Key Takeaways for Trane Technologies Stock as of June 2026

- Analysts rate Trane Technologies stock 11 buys, 2 outperforms, 10 holds, 1 underperform, and 1 sell, with a mean target of $521, implying around 9% upside from the current price of $478.

- TIKR’s mid-case model values Trane Technologies at around $895 by December 2030, implying around 87% total return, or roughly 15% annualized.

- Americas Commercial HVAC applied bookings surged 160% in Q1 2026, the third consecutive quarter above

Trane Technologies Stock Reaches Record Backlog as Applied Orders Surge for Third Straight Quarter

Trane Technologies (TT) closed Q1 2026 with a record backlog of $10.7 billion, up around 70% year-over-year and more than 30% from year-end 2025, as the strongest order cycle in company history continued to build.

Organic revenue grew 3%, EBIT reached $790 million, up 5% year-over-year, and adjusted EPS climbed 7%, but the structural signal came from the order book: enterprise organic bookings surged 24% and a book-to-bill of approximately 150% confirmed demand is running well ahead of current deliveries.

That momentum concentrated in commercial HVAC, where applied solutions, large engineered systems including centrifugal chillers for data centers, hospitals, universities, and government facilities, posted bookings growth of 160% in Q1. The result marked the third consecutive quarter above 100%, with Americas Commercial HVAC bookings overall rising approximately 40%.

The demand extended across nine of the 14 verticals the company tracks, including healthcare, higher education, high-tech industrial, and government, confirming data center strength is amplifying core market performance rather than masking weakness elsewhere.

With book-to-bill at approximately 150%, CEO Dave Regnery addressed the backlog’s forward implications directly on the Q1 earnings call: “Our Q1 book-to-bill was approximately 150% and our backlog is up nearly 70% year-over-year, strengthening our visibility into 2026 and beyond.”

That visibility led management to raise full-year organic revenue guidance to approximately 7% and adjusted EPS guidance to $14.75 to $14.95, representing 13% to 15% growth for the year.

The Stellar Energy acquisition, completed ahead of Q1, brought approximately $1 billion of backlog, with management targeting the modular chiller plant business at $1 billion in annual revenue within two to three years at mid-teens EBITDA margins, up from approximately $350 million in 2025. A concurrent acquisition of LiquidStack extended Trane’s position in liquid cooling for high-density compute environments, supporting the company’s reference design work alongside hyperscalers including NVIDIA.

The second-half guide calls for approximately 10% organic growth in Q2, stepping to low-teens in Q3 and Q4 as backlog converts to customer deliveries, with operating leverage expected to expand to the mid-to-high 20s from the high teens recorded in Q1.

Trane Technologies Stock Has 13 Buys and Outperforms as the Mean Target Sits 9% Above the Current Price

As of June 2026, 23 analysts cover Trane Technologies, with 11 buys, 2 outperforms, 10 holds, 1 underperform, and 1 sell.

The mean price target stands at $521, implying around 9% upside from the current price of $478, against a 52-week range of $348 to $506. The buy count has risen from 7 at end-2025 to 11 as of June 2026, consistent with three consecutive quarters of applied bookings growth above 100% and a backlog up around 70% year-over-year.

