Key Stats for Emerson Stock

- Past-Week Performance: -3.1%

- 52-Week Range: $90.1 to $165.2

- Current Price: $128.2

What Happened?

Automation orders at Emerson Electric (EMR), the St. Louis industrial technology company focused on process control and factory software, surged 9% in fiscal Q1 while the stock sits 22% below its 52-week high of $165.15, creating a widening gap between operational momentum and a share price of $128.15 that has yet to reflect it.

Emerson reported fiscal Q1 adjusted EPS of $1.46 on February 3, beating the IBES consensus of $1.41, and raised the floor of its fiscal 2026 adjusted EPS guidance to $6.40 from $6.35, citing sustained demand across power generation, liquefied natural gas infrastructure, and semiconductor manufacturing.

Ovation, Emerson’s power-plant control software that manages electricity generation at data centers and utility facilities, posted order growth of 74% in Q1, including a win to automate a new 1.7-gigawatt AI data center in the U.S., and the company’s $7.9 billion backlog, up 9% year-over-year, now underwrites the 6% underlying sales growth guided for the second half.

COO Ram Krishnan stated at the J.P. Morgan Industrials Conference on March 17 that “our project pipeline, $11 billion, almost $6.4 billion in these growth verticals of life sciences, aerospace and defense, semi, LNG and power, all continue to move at the right pace and the right momentum,” directly corroborating the company’s second-half revenue acceleration thesis.

Emerson’s plan to deploy $6 billion in share repurchases through fiscal 2028, reach $8 in adjusted EPS, and grow its software business from $2.5 billion to $3.5 billion in annual revenue positions the company to compound returns well beyond the current multiple, supported by over 50% market share in global LNG control systems and a 315 million tons-per-annum LNG capacity wave still awaiting contract awards.

Wall Street’s Take on EMR Stock

The 9% Q1 order surge, paired with a raised EPS floor and $7.9 billion backlog up 9% year-over-year, directly supports the TIKR model’s assumption of 5.2% revenue growth to $18.96 billion in fiscal 2026 and acceleration to $20 billion in fiscal 2027.

TIKR estimates normalized EPS reaching $6.51 in fiscal 2026 and $7.18 in fiscal 2027, compounding at 7.8% annually through fiscal 2028, driven by the 40% incremental operating leverage Emerson has guided and its 240-basis-point adjusted segment EBITA margin expansion plan.

Emerson’s free cash flow is also forecast to grow from $2.67 billion in fiscal 2025 to $3.53 billion in fiscal 2026 and $4.34 billion by fiscal 2028, expanding margin from 14.8% to 20.6% as software mix rises and the AspenTech renewal headwind reverses.

Wall Street carries 14 buys, 3 outperforms, 9 holds, 1 underperform, and 1 sell on EMR, with a mean price target of $166.37 that implies 29.8% upside from $128.15, suggesting analysts broadly see the software renewal drag as temporary, not structural.

The $104 bear target reflects a scenario where China and European chemical weakness deepens and Middle East disruption extends through fiscal 2026; the $204.00 bull target requires the LNG order wave, the 315 million tons-per-annum still-to-be-awarded capacity, and power generation wins to accelerate shipments into fiscal 2027.

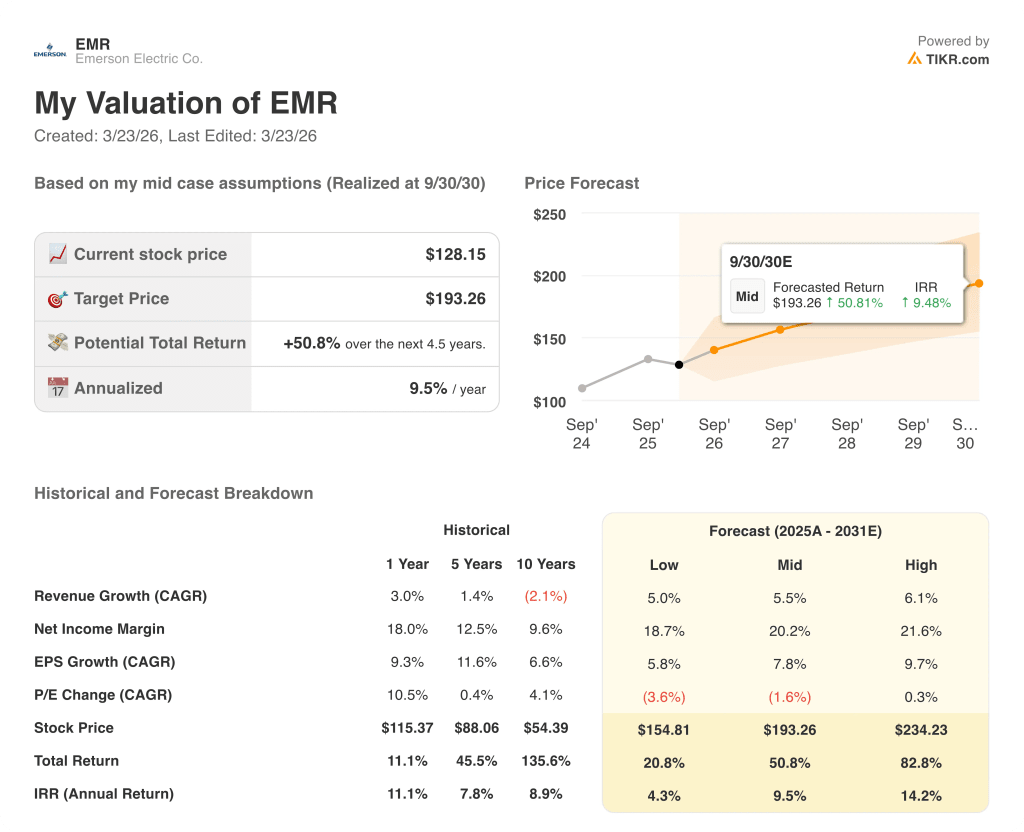

What Does the Valuation Model Say?

The TIKR mid-case price target of $193.26, implying a 50.8% total return at a 9.5% IRR over 4.5 years, assumes 5.5% revenue CAGR and net income margins expanding to 20.2%, both underwritten by the $11.1 billion project funnel and Ovation’s 74% Q1 order growth in the power generation market.

The market is pricing EMR as if the 22% price decline from $165.15 reflects a broken growth story, yet trailing 12-month orders of 6% and a book-to-bill of 1.13 make that read factually wrong.

The $7.9 billion backlog, phased to deliver the guided 6% second-half underlying sales acceleration, is the operational evidence that the TIKR model’s $193.26 target is grounded, not aspirational.

COO Ram Krishnan’s March 17 confirmation that orders continued at Q1 pace heading into fiscal Q2, even amid Middle East logistics disruption, signals the revenue trajectory is intact and the stock’s discount is a sentiment gap, not a fundamental one.

A sustained Middle East conflict beyond several weeks, where Emerson derives roughly 7% of total sales from Saudi Arabia, UAE, and Qatar, is the primary risk that breaks the second-half shipment phasing the TIKR model depends on.

Fiscal Q2 results, expected in early May, will reveal whether the guided $1.50–$1.55 adjusted EPS holds despite Middle East logistics strain; the number to watch is Intelligent Devices underlying sales growth, the segment most exposed to regional project execution.

Should You Invest in Emerson Electric Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EMR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Emerson Electric Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze EMR stock on TIKR for Free →