Key Stats for CAVA Stock

- Past week’s performance: 3.1%

- 52-week range: $42 to $99

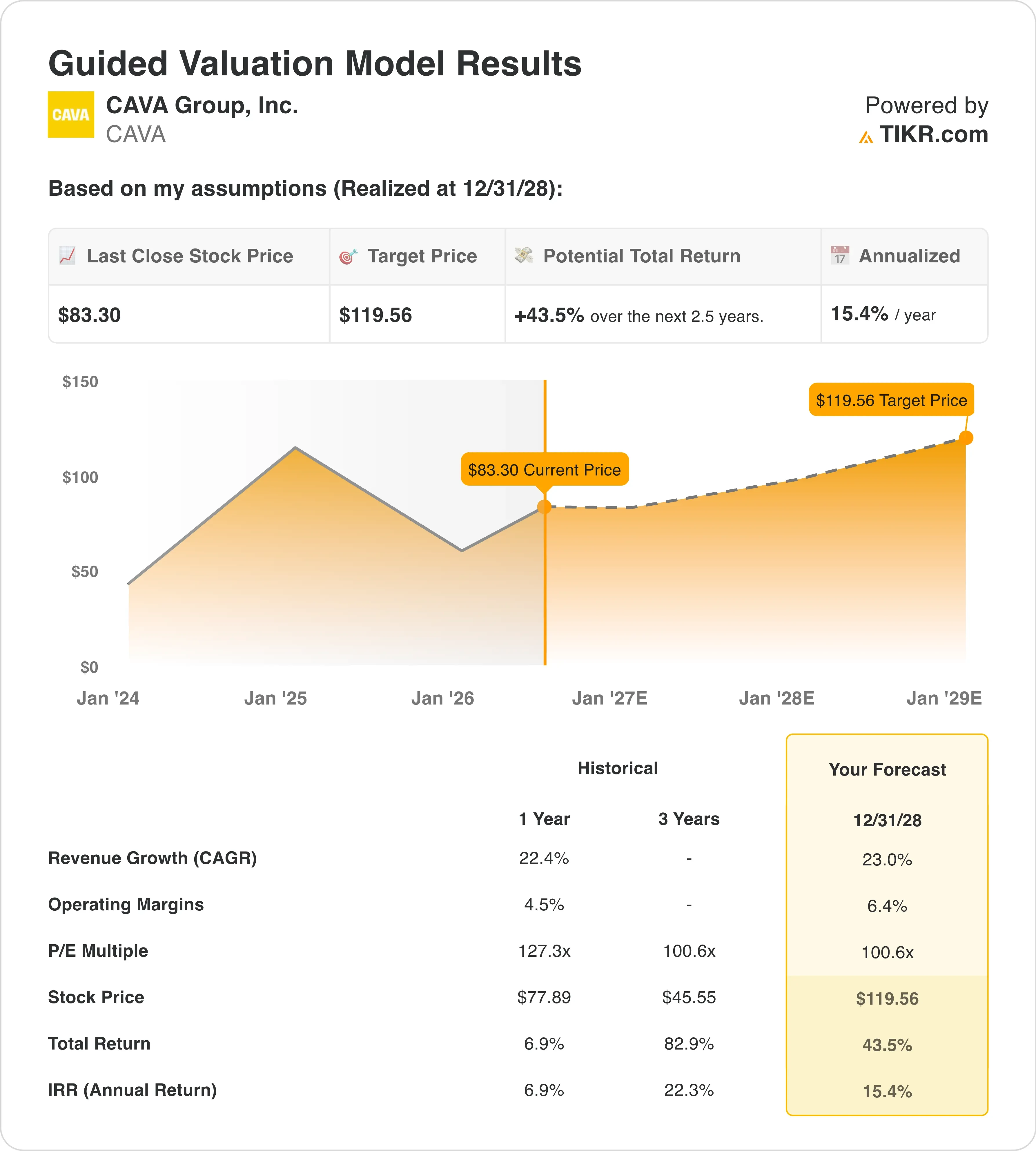

- Valuation model target price: $120

- Implied upside: +43.5% over the next 2.5 years

Value your favorite stocks like CAVA with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

A Record Quarter the Market Has Already Moved Past

CAVA Group (CAVA) surged after its May earnings report but has since retreated. The stock now trades near $83, well below its post-earnings peak. Investors are asking whether this year’s growth story is already fully priced in.

