Key Stats for Dell Technologies Inc. Stock

- This Week Performance: -1.6%

- 52-Week Range: $66.3 to $168.1

- Current Price: $149.2

What Happened?

Dell (DELL) closed fiscal year 2026 with $64.1B in AI server orders — proof that the company’s infrastructure division, which builds and sells the specialized rack servers that power large-scale AI data centers, has transformed from a PC maker’s sideline into the defining growth engine of one of the largest hardware businesses on earth, with shares up 24% year-to-date to $149.21.

Q4 FY2026 revenue hit a record $33.4B, up 39% and beating the $31.73B analyst consensus, while the company raised its FY2027 revenue guidance to $138B–$142B against a prior Street estimate of $125.54B — a gap that sent shares surging 17.5% on February 27, their biggest single-day gain in nearly two years.

AI-optimized server revenue more than doubled to $24.68B for the full year and reached $9B in Q4 alone, up 4.4x year over year, while rival Hewlett Packard Enterprise reported an AI backlog of just over $5B compared to Dell’s record $43B entering FY2027.

CFO David Kennedy stated on the Q4 FY2026 earnings call that “we went from a net new $34 billion of demand sequentially in the quarter, but yet our dollar pipeline dollar value has never been higher now than it has been in history,” underscoring that record order conversion has not drained forward demand.

A $43B AI backlog, a guide for $50B in AI server revenue in FY2027, a 20% dividend increase to $2.52 per share annually, and an additional $10B share repurchase authorization together frame a capital return story that grows harder to dismiss as the enterprise AI adoption cycle — now at 4,000-plus customers and accelerating — continues to broaden.

Wall Street’s Take on DELL Stock

The $43B AI backlog entering FY2027 effectively pre-loads the revenue line, converting Dell’s infrastructure division (ISG, which houses AI servers, traditional servers, and storage) into a visibility-rich business rather than a cyclical hardware bet — and that shift is the direct cause of the FY2027 revenue guidance of $138B–$142B that blew past the prior Street consensus of $125.54B.

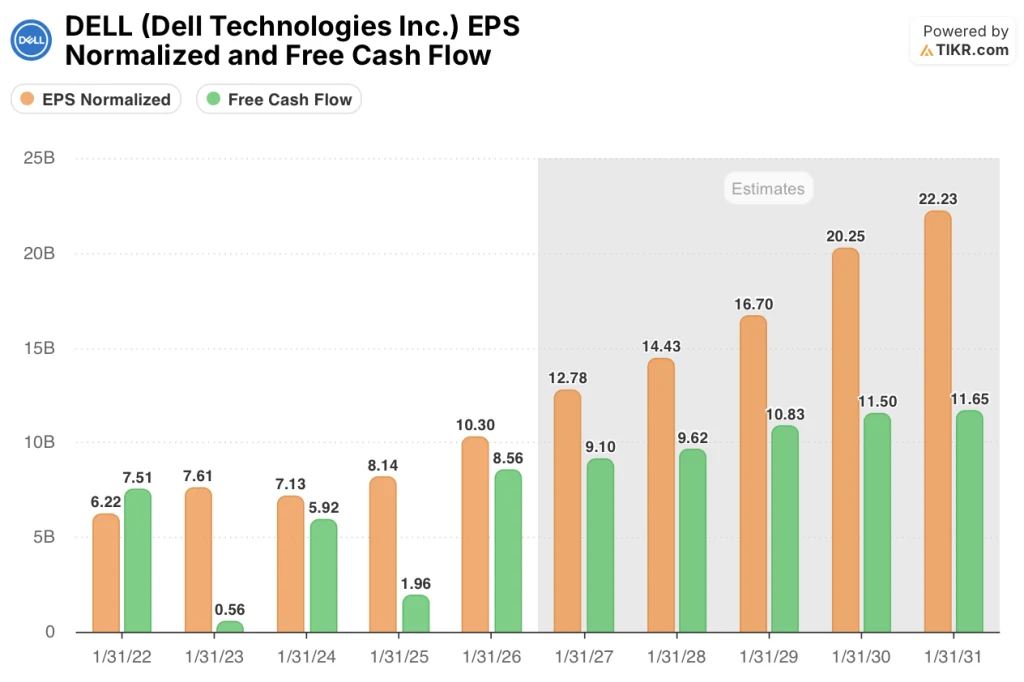

TIKR estimates FY2027 normalized EPS at $12.78, up 24.1% from FY2026’s $10.30, anchored by the $50B AI server revenue guide and a continued OpEx scaling story that has taken operating expenses from over 13% of revenue to 9.9% in Q4 alone.

Free cash flow surged 337% to $8.56B in FY2026 as AI server shipments scaled, and TIKR models $9.10B in FY2027 FCF, providing the fuel behind the 20% dividend hike to $2.52 per share annually and the $10B buyback authorization announced February 26.

The Street’s consensus mean target of $167.22 across 23 analysts — 14 buys, 5 outperforms, 6 holds, 1 sell — implies 12.1% upside from the March 18 close of $149.21, though that target was set against a consensus revenue estimate Dell has already surpassed with its own guidance.

