Key Stats for Tesla Stock

- 52-Week Range: $288.77 – $498.83

- Current Price: $379.71

- Street Mean Target: ~$421

- TIKR Model Target: ~$1,643

- Annualized IRR: ~38%

- Q1 2026 Revenue: $22.4B (+16% YoY)

- Q1 2026 Gross Margin: 21.1%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Revenue Dipped in 2025, but the Margin Recovery Changes the Conversation

Tesla (TSLA) designs and manufactures electric vehicles, energy storage systems, and solar products, while also developing autonomous driving software and humanoid robotics.

The automotive segment remains by far the largest source of revenue, but the company has spent the past two years deliberately arguing that the car business is a foundation for something bigger, not the destination itself.

The Q1 2026 results gave bulls something concrete to work with. Revenue came in at $22.4 billion, up 16% year-over-year, as vehicle deliveries grew 6% to 358,023 units and services revenue jumped 42%.

More importantly, gross margin expanded to 21.1%, up nearly five percentage points from 16.3% a year earlier, driven by lower material costs, higher average selling prices, and growing FSD subscription revenue.

Tesla launched unsupervised Robotaxi rides in Dallas and Houston in April, adding the first real commercial data points to what has been a long-promised autonomous driving business.

The revenue chart tells a more complicated story over the longer arc. After compounding from $53.8 billion in 2021 to $97.7 billion in 2024, total revenue actually declined to $94.8 billion in 2025 as aggressive price cuts took their toll on the automotive segment. Street estimates now project recovery to around $103 billion in 2026, scaling toward roughly $119 billion in 2027 and $226 billion by 2030.

That forward trajectory requires Tesla to successfully ramp Robotaxi, Optimus, Cybercab, and energy storage simultaneously, all within a competitive landscape that did not exist when the company first outlined these ambitions.

The Q1 gross margin recovery is real, but TSLA’s operating cost structure is absorbing every dollar of it. Pull up Tesla’s full income statement on TIKR to see exactly where the leverage is — and where it isn’t. Access the data on TIKR for free →