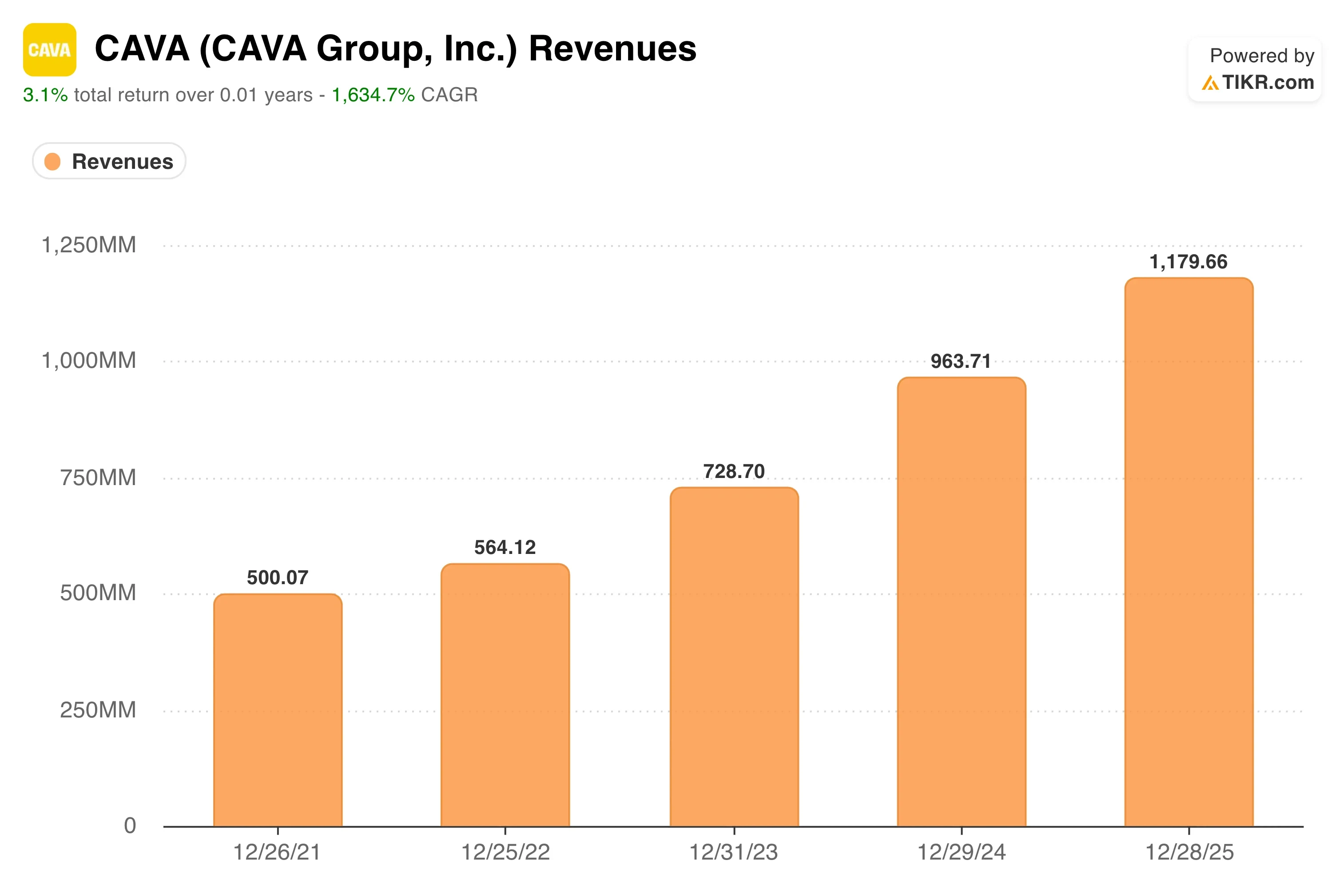

The Q1 numbers were genuinely strong. Revenue grew 32.2% year over year. Same-restaurant sales rose 9.7%, driven by guest traffic growth of 6.8%. Adjusted EBITDA rose 37.6% to $61.7 million. The company also opened 20 net new restaurants, bringing its total to 459 locations. That combination of traffic-led comparable sales and unit expansion is exactly what bulls want to see.

Sentiment has cooled since then. On June 24, Reuters reported that Darden Restaurants issued an earnings warning, citing higher costs and weaker traffic. While CAVA is fast-casual rather than full-service, the Darden warning reminded investors that consumer spending pressure is real. Large institutional holder Artal Participations also sold 3 million shares worth roughly $271 million in mid-June, adding supply pressure at a difficult moment.

