Key Stats for Axcelis Stock

- Past-Week Performance: +1.5%

- 52-Week Range: $40.4 to $102.9

- Current Price: $84.4

What Happened?

Axcelis Technologies (ACLS), a maker of ion implantation equipment used to manufacture semiconductors, posted Q4 revenue of $238.3 million against a $215 million consensus, while its CS&I aftermarket business (customer support and infrastructure services that generate high-margin recurring revenue) hit a quarterly record of $82 million, even as the stock trades at $84.43, down sharply from its 52-week high of $102.93.

Axcelis reported non-GAAP diluted EPS of $1.49 on February 17, beating the $1.12 consensus by 33%, while non-GAAP gross margin reached 47.3% against a 43% outlook, driven by a surge in high-margin CS&I upgrades including a customer conversion of silicon carbide tools from 150mm to 200mm wafers using the Purion Power Series+, a platform that allows chipmakers to upgrade capacity within the same physical footprint.

Meanwhile, CS&I revenue grew 14% year-over-year in 2025 and the company delivered a record in system upgrades and services, generating $107 million in full-year free cash flow despite lower overall revenue, a combination that rivals in the semiconductor equipment peer group have struggled to replicate during the same cyclical digestion period.

On March 13, Axcelis named David Ryzhik, previously Senior Vice President of Investor Relations and Corporate Strategy, as interim CFO after James Coogan departed to pursue a CFO role at a public company in a different industry, with Coogan remaining through April 24 to support the transition while the company conducts a formal search.

Russell Low, President and CEO, stated on the Q4 2025 earnings call that “we secured an order for a high current system from a leading North American memory manufacturer, which is an important customer win that broadens our presence beyond our strong position in Korea,” a development that widens Axcelis’s addressable DRAM base ahead of a capital-intensive memory expansion cycle.

Furthermore, SK Hynix’s Yongin cluster alone targets four mega-fabs at 200,000 wafer starts per week with equipment orders expected into 2027, while a $110 million buyback authorization and a pending merger with Veeco, expected to close in the second half of 2026, anchor the multi-year return case.

Wall Street’s Take on ACLS Stock

The Q4 beat and record CS&I revenue confirm the aftermarket flywheel is intact even as new system orders remain soft, directly supporting the TIKR model’s assumption that revenue troughs in 2026 before the DRAM-driven recovery pushes revenue to $0.9 billion in 2027.

The 2026 earnings setup looks worse before it gets better: normalized EPS is expected to contract 25.4% to $3.64, driven by a less favorable product mix and tariff headwinds below 100 basis points, but the 2027 estimate of $4.51 per share implies 23.9% EPS growth as new DRAM fab capacity, specifically SK Hynix’s Yongin cluster targeting 200,000 wafer starts per week, comes online.

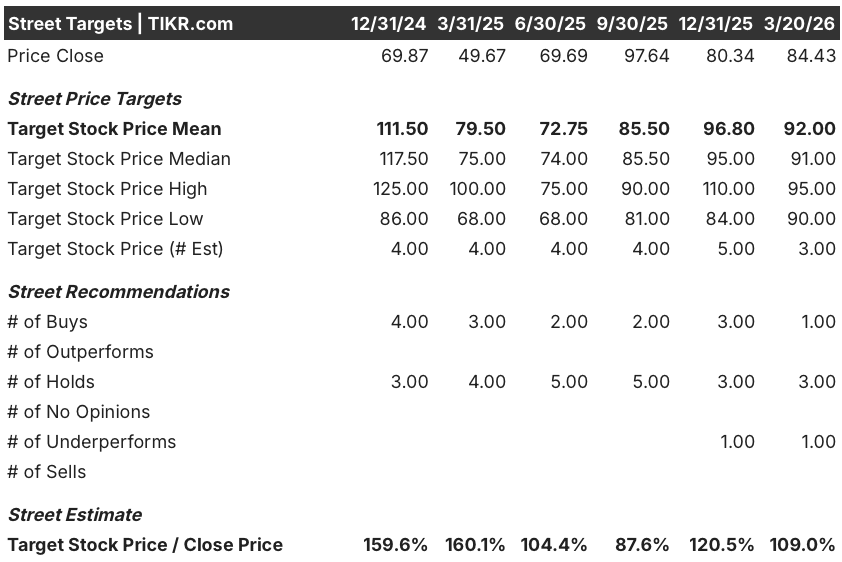

Wall Street’s caution appears poorly timed given that DRAM bookings accelerated sequentially in Q4, a North American memory customer placed an order before an evaluation even completed, and management has explicitly guided for memory-led revenue acceleration into 2027: of 5 analysts covering ACLS as of March 20, only 1 rates it a buy, 3 hold, and 1 underperforms, with a mean price target of $92 implying just 9% upside from $84.43.

