Key Stats for COIN Stock

- Past week’s performance: -2.9%

- 52-week range: $139 to $445

- Valuation model target price: $270

- Implied upside: 36.7% over 2.8 years

Value your favorite stocks like COIN with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Coinbase (COIN) stock has been under pressure in recent weeks, and shares were down about 2.9% over the past week through March 20. The move came as crypto sentiment softened again, and investors weighed both company-specific issues and a less supportive backdrop for digital assets. This matters because Coinbase still trades as a leveraged play on crypto prices, volumes, and overall market activity.

Part of the pressure also came from platform disruptions. The company flagged delayed sends and receives on the BSC network on March 19, and then delayed sends and receives on Ethereum, plus latency or degraded performance for some fiat withdrawals on March 23. These incidents did not shut down the platform, but they added friction at a time when investors already wanted more confidence in operating stability.

The stock also continued to digest Coinbase’s February earnings release. The company posted adjusted EBITDA of $566 million, but quarterly results still faced pressure from weaker trading volumes and a broad digital-asset selloff.

In its shareholder letter, Coinbase also guided Q1 subscription and services revenue to $550 million to $630 million, reflecting lower average crypto prices, lower interest rates, and lower staking reward rates than in Q4.

There were some positive headlines too, but they were not enough to fully change the tone. Coinbase was reported to be competing for a stablecoin deal tied to Cloudflare and AI agent payments, which fits the company’s push to expand beyond trading. But for now, the stock still seems more sensitive to crypto prices, network performance, and near-term revenue expectations than to longer-dated product optionality.

See analysts’ growth forecasts and price targets for COIN (It’s free) >>>

Is COIN Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 6.7%

- Operating Margins: 26.2%

- Exit P/E Multiple: 41x

Based on these inputs, the model estimates a target price of $270, implying 36.7% total upside from the current share price and a 11.9% annualized return over the next 2.8 years.

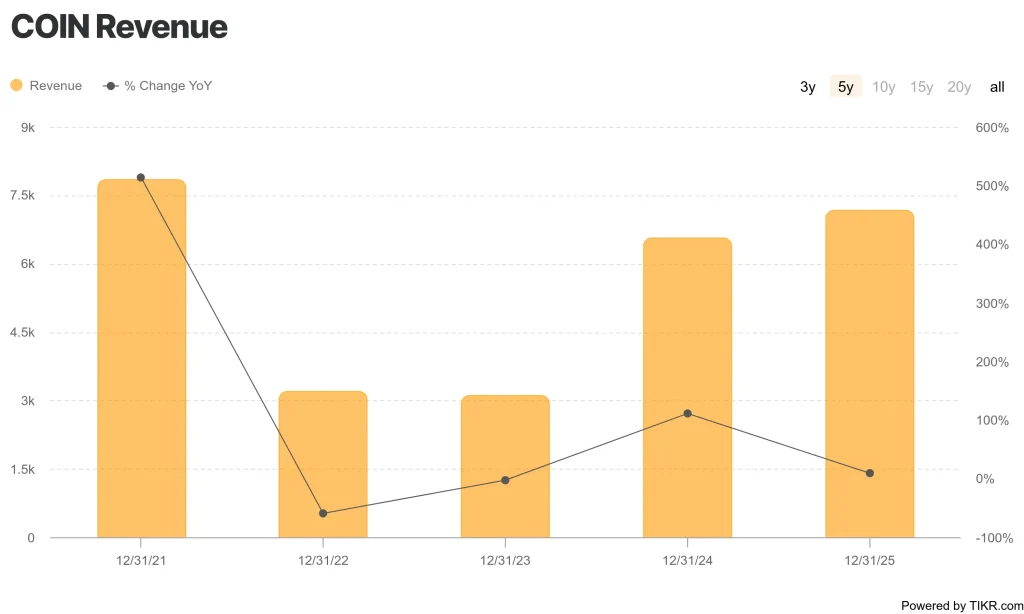

Based on analysts’ consensus estimates, we assume a much steadier Coinbase than the market often prices day to day. Revenue grew 9.4% in 2025 to $6.88 billion, but the model only assumes 6.7% annual revenue growth through 2028. That means the path to the target price does not require another explosive crypto cycle, but it does assume the business can keep growing beyond pure spot trading.

Margins are a major part of the story. Coinbase’s LTM EBIT margin is 21.5%, while the valuation model assumes operating margins improve to 26.2% by 2028. That suggests the model is counting on operating leverage from a larger platform, not just on higher token prices or a speculative rebound in retail volumes.

The multiple assumption is still elevated, but it is not detached from current trading. The model uses a 41.0x P/E multiple, versus an LTM P/E of around 44.4x and a 1-year historical P/E of 44.2x in the valuation image. So the forecast does not require a big multiple rerating, but it does require Coinbase to preserve earnings power in a more volatile environment.

What’s Driving the Stock Going Forward?

Coinbase’s next move will still be driven first by crypto market conditions. The company has high margins and strong balance-sheet flexibility, but transaction revenue remains tied to asset prices and trading activity. When bitcoin and ether weaken, investor expectations for Coinbase usually compress quickly because lower volatility can reduce trading intensity.

That said, the business is much broader than it was a few years ago. Management said Coinbase One subscriptions reached about 1 million, trading volume and market share doubled in 2025, and USDC held on the platform reached an all-time high. Those details matter because they show Coinbase is trying to become a more diversified financial platform rather than just a crypto broker.

The balance sheet is also a real source of flexibility. Coinbase ended 2025 with about $11.6 billion in cash and short-term investments, and it remained in a net cash position of roughly $3.7 billion based on the figures provided. That gives the company room to invest, repurchase stock, and pursue acquisitions even if crypto markets stay choppy.

The clearest near-term catalyst is the next earnings report, expected on April 30. Investors will likely focus on transaction revenue, subscription and services revenue, stablecoin trends, and whether platform reliability issues fade after the March incidents. Until then, the stock may keep trading with crypto prices, macro rate expectations, and every headline tied to regulation, stablecoins, or network performance.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Coinbase Global, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up COIN, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track COIN alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Coinbase Global stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!