CEO Brett Schulman noted that same-restaurant sales growth of 9.7% “speaks to the structural strength of our business” and its “compelling value proposition.” Going forward, CAVA stock will need continued traffic-led momentum and disciplined new-unit economics to justify its still-elevated multiple.

See analysts’ growth forecasts and price targets for CAVA (It’s free) >>>

Is CAVA Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 23%

- Operating Margins: 6.4%

- Exit P/E Multiple: 100.6x

Based on these inputs, the model estimates a target price of $120, implying 43.5% total upside and a 15.4% annualized return over the next 2.5 years.

Those assumptions require sustained execution. Revenue growing at 23% annually means CAVA must keep opening restaurants and growing same-store sales simultaneously. The one-year historical revenue CAGR of 22.4% suggests that the pace is achievable. But it leaves little room for a traffic slowdown.

Operating margins of 6.4% represent meaningful expansion from the current 4.5% level. That expansion depends on labor cost management, menu pricing discipline, and the benefits of scale. CFO Tricia Tolivar noted that new restaurant openings in 2026 are exceeding expectations, with average unit volumes of $3 million and productivity at 100% or greater. That is an encouraging sign for unit-level margin maturity.

The exit multiple of 100.6x is the most debated input. CAVA currently trades above 100x last-twelve-month earnings, so the model assumes the multiple holds rather than compresses. Chipotle, CAVA’s closest fast-casual comparable, saw its multiple compress materially after its high-growth phase. Dutch Bros, another high-growth concept, also commands a premium but has seen its multiple fluctuate sharply around earnings.

A forward revenue estimates chart covering the next three years is the most useful visual here. It shows whether the growth trajectory remains intact after the Q1 beat and whether the raised annual forecast has shifted analyst expectations for the rest of fiscal 2026.

See how CAVA’s growth compares to Chipotle and Dutch Bros on TIKR >>>

How CAVA Stacks Up Against Its Competitors

Chipotle (CMG) is the clearest benchmark for CAVA. Chipotle trades at a next-twelve-month P/E above 45x and generates operating margins above 16%. CAVA’s operating margins remain around 5%, so the profitability gap is wide. But Chipotle, at a similar early stage of national expansion, also carried thin margins and a high multiple, and it rewarded patient investors as the unit count scaled.

Dutch Bros (BROS) offers a different comparison. It is growing revenue rapidly, but its margins remain under pressure as it invests in new markets. Dutch Bros trades at a similarly elevated revenue multiple to CAVA. Yet its drive-through-only format generates less predictable traffic patterns than CAVA’s dine-in and digital mix. CAVA’s digital revenue reached 39.9% of total revenue in Q1, adding a recurring, higher-margin order channel that strengthens the competitive moat.

The key distinction is that CAVA’s Mediterranean format has not yet faced a credible national competitor. That absence gives CAVA pricing power that neither Chipotle nor Dutch Bros had to protect as aggressively in their early growth phases. Investors comparing the three on a forward revenue multiple basis will find CAVA at a slight premium to Chipotle but roughly in line with Dutch Bros. CAVA’s same-restaurant sales growth rate is running well above either peer right now, which partially justifies that premium.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What’s Driving CAVA Stock Going Forward?

New restaurant openings are the single most important forward driver. CAVA has been expanding into new Midwest markets, including Cincinnati, St. Louis, and Columbus. Each new market tests whether the brand’s appeal is truly national or concentrated in coastal and Sun Belt regions.

Same-restaurant sales growth will determine whether the raised full-year forecast proves conservative. The company guided for 3% to 5% same-restaurant sales growth for the full year. The Q1 result of 9.7% came in well above that range. But comparison periods get harder in the second half as the prior-year base strengthens.

Margin expansion is the catalyst investors are watching most closely. Every 100 basis points of operating margin improvement adds meaningfully to earnings per share. CFO Tolivar noted that the salmon menu launch, which began in Q2, will add 20 to 40 basis points of headwind from food and energy costs. So near-term margin progression must overcome that pressure before improvement becomes visible.

Digital ordering and catering growth also matter over the medium term. CAVA’s 39.9% digital revenue mix carries higher average check sizes and more predictable order patterns. As those channels grow as a share of system-wide sales, they support both revenue per location and overall margin improvement across the restaurant base.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in CAVA Group?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CAVA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CAVA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CAVA stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!