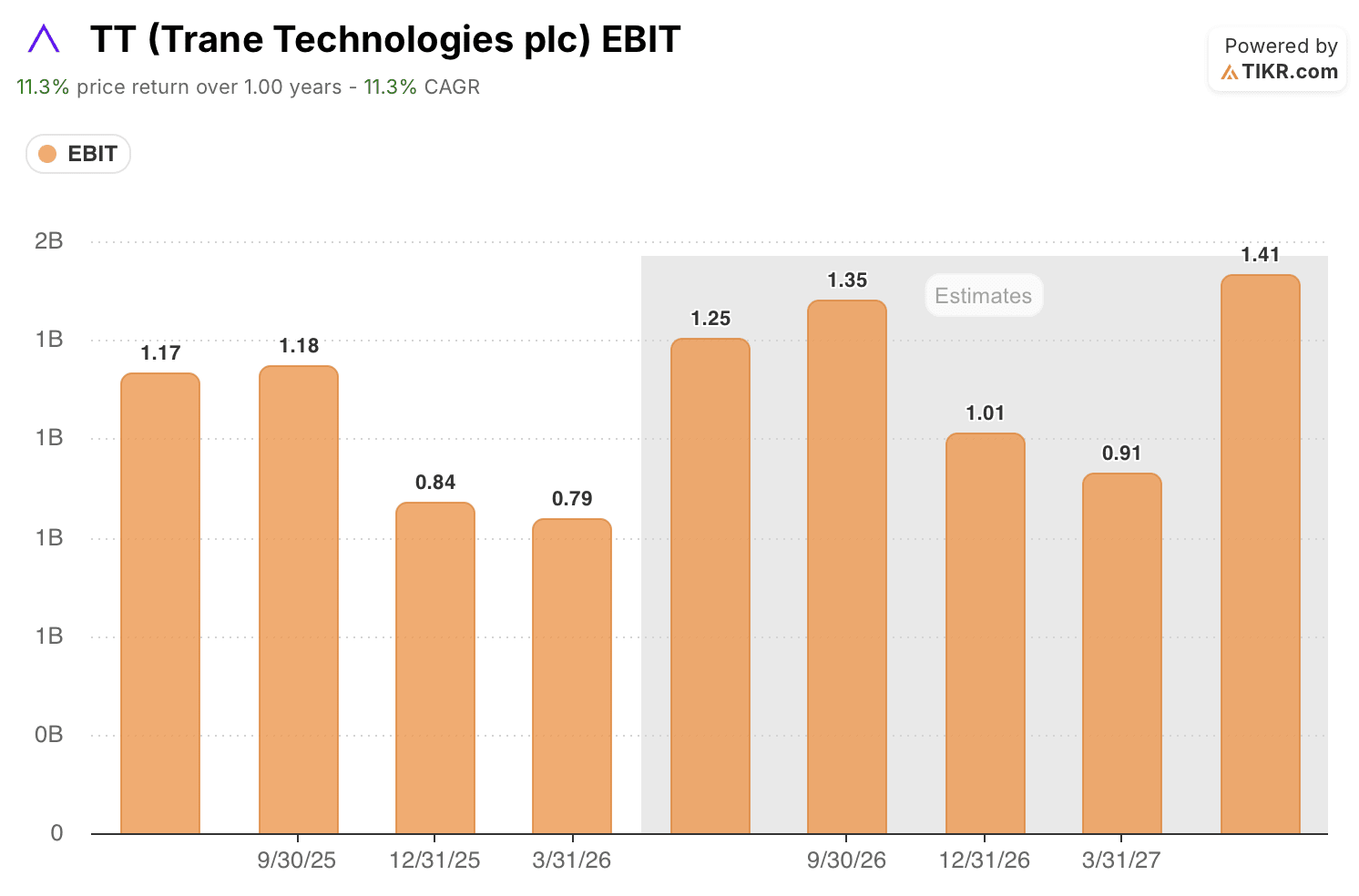

Wall Street Expects Trane Technologies’ EBIT to Accelerate Past 20% Growth by Q4 2026

Trane Technologies posted EBIT of $790 million in Q1 2026, a 5% gain year-over-year, as organic revenue grew 3% and operating leverage ran in the high teens. The result reflected the seasonally softer first quarter, with the commercial HVAC backlog still in its early conversion phase.

Consensus estimates project EBIT at around $1.25 billion for Q2 2026, a gain of around 7% year-over-year, as the Americas applied backlog begins converting to revenue at scale. By Q3, consensus rises to around $1.35 billion, a gain of around 14%, with EBIT margins reaching approximately 21% as applied solutions deliveries accelerate.

Q4 2026 consensus sits at around $1.01 billion, up around 21% year-over-year, as the full weight of the backlog conversion runs through the income statement. The growth rate extends into 2027, with Q1 and Q2 estimates at $910 million and $1.41 billion respectively, both representing double-digit gains over the same periods in 2026.

Trane Technologies stock trades at a discount to what the EBIT trajectory implies. The thesis confirms if Q3 2026 EBIT reaches the consensus $1.35 billion: a delivery shortfall would break the step-change narrative and challenge the undervaluation case.

Trane Technologies Leads JCI and Carrier on EBIT Through 2027

Trane Technologies posted $790 million in EBIT in Q1 2026, against Carrier’s (CARR) $560 million and Johnson Controls’ (JCI) $890 million. By Q3 2026, consensus has Trane at $1.35 billion, pulling ahead of both peers, with Johnson Controls at $1.19 billion and Carrier at $1.07 billion.

The gap widens into 2027. Trane’s Q2 2027 EBIT estimate of $1.41 billion sits above both Johnson Controls and Carrier, each estimated at $1.18 billion for the same period.

TIKR’s $895 Target on Trane Technologies Stock Holds If Backlog Conversion Delivers the Guided Margin Expansion

TIKR’s mid-case model values Trane Technologies at around $895 by December 2030, implying around 87% total return from the current price of $478, or roughly 15% annualized over 4.5 years.

That return profile implies a premium over the conventional expectation for large-cap diversified industrials, grounded in the earnings acceleration the $10.7 billion backlog is set to deliver.

The $895 target is reachable if the second-half backlog conversion delivers the guided earnings acceleration. EBIT growth above 20% in Q3 and Q4 2026, services compounding at low-teens annually, and Stellar Energy scaling toward $1 billion in revenue at mid-teens EBITDA all support the trajectory TIKR’s mid-case assumes.

The variable is timing: a delay in applied deliveries would push the inflection into 2027, but the 4.5-year model horizon absorbs that risk without breaking the case for Trane Technologies stock at current prices.

Should You Invest in Trane Technologies plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Trane Technologies plc stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Trane Technologies plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TT stock on TIKR for Free →