Key Stats for Intel Stock

- Current Price: $110.39

- Target Price (Mid): ~$298

- Street Target (TIKR): ~$101

- Potential Total Return: ~170% over the next 4.5 years

- Annualized IRR: ~25% / year

- Max Drawdown (last year): 24.17% on March 30, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Intel Corporation (INTC) just did something a stock up almost 290% on the year is not supposed to do: it fell roughly 10% in a single session. Shares closed July 7 at $110.39, down $11.81, and the strangest part is that almost none of it was about Intel. The selling came from a broad semiconductor reset, sparked by Samsung profit-taking and a Bank of America note flagging bubble risk in the AI chip trade. Just five days earlier, on July 2, HSBC had doubled its price target on Intel to a Street-high $200.

That is the tension in one sentence. The most bullish call on Wall Street and the sharpest daily drop of the summer arrived in the same week, on the same stock. Bulls look at the pullback and see a gift on a name whose turnaround is finally producing receipts. Bears look at a chip that ran roughly five times faster than the Philadelphia Semiconductor Index in the first half and see a crowded trade unwinding. The question the market cannot yet answer is whether a business still losing billions in its foundry arm has earned the right to trade like this at all.

A selloff that skipped the fundamentals

Nothing broke at Intel on July 7. The catalyst was Samsung’s preliminary Q2 report, a record profit beat that still triggered profit-taking across the chip complex, with Applied Materials and AMD falling alongside Intel. Layered on top was the July 1 BofA warning that AI semiconductor valuations had run ahead of near-term demand. Morgan Stanley added to it, moving to underweight semiconductors in favor of hyperscale cloud names, and describing the two-day drop in high-beta chip stocks as a rotation rather than a call on AI itself.