The Street’s $90 to $95 analyst target range spans just $5, a compression that reveals analysts anchoring to near-term EPS weakness rather than the multi-year DRAM capacity buildout already confirmed in public fab announcements.

What Does the Valuation Model Say?

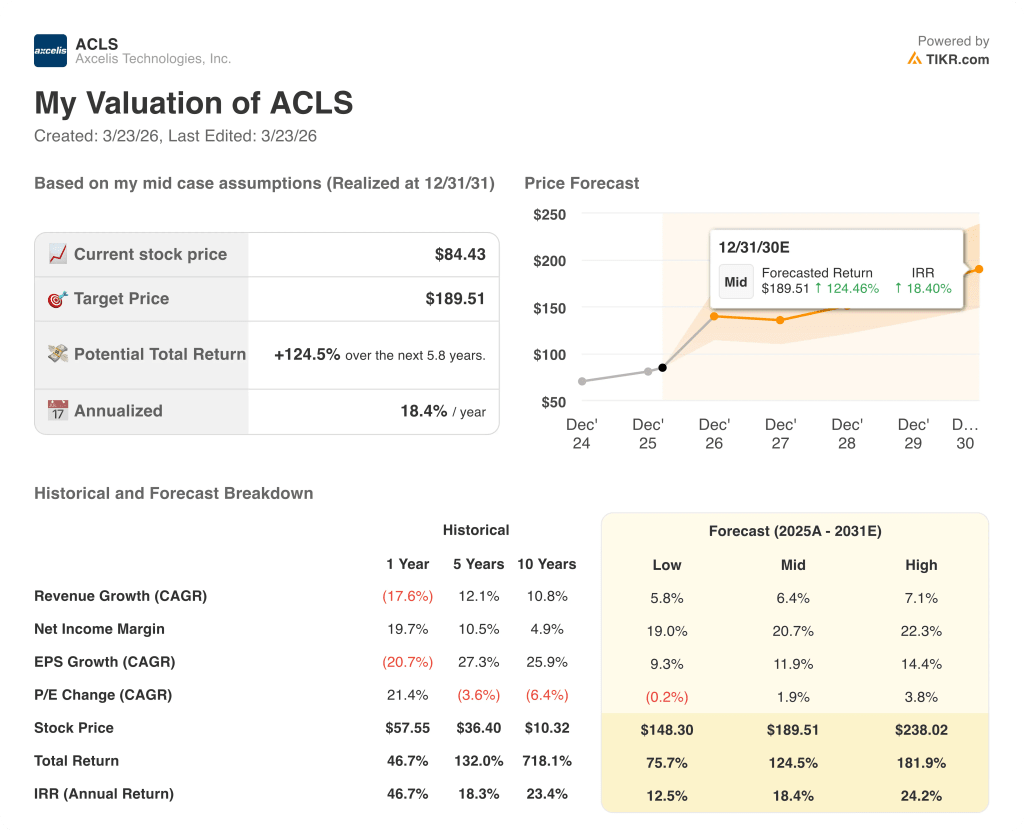

The TIKR mid-case target of $189.51, representing 124.5% total return and an 18.4% IRR through December 2030, rests on an 11.9% EPS CAGR and a 20.7% net income margin assumption, both of which are grounded in the DRAM ramp, CS&I expansion, and the Veeco merger unlocking new revenue streams across complementary semiconductor process equipment.

The market is mispricing a trough-year P/E of 21x as a ceiling, ignoring that the last DRAM revenue cycle peak generated $90 million before Axcelis even had the North American memory customer now on its roster.

The TIKR $189.51 mid-case target requires the DRAM recovery to translate into measurable systems revenue in 2027, a development already supported by multi-quarter customer forecasts management described as “very sound” on the February 17 earnings call.

The North American memory manufacturer order, received before an existing system evaluation was complete, signals Axcelis is gaining share in high current tools at the precise moment DRAM wafer start capacity is about to inflect upward.

The Veeco merger close, expected in the second half of 2026 pending final Chinese regulatory approval, is the single execution risk that, if delayed materially, removes the revenue synergy assumptions embedded in the long-end of the TIKR model.

The Q1 2026 earnings release is the number to watch: a memory systems revenue contribution above the implied trough, or any acceleration in bookings beyond the $128 million Q4 level, would confirm the DRAM recovery is tracking ahead of the flat-revenue 2026 consensus.

Should You Invest in Axcelis Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ACLS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Axcelis Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ACLS stock on TIKR for Free →