Woodside Energy (WDS) is a global energy company focused on the safe, reliable, and responsible production of oil and gas, primarily Liquefied Natural Gas (LNG). The company’s core strategy centers on optimizing its world-class producing assets while developing a robust pipeline of major growth projects designed to meet future global energy demand. This focus on execution ensures Woodside maintains its position as a major, resilient LNG supplier.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)>>>

The third quarter of 2025 demonstrated strong operational performance, highlighted by disciplined asset management and capital execution. This stability allowed Woodside to capitalize on a favorable average realized quarterly price of $60 per barrel of oil equivalent (boe). The successful operation of core assets directly translates into strong cash flow, which is essential for funding the next phase of its massive growth pipeline.

Woodside’s focus is clear: delivering its flagship Scarborough Energy Project on schedule while accelerating new ventures like Trion and Louisiana LNG. The disciplined progression of these projects, combined with strict capital allocation, is crucial for translating today’s investment into substantial future production growth and resilient shareholder returns.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Woodside delivered stable production, reporting 50.8 million barrels of oil equivalent (MMboe) for the third quarter, a one percent increase from the prior quarter. Full-year 2025 production guidance has been revised to 192-197 MMboe, demonstrating confidence in operational stability. The average realized quarterly price of $60 per boe provided a strong financial underpinning for the period.

