Key Stats for Dominion Stock

- Past-Week Performance: -6.1%

- 52-Week Range: $48.1 to $67.6

- Current Price: $59.4

What Happened?

Dominion Energy (D), a Virginia-based electric utility serving the world’s largest data center market, locked in nearly 48.5 GW of contracted data center capacity by December 2025, driving a 30% increase in its five-year capital plan to $64.7 billion.

On February 23, Dominion reported Q4 2025 operating earnings of $0.68 per share, beating the $0.67 LSEG consensus estimate, while full-year 2025 operating EPS of $3.42 landed above the guidance midpoint of $3.30, even as 2026 guidance of $3.45 to $3.69 per share missed the $3.60 Street consensus at the midpoint.

Weather-normal electricity sales in Dominion Energy Virginia, the company’s largest utility and home to the most concentrated data center market in the United States, rose 5.4% in 2025, with all top 20 peak demand days in the Dominion zone occurring within the prior 14 months, a demand acceleration no peer utility has matched at this scale.

Robert Blue, Chair, President and Chief Executive Officer, stated on the Q4 2025 earnings call “our forecasted data center demand through 2045 is more than covered by existing signed ESAs and CLOAs,” referring to Electrical Service Agreements and Construction Letters of Authorization, the binding contracts that obligate customers to minimum payments, a claim validated by the 1.4 GW pipeline expansion recorded between September and December 2025 alone.

Dominion’s reaffirmed 5% to 7% long-term EPS growth rate, now biased toward the upper half of that range from 2028 onward, rests on a $64.7 billion capital deployment plan, a February 13 PJM transmission award exceeding $5 billion, and a Coastal Virginia Offshore Wind project more than 70% complete and on track to deliver first power to the grid by the end of March.

Wall Street’s Take on D Stock

The $64.7 billion capital deployment plan Dominion announced on February 23, backing the data center demand surge already underway in Virginia, sets a direct path to normalized EPS of $4.63 by December 2030 from $3.42 in 2025.

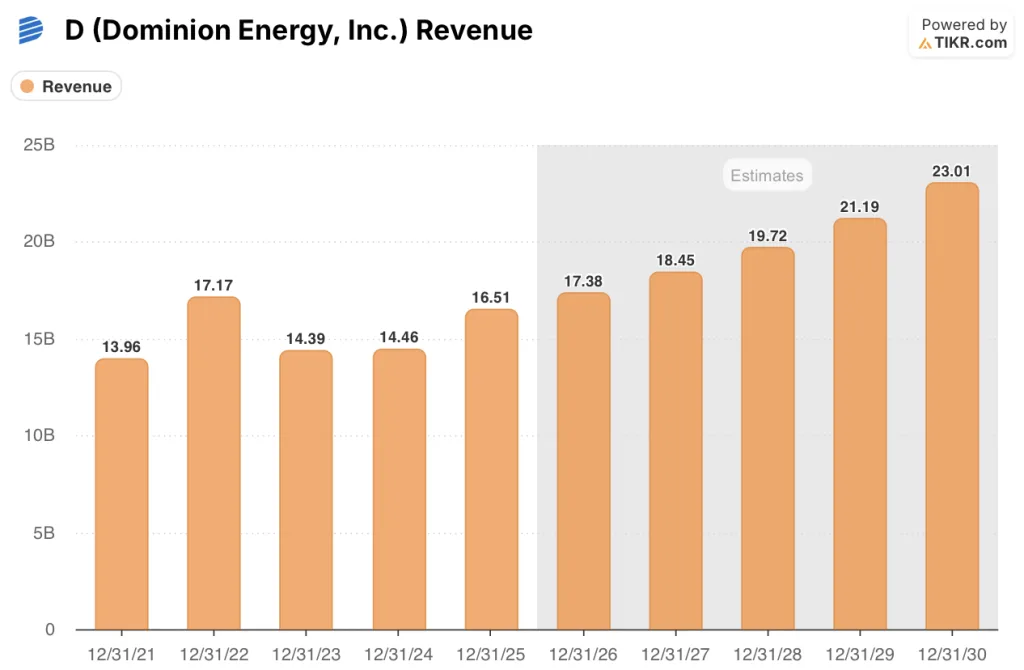

Revenue is forecast to grow from $16.5 billion in 2025 to $23.0 billion by 2030 at a 7.2% mid-case CAGR, while EBITDA margins, a measure of operating profitability before interest and taxes, expand from 47.9% to 56.8%, reflecting the high-margin nature of regulated rider recovery mechanisms covering nearly two-thirds of the capital plan.

