Key Stats for Centene Stock

- Past-Week Performance: -0.2%

- 52-Week Range: $25.1 to $66

- Current Price: $34.4

What Happened?

Medicaid managed care’s biggest turnaround story of 2026 belongs to Centene (CNC), the government-focused insurer serving 1 in 15 Americans, which swung from a $6.67 billion net loss in 2025 to guiding for adjusted EPS above $3.00 this year, trading at $34.4 against a 52-week high of $66.03.

On February 6, CEO Sarah London confirmed a Q4 2025 adjusted diluted loss per share (the per-share net loss after accounting for all potential shares outstanding) of $1.19, beating the LSEG consensus of $1.22, as the company’s Medicaid health benefits ratio improved 190 basis points from its Q2 2025 trough of 94.9% to 93.0% by year-end.

Behavioral health, home care, and high-cost drugs drove mid-6s percent medical cost trend across Medicaid in 2025, but Centene’s ABA task force (a fraud and utilization unit targeting outlier providers in applied behavioral therapy) now runs 75 detection algorithms daily across a 29-state footprint, giving the company a measurable cost lever peers like Molina Healthcare, which forecast 2026 adjusted EPS of just $5 against a Street estimate of $13.76, have yet to demonstrate.

London also stated on the Q4 2025 earnings call that “if all we do is deliver a 93.7% in Medicaid, I will be very disappointed,” tying that challenge directly to the company’s pipeline of 2026 trend initiatives, including network optimization, clinical program rollouts, and expanded fraud litigation.

Centene’s planned March 25 redemption of $1 billion in 4.25% notes due 2027, funded through a PDP (prescription drug plan) receivable sale, accelerates its deleveraging ahead of peak policy uncertainty, and combined with a 40%-plus adjusted EPS growth target, a 3.5 million-member Marketplace stabilization, and a Medicare Advantage breakeven roadmap set for 2027, positions the company to rebuild toward the earnings power that justified a $66 stock less than a year ago.

Wall Street’s Take on CNC Stock

Centene’s Medicaid HBR improvement from 94.9% in Q2 2025 to 93.0% by year-end directly supports the 2026 normalized EPS estimate of $2.98, representing a 43.4% recovery from the $2.08 trough, as ABA fraud controls and network tightening convert trend mitigation into margin.

EBITDA is also forecasted to nearly double from $0.99 billion in 2025 to $1.87 billion in 2026, reflecting the Marketplace pretax margin swing from approximately -1% to approximately +4% and stabilizing Medicaid costs.

Fourteen of 17 analysts with active recommendations carry a hold or better on CNC, with a mean price target of $43.18 implying 25.5% upside from $34.40, as the Street waits for Q1 2026 results to confirm that the 93.0% Medicaid HBR exit rate is a sustainable base, not a seasonal low.

The spread between the analyst low of $32 and high of $70 reflects the binary nature of the risk adjustment outcome in Marketplace, where a net payable position (meaning Centene pays back into the industry pool for having healthier-than-average members) could pressure the +4% pretax margin assumption that underpins the recovery narrative.

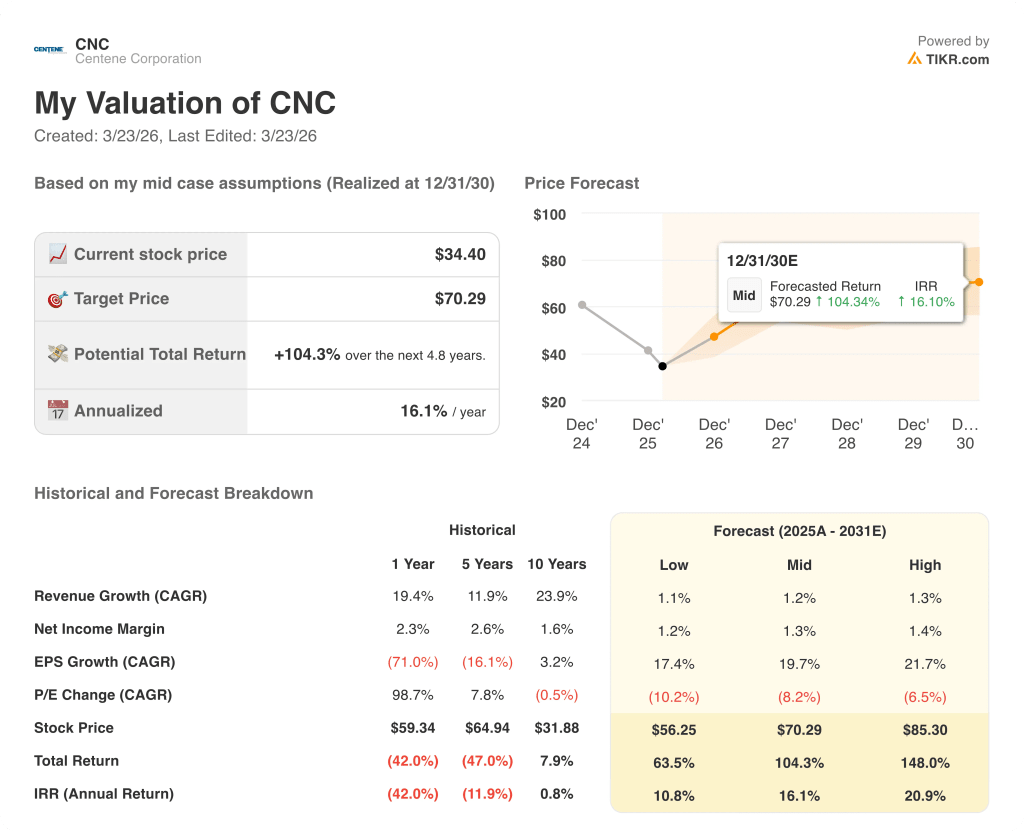

What Does the Valuation Model Say?

The TIKR mid-case model prices CNC at $70.29 by December 2030, implying a 16.1% annualized return, anchored by normalized EPS compounding from $2.98 in 2026 to $9.53 in 2030 as EBIT margins expand from 0.6% to 3.5% on fraud controls, ABA task force scaling, and Marketplace repricing.

At $34.40, the market prices Centene as if the 2025 loss year defines the business, ignoring that normalized EPS already rebounded to $2.08 and is forecast to reach $2.98 in 2026.

The ABA task force’s 75 daily fraud detection algorithms, already delivering sequential HBR improvement in H2 2025, is the operational proof behind the TIKR model’s $70.29 target and its assumption of sustained margin recovery through 2030.

CEO London’s public commitment to outperforming a flat Medicaid HBR, paired with the March 25 redemption of $1 billion in notes, signals management treats $3.00 adjusted EPS as a floor, not a ceiling.

The March 25 note redemption reduces near-term financial flexibility; if Medicaid trend re-accelerates above mid-4s percent in H1 2026, the deleveraging priority leaves no buyback buffer to support the stock.

The single number to watch is Q1 2026 Medicaid HBR: a print at or below 93.0% confirms the trend initiatives are annualizing, validating the TIKR model’s path to $70.29.

Should You Invest in Centene Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CNC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Centene Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CNC stock on TIKR for Free →