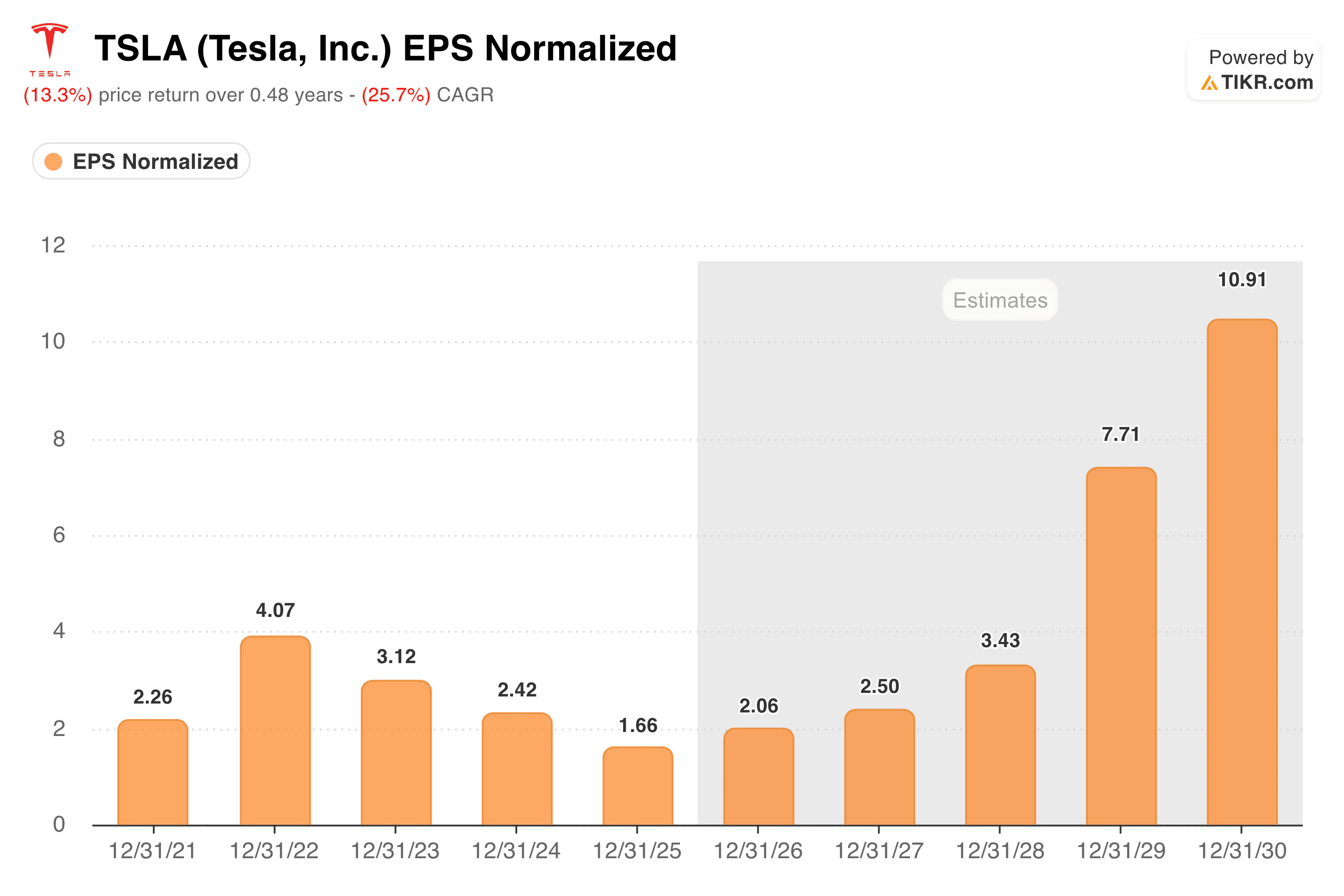

EPS Fell 59% From Its Peak. The Forward Curve Assumes a Dramatic Reversal

The earnings chart captures the damage from the years of the pricing war and frames the stakes of the current recovery attempt.

Normalized EPS peaked at $4.07 in 2022, then compressed steadily to $1.66 in 2025 as Tesla cut vehicle prices aggressively to defend market share against rising competition from Chinese EV makers and domestic rivals.

The consensus now expects around $2.06 in 2026, rising to $2.50 in 2027, and accelerating sharply to nearly $11 by 2030. That endpoint requires a complete transformation of the earnings mix: the automotive business contributes steady volume, while robotaxi, Optimus, and energy storage provide the high-margin revenue streams that justify a meaningfully higher earnings base.

Active FSD subscriptions grew 51% year-over-year to 1.28 million in Q1, which is encouraging, but is a long way from the scale the forward EPS curve demands.

The energy segment grew from $2.8 billion in 2021 to $12.8 billion in 2025, more than quadrupling over four years, and is frequently cited by analysts as the most underappreciated part of the business today.

See historical and forward estimates for Tesla stock (It’s free!) >>>

TIKR’s Model Targets Around $1,640, but the IRR Depends on a 21% Revenue CAGR Through 2035

The TIKR valuation model targets approximately $1,643 per share for Tesla, implying a total return of around 333% over 4.5 years and an annualized IRR of roughly 38%.

The mid-case assumptions are aggressive by the standards of any established business: around 21% annual revenue growth through 2035 and net income margins expanding to roughly 23%. For context, Tesla generated an 18% net income margin in its best recent year.

Achieving and sustaining margins at that level while scaling to $225 billion in revenue would require the robotaxi and Optimus businesses to become genuinely profitable at volume, not just technically operational.

The Street’s mean target of around $421 is far more modest, implying that most analysts are pricing Tesla closer to its automotive earnings power with a modest premium for optionality.

The gap between the TIKR model’s $1,643 and the Street’s $421 reflects the market’s current disagreement about which version of Tesla will materialize over the next decade.

Should You Invest in Tesla, Inc.?

Tesla is a company with a legitimate foundation in electric vehicles and energy storage, a margin recovery underway, and a set of platform bets in autonomy and robotics that could prove transformative or could remain perpetually just over the horizon.

The NTM P/E of roughly 176x prices in a great deal of optimism about which scenario plays out. TIKR gives you the tools to track the metrics, margins, and delivery numbers that will determine whether that optimism is warranted.

See how Tesla performs against its peers in TIKR (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!