Sixteen analysts currently cover Dominion with 2 buys, 1 outperform, 16 holds, and 1 sell, setting a mean price target of $65.63, implying approximately 10.5% upside from the March 20 close of $59.38, a cautious consensus anchored to near-term guidance softness rather than the multi-year capital cycle.

The spread between the Street’s low target of $59.00 and high of $69.00 reflects a binary read on two risks already named in the story: CVOW turbine installation delays that could add $150 million to $200 million per quarter beyond July 2027, and Millstone’s power purchase agreement expiration in August 2029.

What Does the Valuation Model Say?

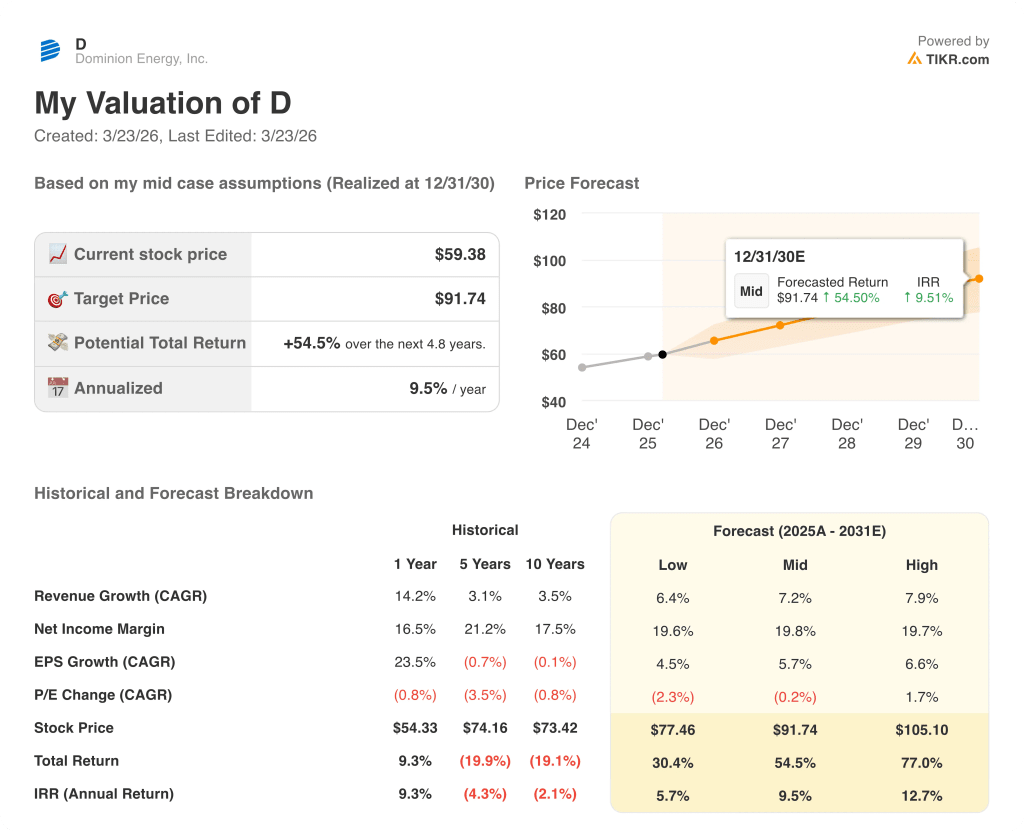

The TIKR mid-case target of $91.74 implies a 54.5% total return, driven by a 7.2% revenue CAGR and net income margin expansion from 18.0% to 19.8%, both grounded in the 48.5 GW contracted data center pipeline and the February 13 PJM transmission award exceeding $5 billion.

The Street prices Dominion as a slow-growth utility; the TIKR model prices it as a regulated capital compounder, and 5.4% weather-normal sales growth in 2025 supports the latter.

TIKR’s $91.74 target requires normalized EPS to reach $4.63 by 2030, a trajectory consistent with the company’s own 5%–7% guided EPS CAGR and the upper-half bias management signaled starting 2028.

Robert Blue’s confirmation that 20-plus years of data center demand is already covered by signed ESAs and CLOAs removes the single biggest execution risk bears cite against the capital plan.

CVOW turbine installation delays beyond July 2027 break the model: each additional quarter adds up to $200 million in project cost and pressures the credit metrics Dominion needs to fund the $64.7 billion plan at investment-grade spreads.

The South Carolina rate case decision expected in June, with rates effective in July, is the first near-term number to watch; a constructive ruling confirms the regulatory execution that underpins the upper-half EPS growth bias from 2028.

Should You Invest in Dominion Energy, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up D stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Dominion Energy, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze D stock on TIKR for Free →