Analyst price targets range from $110 to $220, where the bear case centers on memory cost inflation eroding CSG margins and the bull case reflects AI server demand sustaining the $50B trajectory Dell itself has guided; the memory pricing cycle — with DRAM spot prices up 5.5x over six months — is the single variable that separates those two outcomes.

What Does the Valuation Model Say?

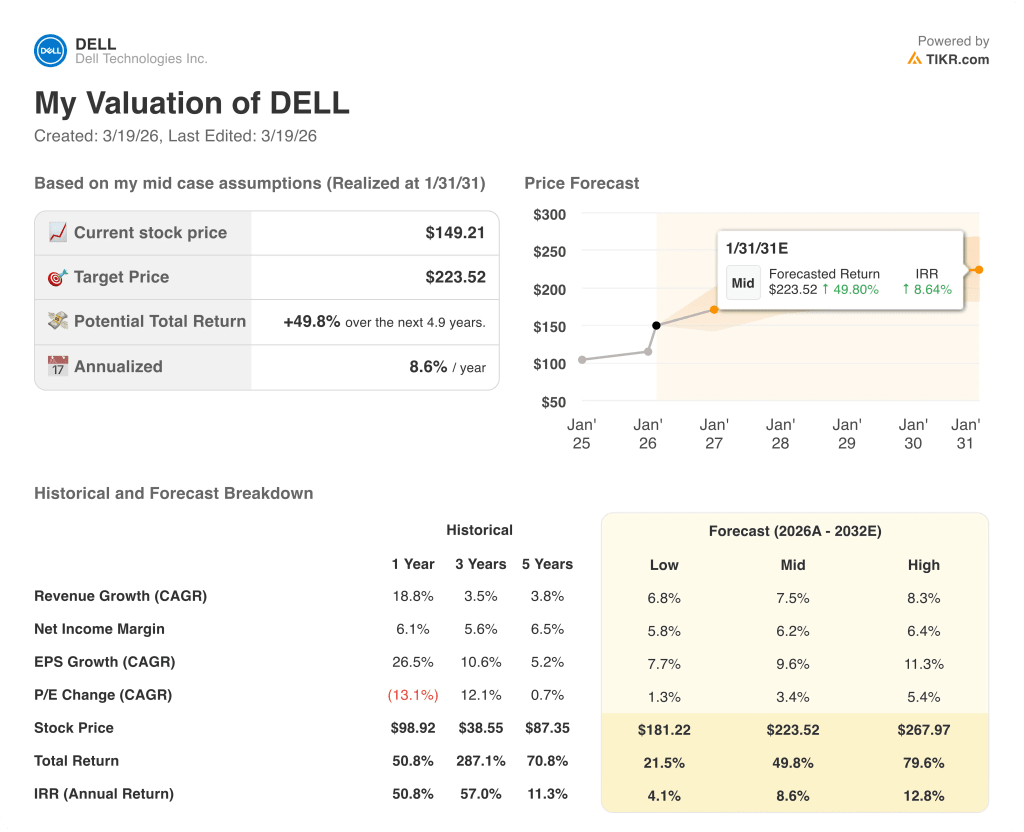

The TIKR mid-case target of $223.52, underpinned by a 7.5% forward revenue CAGR and 9.6% EPS CAGR through FY2031, implies 49.8% total return over 4.9 years at an 8.6% IRR, justified by Dell’s $64.1B in FY2026 AI orders and a backlog that provides forward revenue coverage with no comparable peer match.

Dell trades at roughly 11x forward earnings against a normalized EPS growth rate of 24.1% projected for FY2027 — a PEG ratio well below 1, which the $43B backlog and $50B AI revenue guide make difficult to dismiss as speculative.

The $43B AI backlog, overwhelmingly composed of Grace Blackwell server orders with Vera Rubin demand building in the 5-quarter pipeline, gives TIKR’s 7.5% forward revenue CAGR a concrete operational foundation that analyst models built before the February 26 guidance raise have not fully absorbed; TIKR’s mid-case target is $223.52.

CFO David Kennedy stated on the Q4 earnings call that the 5-quarter forward pipeline dollar value “has never been higher,” specifically calling out enterprise as the fastest-growing cohort — the segment that also drives higher-margin storage and services attach, the mix improvement that underpins the EPS compounding thesis.

If memory costs escalate faster than Dell’s pricing actions can offset — DRAM spot prices already up 5.5x in six months — CSG operating margins, already at 4.7% in Q4 and guided to the lower end of the long-term framework, compress further and break the OpEx leverage story supporting EPS growth.

Q1 FY2027 results, expected to show $13B in AI server revenue and non-GAAP EPS of $2.90 against a prior Street estimate of $2.37, will confirm whether the $50B full-year AI revenue guide is tracking and whether CSG margins have stabilized following the January 6 price increases.

Should You Invest in Dell Technologies Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DELL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Dell Technologies Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DELL stock on TIKR for Free →