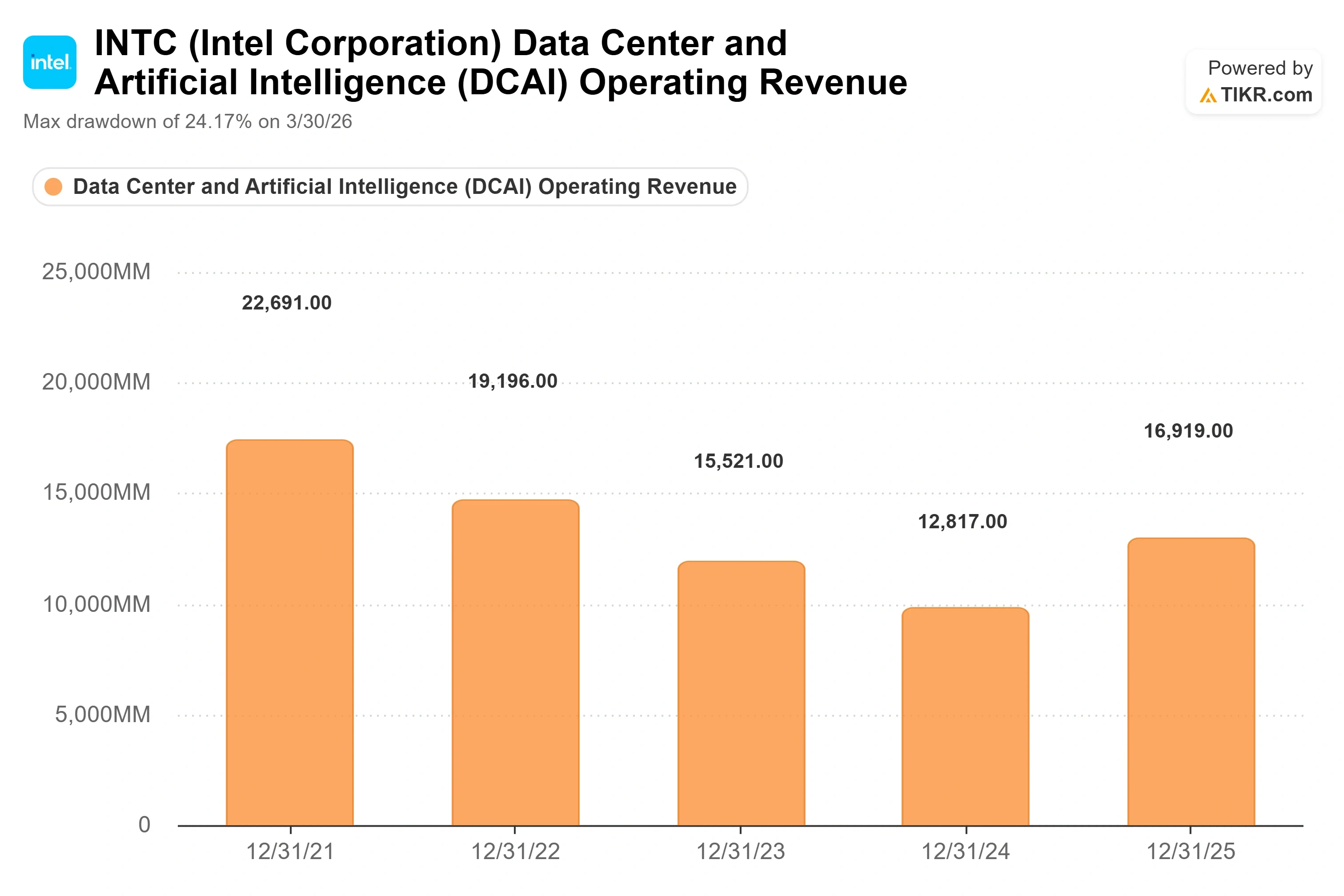

For Intel specifically, two nagging worries resurfaced under the sector pressure. The first is the 18A foundry timeline, Intel’s most advanced manufacturing process, which some now expect will not deliver profitable yields until late 2026 or 2027. The second is competitive: in Q1 2026, AMD’s data center revenue of $5.8 billion edged past Intel’s $5.1 billion for the first time. Intel still runs about two-thirds of the server CPU market, but momentum in the segment has clearly shifted.

See historical and forward estimates for Intel stock (It’s free!) >>>

Why the bull case did not actually change

Here is what the selloff did not touch: management’s own account of where the margins are headed. Speaking at the Bank of America 2026 Global Technology Conference on June 2, CFO David Zinsner directly addressed the yield fear now being used to sell the stock. He described the plan to reach the yields that generate strong margins as an end-of-2027 target, then added the line investors have been chewing on since.

“Based on the progress we’ve made to date now, we are likely going to pull in those milestones by at least a quarter, potentially even a little more,” Zinsner said.

That matters because Intel’s margins hinge almost entirely on factory yields. When yields improve, more revenue drops through a cost base that is largely fixed, so pulling the yield milestones forward pulls forward the point at which the fabs start working for the company instead of against it. Zinsner was careful about scope: he kept Intel Foundry’s own breakeven target at exiting 2027, and said the only thing that would push it out is being “more wildly successful” and spending more on capacity. That is the rare kind of risk investors do not mind.

He was blunt about how the turnaround got here, too, framing the whole recovery as an execution and culture fix rather than a market gift. CEO Lip-Bu Tan collapsed twelve management layers into six, cut the vice president count from over 400 to 200, and reduced headcount from more than 100,000 to under 80,000. On product, Zinsner conceded Intel is weaker in multi-threading, and noted the fix arrives later in the roadmap: the Diamond Rapids server chip lacks it, and it returns in the following product, Core Rapids. That kind of candor is the point. It is a company that now says what is broken.

What the peers say about the price

Intel does not screen cheap against its own sector on the surface. On TIKR’s Competitors page, Intel trades at around 28x NTM EV/EBITDA (next twelve months enterprise value to earnings before interest, taxes, depreciation, and amortization) and about 104x NTM P/E, both well above the peer group. NVIDIA sits near 16x NTM EV/EBITDA, Broadcom near 19x, and AMD near 50x. On earnings, Intel’s multiple looks punishing next to NVIDIA at roughly 20x and Broadcom near 24x.

The premium is not justified on trailing math, and that is the honest read. It is only justified if you believe the forward earnings recovery baked into consensus. Intel’s earnings are estimated to swing from a Q1 2026 adjusted EPS of $0.29 to a full-year path that turns sharply positive, and that inflection, not today’s ratio, is what a buyer is underwriting. This is a bet on the second derivative, not the current one.

See how Intel performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $110.39

- Target Price (Mid): ~$298

- Potential Total Return: ~170%

- Annualized IRR: ~25% / year

See analysts’ growth forecasts and price targets for Intel stock (It’s free!) >>>

Using TIKR’s mid-case, the model values Intel at around $298 by year-end 2030, implying around 170% total return from the current price, or roughly 25% annualized over about 4.5 years. We use the mid-case here because it best matches management’s own stated cadence: it assumes revenue growth of around 13% CAGR and a net income margin near 15%.

The two revenue drivers are server CPU demand, where the shift from AI training toward inference and agentic workloads is pulling CPUs back into the buildout, and Intel Foundry, where external design commitments are expected to begin in the second half of 2026. The margin driver is factory yield improvement on 18A, the single lever Zinsner tied every margin milestone to. The primary risk is the same lever inverted: if 18A yields slip, the fixed-cost fab base works against Intel, and the earnings recovery moves right.

The upside is that on-time 18A execution proves the roadmap is real, foundry customers sign volume, and Intel re-rates as the default American foundry with margins to match. The downside is that yields disappoint, and a stock still trading richly gives back the premium it built on promises.

One number to keep honest: TIKR’s Street mean target sits at around $101, slightly below the current price, because the sell-side consensus has not caught up to the HSBC and Cantor upgrades. The model’s ~$298 is a conviction case, not the crowd’s.

Conclusion

The one thing to watch is non-GAAP gross margin when Intel reports Q2 2026 results on July 23. Management guided to around 39% for the quarter, down from Q1’s 41%. Hold at or above that mark, and Zinsner’s “pull in by at least a quarter” comment starts to look conservative, and the yield-and-pricing story is working. Slip meaningfully below it, toward 37% or lower, and the margin-recovery timeline shifts right, which is the one thing a stock priced this richly cannot absorb. The July drop handed patient buyers a cheaper entry into that print. Whether it was a gift or a warning is a question only the margin line, not the target price, will answer.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Intel?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Intel, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intel alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!