from AI data centers, and the ongoing shift from coal to gas, all of which require more pipeline infrastructure to move fuel across the country.

The stock has moved higher this year primarily because investors are pricing in stronger long-term earnings as demand for natural gas transportation increases and pipeline capacity tightens across the U.S.

This trend is also reflected across peers like Williams Companies and Energy Transfer, as investors re-rate pipeline operators that benefit from rising natural gas volumes and improving infrastructure utilization.

Recent institutional activity has reinforced this trend, with firms like Holocene Advisors initiating a $78 million position, Focus Partners Wealth increasing its stake to about $127 million, and Mirabella Financial Services boosting its holdings by 145%, while overall institutional ownership remains high at roughly 63%, signaling sustained demand for shares.

Analyst sentiment remains largely neutral, with Scotiabank raising its price target to $31 from $30 while maintaining a sector perform rating, while the broader consensus target sits near $33 with a near-even split between Buy and Hold ratings.

Additional positioning updates show Gotham Asset Management increasing its stake by about 4% to roughly $28 million, while MIRAE Asset Global ETFs trimmed its position slightly to about $244 million, reflecting selective positioning across the sector.

At the same time, a small insider sale saw VP Michael Garthwaite sell 1,550 shares at $33.30, a limited transaction that did not materially impact overall sentiment.

This month at the Raymond James Institutional Investor Conference, Kinder Morgan highlighted its strong growth outlook, noting a $10 billion project backlog expected to generate over $500 million in incremental annual EBITDA.

Management also pointed to tightening pipeline capacity, with utilization rising to 90% in 2025 from 74% in 2016 and contract terms extending to 7 to 8 years, as executive David Michels said “we move about 40% of all of the natural gas molecules that are produced in the U.S.,” reinforcing the company’s scale advantage as LNG exports, power demand, and data center growth increase demand for pipeline infrastructure.

Value Kinder Morgan instantly (Free with TIKR) >>>

Is KMI Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 3.8%

- Operating Margins: 28.4%

- Exit P/E Multiple: 21.0x

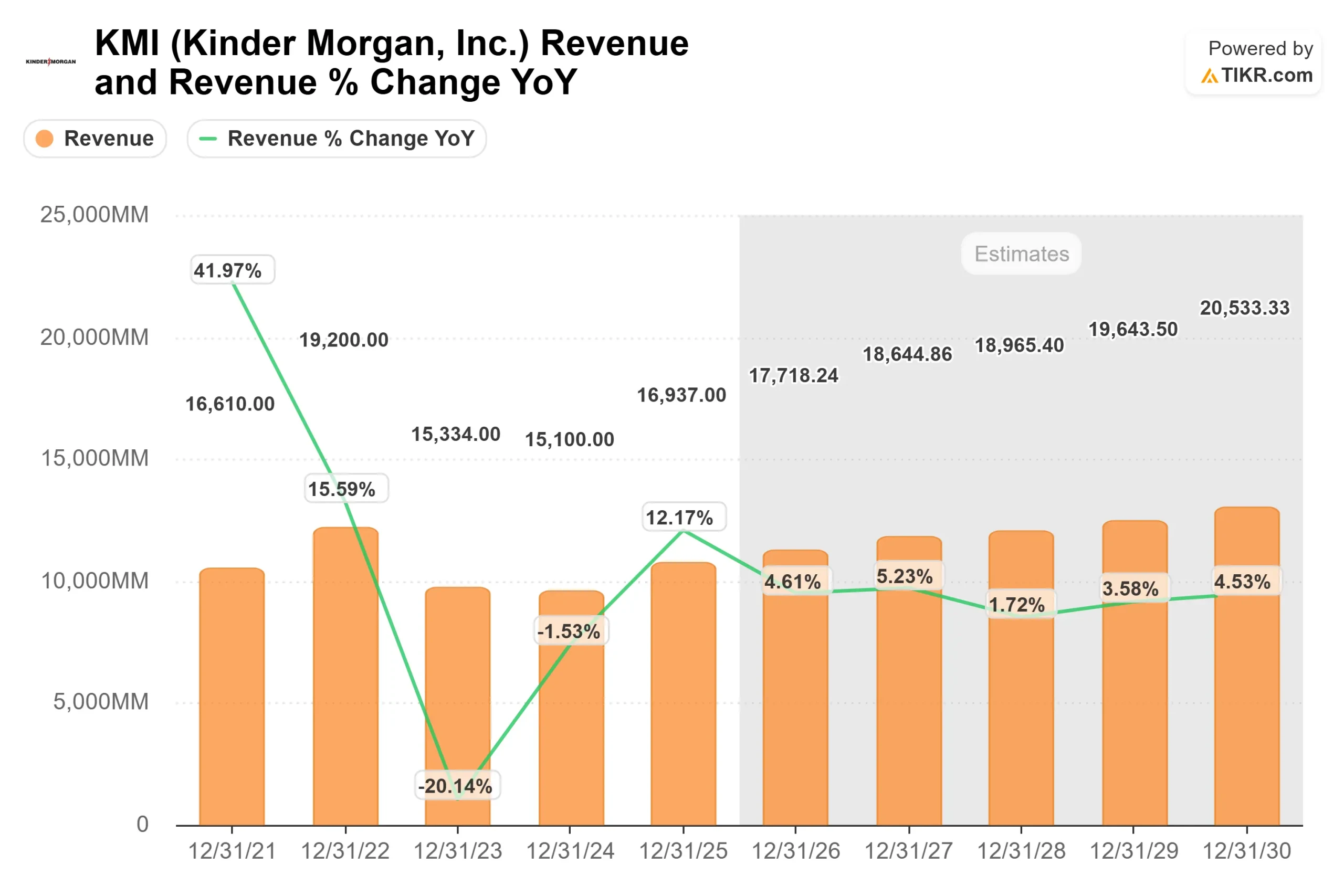

Growth is expected to remain steady as rising natural gas demand increases volumes moving through Kinder Morgan’s pipeline network, particularly from LNG exports and electricity generation.

See analysts’ growth forecasts and price targets for Kinder Morgan (It’s free) >>>

Margins are supported by the company’s fee-based model, where customers pay for pipeline capacity regardless of usage, allowing higher volumes to translate into predictable cash flow without reliance on commodity prices.

Future performance is tied to expanding pipeline capacity and higher utilization rates, where tighter infrastructure supply allows Kinder Morgan to secure longer-term contracts at improved pricing, supporting incremental EBITDA growth.

Peers such as Williams Companies and Energy Transfer are seeing similar demand tailwinds, but Kinder Morgan’s larger pipeline network provides a scale advantage in capturing new projects tied to LNG and power demand growth.

At current levels, Kinder Morgan appears modestly undervalued, with future returns driven by rising gas volumes, improving pricing power, and continued expansion of U.S. energy infrastructure.

How Much Upside Does KMI Stock Have From Here?

Investors can estimate Kinder Morgan potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Kinder Morgan in under 60 seconds with TIKR (It’s free) >>>