Key Stats for General Motors Stock

- Past-Week Performance: -3.8%

- 52-Week Range: $41.6 to $87.6

- Current Price: $72.4

What Happened?

General Motors (GM), the Detroit automaker behind Chevrolet, Buick, Cadillac, and GMC, is forcing a re-rating after guiding 2026 EBIT adjusted to $13 billion to $15 billion while targeting a return to 8% to 10% North America margins ahead of most investor timelines, with shares currently trading at $72.39.

On January 27, General Motors reported full year 2025 EBIT adjusted of $12.7 billion and adjusted automotive free cash flow of $10.6 billion, both at the high end of guidance, while absorbing $3.1 billion in gross tariff costs and booking $7.6 billion in EV-related charges to reset its manufacturing footprint.

GM’s structural free cash flow improvement, from roughly $3 billion annually five years ago to a consistent $10 billion run rate, reflects the discipline of running 48 days of dealer inventory versus the industry’s historical 100-plus days, a posture that strips out the self-induced cyclicality that once defined the stock’s discount.

CFO Paul Jacobson stated at the Citi Global Industrial Tech and Mobility Conference on February 17 that “this feels like the most stable year of the last several,” then tied that confidence to $3 billion to $4 billion in manageable tariff exposure and a tariff playbook the team had prepared before inauguration day.

With a Board-approved $6 billion repurchase authorization, a 20% dividend increase to $0.18 per share quarterly, $5 billion committed to onshoring U.S. production toward a 2-million-unit annual capacity target by 2027, and LMR battery chemistry projected to cut EV pack costs by thousands of dollars per vehicle when it launches in 2028, GM’s investment case rests on a durability of cash generation that the current valuation has not yet fully priced in.

Wall Street’s Take on GM Stock

The $13 billion to $15 billion EBIT adjusted guidance for 2026, which arrives roughly 12 to 18 months ahead of investor timelines, directly validates the free cash flow durability that underpins GM’s accelerating capital return program, including the new $6 billion buyback authorization and the 20% dividend increase announced January 26.

Consensus estimates show normalized EPS rising from $10.60 in 2025 to $12.45 in 2026, a 17.4% step-up driven by the $1 billion warranty cost improvement, the $500 million to $750 million in compliance credit savings from CAFE deregulation, and the $1 billion to $1.5 billion EV capacity rightsizing benefit that GM quantified on the January 27 earnings call.

Twelve analysts carry buy ratings, seven hold outperform ratings, and six hold neutral ratings, against just one underperform and one sell, with the mean price target of $95.04 implying 31.3% upside from the current $72.39 close, a spread that reflects Wall Street’s growing conviction in the North America margin recovery thesis.

The $57 low target and $122 high target define a range where the bear case assumes tariff escalation and EV demand deterioration erode the $9 billion to $11 billion free cash flow guidance, while the bull case prices in the full execution of the $5 billion U.S. onshoring program and the 2-million-unit domestic production target landing in 2027.

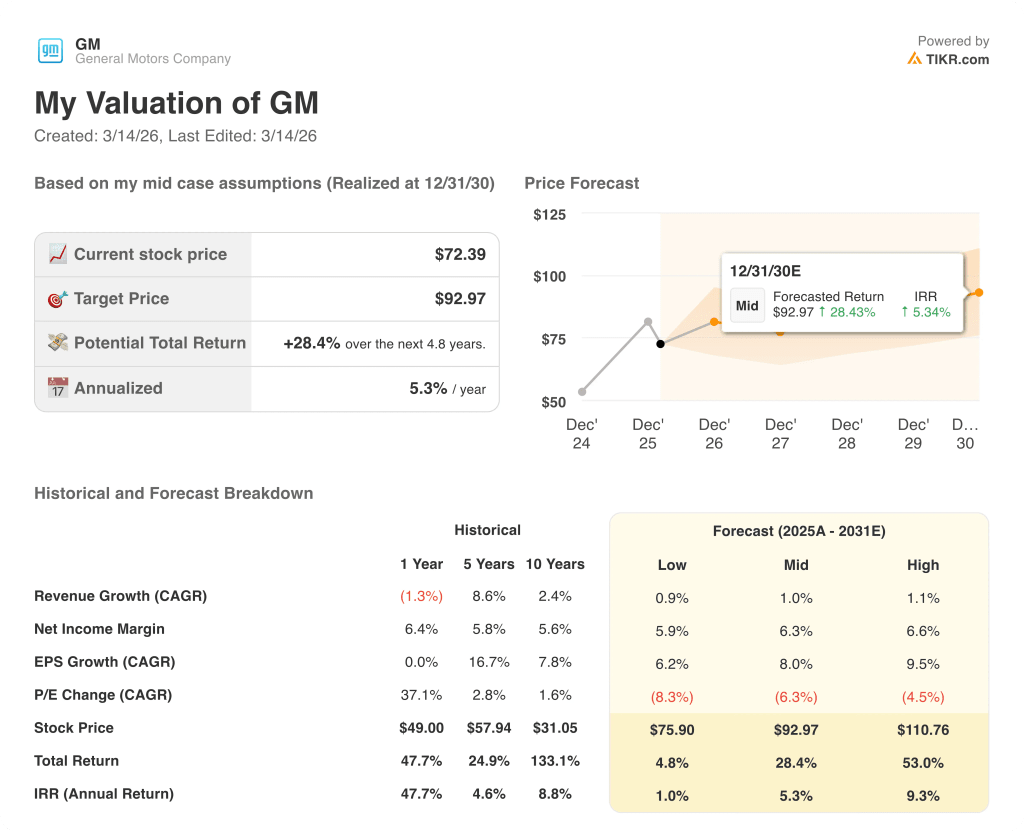

What Does the Valuation Model Say?

TIKR’s model targets $92.97 per share at its mid-case, representing a 28.4% total return over 4.8 years at a 5.3% annualized IRR, pricing in 1.0% revenue CAGR and a 6.3% net income margin, inputs that are conservative against GM’s stated $185 billion revenue base and the $10 billion free cash flow floor the company has now demonstrated for multiple consecutive years.

The market is pricing GM at roughly 5.8x 2026 consensus EPS of $12.45, a discount that ignores $10.6 billion of adjusted free cash flow generated in 2025 while the buyback alone has retired 35% of the float since late 2023.

GM sold over 700,000 vehicles priced under $30,000 profitably in 2025, confirming that the ICE portfolio generates margin at every price point, the operational foundation that makes the EBIT guidance credible rather than aspirational.

CFO Paul Jacobson’s statement at the February 17 Citi conference that the tariff environment “is getting more stable” and that net tariffs in 2026 will finish lower than 2025 signals that management sees the cost structure as peaking, not accelerating.

A sustained deterioration in North America pricing, where GM currently runs incentives roughly 200 basis points below the industry average, would directly compress the 8% to 10% margin target and invalidate the EPS growth trajectory the TIKR model depends on.

The next confirmation point is Q1 2026 earnings, where the $750 million to $1 billion tariff cost guidance and the early trajectory of the warranty improvement program will either validate or challenge the $13 billion to $15 billion full year EBIT range.

Should You Invest in General Motors Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track General Motors Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GM stock on TIKR for Free →