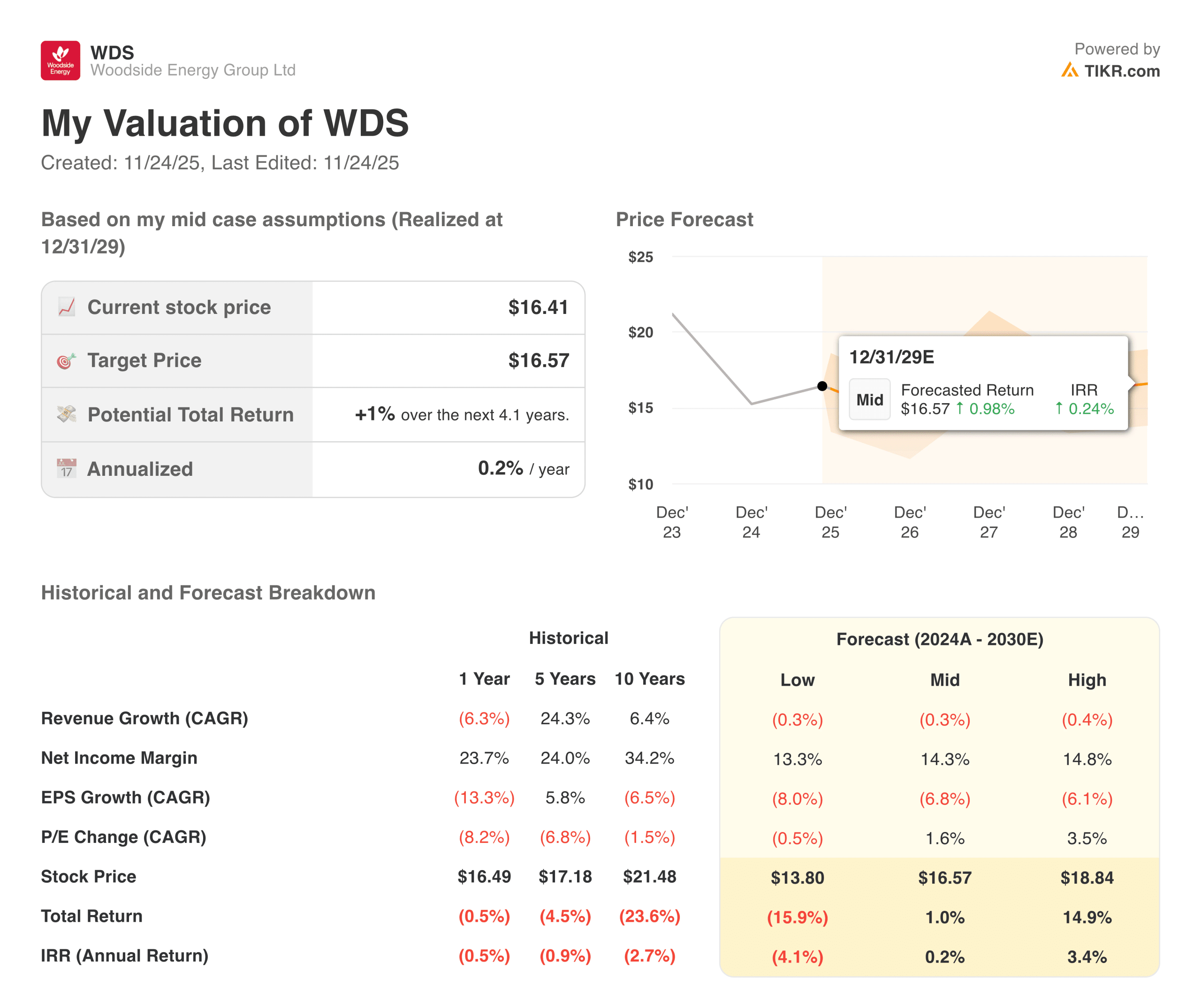

| Metric | Value |

|---|---|

| Revenue Growth (1 yr) | (6.3%) |

| Net Income Margin (1 yr) | 23.7% |

| EPS Growth (1 yr) | (13.3%) |

| P/E Change (1 yr) | (8.2%) |

| Historical 5-year EPS CAGR | 5.8% |

| Historical 10-year EPS CAGR | 6.5% |

| 2029 Mid Case Target Price | $16.57 |

| Total Return (Mid Case) | 1.0% through 2029 |

| Annualized IRR (Mid Case) | 0.2% |

Half-year net profit after tax (NPAT) reached $1.069 billion U.S. dollars, reflecting effective cost management against volatile commodity prices. Operational discipline focused keenly on efficiency, with Woodside successfully reducing sustaining capital expenditure by 13% year over year. This control is vital for maximizing cash generation from existing assets to fund the capital-intensive growth portfolio.

The high quality of assets was demonstrated by Pluto LNG achieving 100% reliability for the quarter, minimizing production deferrals. The strong operational performance supports a commitment to a balanced capital allocation framework that prioritizes both growth investment and consistent shareholder returns. This strategy aims to maximize long-term shareholder value throughout the energy transition.

Look up Woodside Energy’s full financial results & estimates (It’s free)>>>

Broader Market Context

Energy has been one of the more volatile sectors in the past year. LNG prices moved sharply due to changes in European storage levels, Asian demand, and supply disruptions. The global majors also faced rising costs, slower project approvals, and tighter capital markets. Woodside’s performance sits roughly in the middle of its peer group.

The company has not suffered the deep cuts seen in some integrated producers, but it has not benefited from the sharp rebounds seen elsewhere. The market has taken a wait-and-see stance, especially around Scarborough and long-term LNG demand.

1. Operational Discipline and Cash Generation

Woodside continues to focus on operational stability across its LNG portfolio. Production levels remain consistent with prior guidance, and the company has taken steps to tighten cost controls after a year of inflation pressure. The focus on reliability has helped keep margins steady, despite softer commodity prices. Management emphasized efficiency improvements across the North West Shelf and Pluto, which should support cash generation as conditions normalize.

The company’s operating cash flow remains one of its strongest features. Even with lower pricing, the core LNG assets continue to produce steady cash that supports the balance sheet. Free cash flow fluctuates with market conditions, but the underlying generation capacity remains intact. Over time, better cost discipline and improved project sequencing may help stabilize results. Investors will be watching whether Woodside can keep capital spending moderate without sacrificing growth.

2. Project Pipeline, Scarborough, and Long-Term Outlook

The Scarborough project remains central to Woodside’s future. It represents a major share of the company’s long-term volume, and investors want greater clarity on cost updates, regulatory milestones, and timing. While progress continues, the market has priced in some uncertainty amid changing cost estimates for global LNG developments.

Longer term, Woodside sees demand strength from Asia as a key tailwind. LNG remains a transitional fuel for many economies that are reducing coal dependence. Management expects robust demand through the next decade, with Woodside positioned as a reliable supplier. The company’s ability to deliver Scarborough, optimize existing assets, and maintain capital discipline will shape how much of that demand translates into value creation. For now, the trajectory remains constructive but not without execution risk.

Value stocks like Woodside Energy in less than 60 seconds with TIKR (It’s free) >>>

3. Valuation, Expectations, and What the Model Suggests

The TIKR valuation model shows low single-digit upside in the mid case through 2029. Revenue growth is expected to remain flat in the base scenario, with margins stable and capital spending normalized. The low case reflects downside risks from continued price softness or delays in major projects, while the high case assumes stronger LNG pricing and better operational leverage.

Investors should interpret these scenarios as reflecting mixed sentiment. Woodside has a stable asset base and dependable cash flows, but earnings will continue to move with global energy markets. The company’s long-term value will depend on consistent execution, disciplined investment, and the ability to keep costs firm across its portfolio.

The TIKR Takeaway

The TIKR valuation model shows low single-digit upside in the mid case through 2029, and revenue growth is expected to remain flat in the base scenario, with margins stable and capital spending normalized. However, 2025 has only seen very minimal growth for shareholders. This reflects downside risks from continued price softness and delays in major projects, while the high-case scenario assumes stronger LNG pricing and better operational leverage.

Investors should interpret these scenarios as reflecting mixed sentiment. Woodside has a stable asset base and dependable cash flows, but earnings will continue to move with global energy markets. The company’s long-term value will depend on consistent execution, disciplined investment, and the ability to keep costs firm across its portfolio.

Should You Buy, Sell, or Hold Woodside Energy Stock in 2025?

Woodside sits in the middle ground where investors want clearer signals before forming stronger views. The core LNG assets continue to generate steady cash, and the balance sheet remains solid, but earnings still move with global pricing and project timing.

Scarborough is the primary variable, and consistent updates on costs and milestones will shape confidence. Investors focused on long-term stability may value the resilience, while others may wait for clearer confirmation that growth and margins are trending in the right direction.

How Much Upside Does Woodside Energy Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!