Public Service Enterprise Group (NYSE: PEG) has been under pressure over the past year. Rising interest rates and softer sentiment across utilities pushed the stock near $81/share, even though PEG continues to report steady margins and consistent earnings. Its regulated business remains a stable anchor in a volatile market.

Recently, PEG highlighted strong progress across several operational initiatives. Management pointed to ongoing rate base expansion from transmission and distribution upgrades, as well as continued momentum in its clean energy transition plan. These developments show that PEG is still moving forward on long-term priorities despite broader sector challenges.

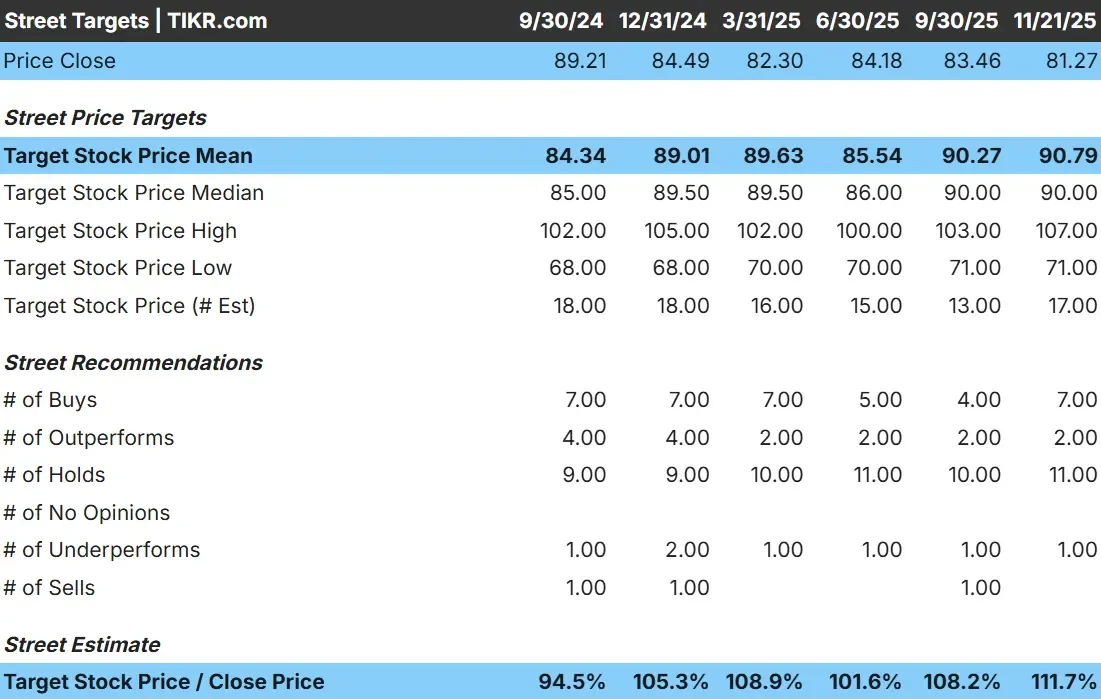

This article explores where Wall Street analysts expect PEG to trade by 2027. We combined consensus price targets with PEG’s valuation model to outline the stock’s expected trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

PEG trades around $81/share today. The average analyst target sits near $91 to $92/share, which implies roughly 12% upside from current levels. This places PEG in the modest-upside category, suggesting a steady but not aggressive outlook.

Key targets:

- High estimate: $107/share

- Low estimate: $71/share

- Median estimate: $90/share

- Ratings: 7 Buys, 2 Outperforms, 11 Holds, 1 Underperform

The range is fairly tight, and most analysts remain neutral to slightly positive. For investors, this generally means PEG is expected to track its earnings performance. Any upside is likely to be driven by steady fundamentals rather than a major shift in sentiment.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

PEG: Growth Outlook and Valuation

PEG’s fundamentals look stable, supported by predictable regulated revenue and steady margin performance:

- Revenue is projected to grow 6.8%

- Operating margins are expected to remain near 29.8

- Shares trade at roughly 19x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19x forward P E suggests about $98/share by 12/31/27

- That implies roughly 20.7% upside, or about 9.3% annualized returns

These numbers suggest PEG can continue compounding gradually, supported by strong earnings visibility and a stable regulated footprint. For investors, PEG behaves more like a steady compounding utility than a high-growth story, with most of the return coming from consistency rather than rapid expansion.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

PEG benefits from predictable regulated returns and a long pipeline of utility infrastructure projects. Upgrades across its transmission and distribution networks are helping improve efficiency, and the company continues to invest in clean energy initiatives that support long-term earnings stability.

For investors, these strengths suggest PEG has a reliable foundation for steady compounding. It is not a high-growth story, but its operational consistency gives analysts confidence that the company can maintain stable performance even in a tougher rate environment.

Bear Case: Slow Growth and Rate Sensitivity

Despite these positives, PEG still faces challenges typical of regulated utilities. Growth remains slow, the business is highly sensitive to interest rates, and comparable utilities with faster renewable expansion may attract more investor attention.

For investors, the main risk is that PEG’s valuation could remain capped if interest rates stay elevated. The company offers resilience, but the upside is naturally limited by its steady-growth profile and the regulatory environment it operates in.

Outlook for 2027: What Could PEG Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19x forward P E suggests PEG could reach about $98/share by 2027. From today’s price near $81/share, that represents roughly 21% upside, or about 9.3% annualized returns.

This scenario reflects stable margin performance and consistent rate base expansion. For PEG to outperform these expectations, earnings would need to accelerate or interest rates would need to ease, allowing for a stronger valuation.

For investors, PEG looks like a reliable long-term utility with predictable compounding. Most of the return potential comes from steady fundamentals rather than rapid growth, making it a suitable choice for those seeking stability over volatility.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>