Key Stats for Box Stock

- 52-Week Range: $21.34 to $34.39

- Current Price: $26.46

- Street Mean Target: $32.50

- Market Cap: ~$3.7B

- LTM Gross Margin: 79.6%

- LTM EBIT Margin: 9.4%

- Forward 2-Yr Revenue CAGR: ~9%

- NTM P/E: ~16x

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

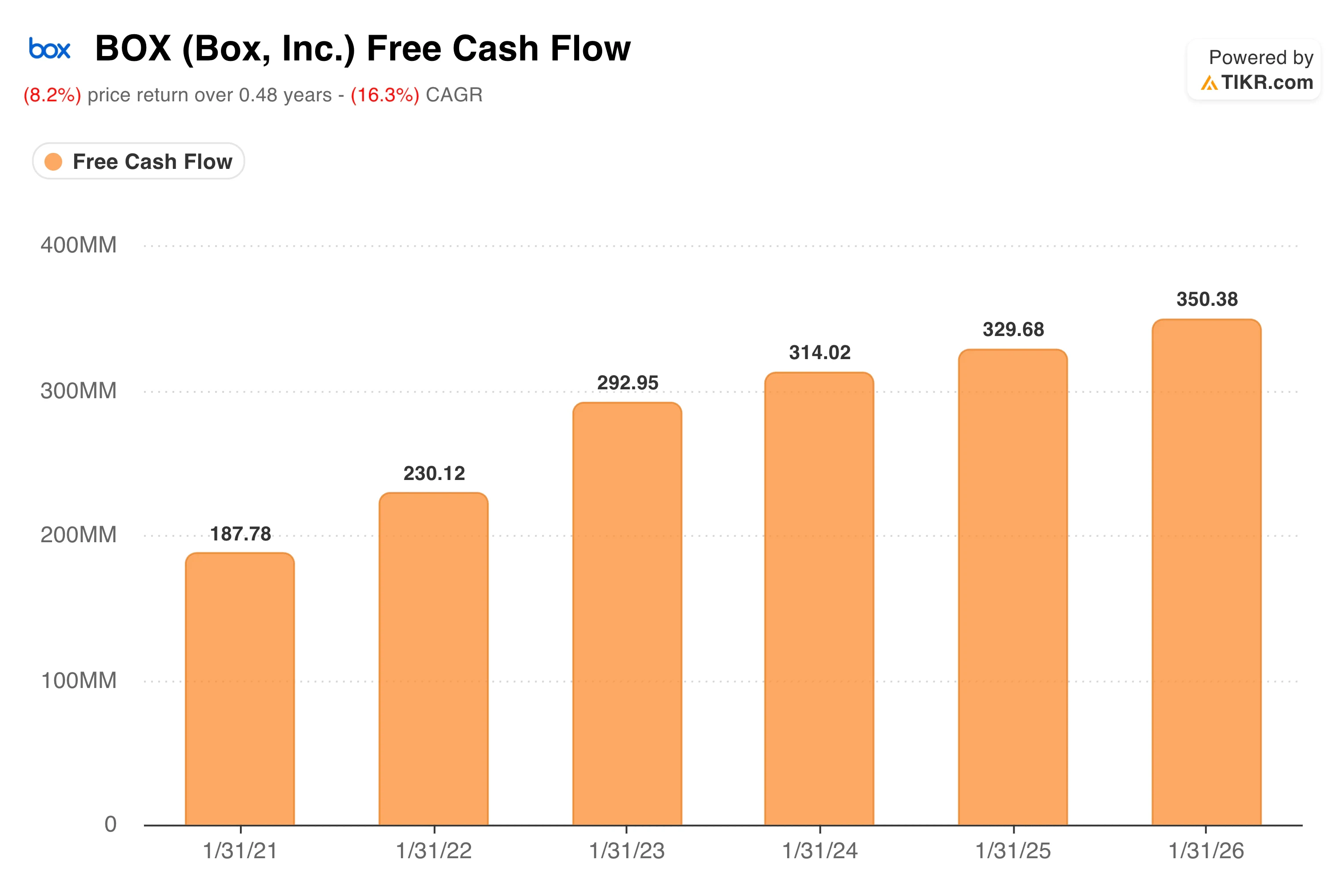

$350 Million in Free Cash Flow From a $3.7B Company

Box (BOX) is not a name that generates much excitement in investor circles. It does not have the growth rate of a hyperscaler, the brand recognition of Microsoft, or the AI hype of a pure-play software startup. What it does have is a remarkably consistent free cash flow profile that most investors walk right past.

Free cash flow has grown every year since FY2021, rising from $188 million to $350 million in FY2026, with no down year. That kind of consistency at a company with a market cap of roughly $3.7 billion is unusual. It implies the business is generating nearly a dollar of free cash flow for every ten dollars of market value, a ratio that tends to attract attention from value-oriented investors even when the growth story is modest.

Box makes its money selling cloud-based content management software to enterprise customers. Think of it as the secure infrastructure layer that large organizations use to store, share, and manage documents across their workforce. A hospital system uses it to manage patient records.

A law firm uses it to share sensitive contracts. A global retailer uses it to coordinate creative assets across dozens of markets. The common thread is security, compliance, and control, areas where Box has spent fifteen years building enterprise-grade capabilities that casual competitors cannot easily replicate.

The business model is subscription-based, which means revenue is highly predictable and gross margins run nearly 80%. Remaining performance obligations, essentially contracted future revenue not yet recognized, stood at $1.6 billion as of Q1 FY2027, up 12% year over year. That backlog provides solid visibility into the next several quarters of growth.

See the exact moment Wall Street upgrades BOX stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

11% Revenue Growth and the Enterprise Advanced Inflection

For most of the past four years, Box grew in the low to mid-single digits as the company invested heavily in its AI platform, while legacy customers renewed at modest rates. That dynamic shifted meaningfully in the most recent quarter.

Q1 FY2027 revenue came in at $306 million, up 11% year over year. That was Box’s first double-digit growth quarter in over three years, and it beat consensus estimates. Non-GAAP EPS was $0.37, up from $0.30 in the prior year period. Non-GAAP operating margin held at 27.7%, and the net retention rate improved to 105%, meaning that, on average, existing customers spent more with Box than they did 12 months ago.

The driver behind the reacceleration is Enterprise Advanced, Box’s premium tier that bundles AI workflow automation, intelligent document processing, and advanced security controls into a single offering. Enterprise Advanced customers now represent 10% of total revenue, up from a standing start just over a year ago.

CEO Aaron Levie told investors that customers are adopting Enterprise Advanced specifically to connect their unstructured data to AI agents, allowing them to build intelligent workflows and automate work at scale.

Box has also moved aggressively on AI partnerships. The company announced integrations with NVIDIA’s Agent Toolkit, Anthropic’s Claude, and Google’s Gemini Enterprise during the quarter, positioning Box as the secure content layer that enterprise AI deployments plug into rather than a standalone product competing against them.

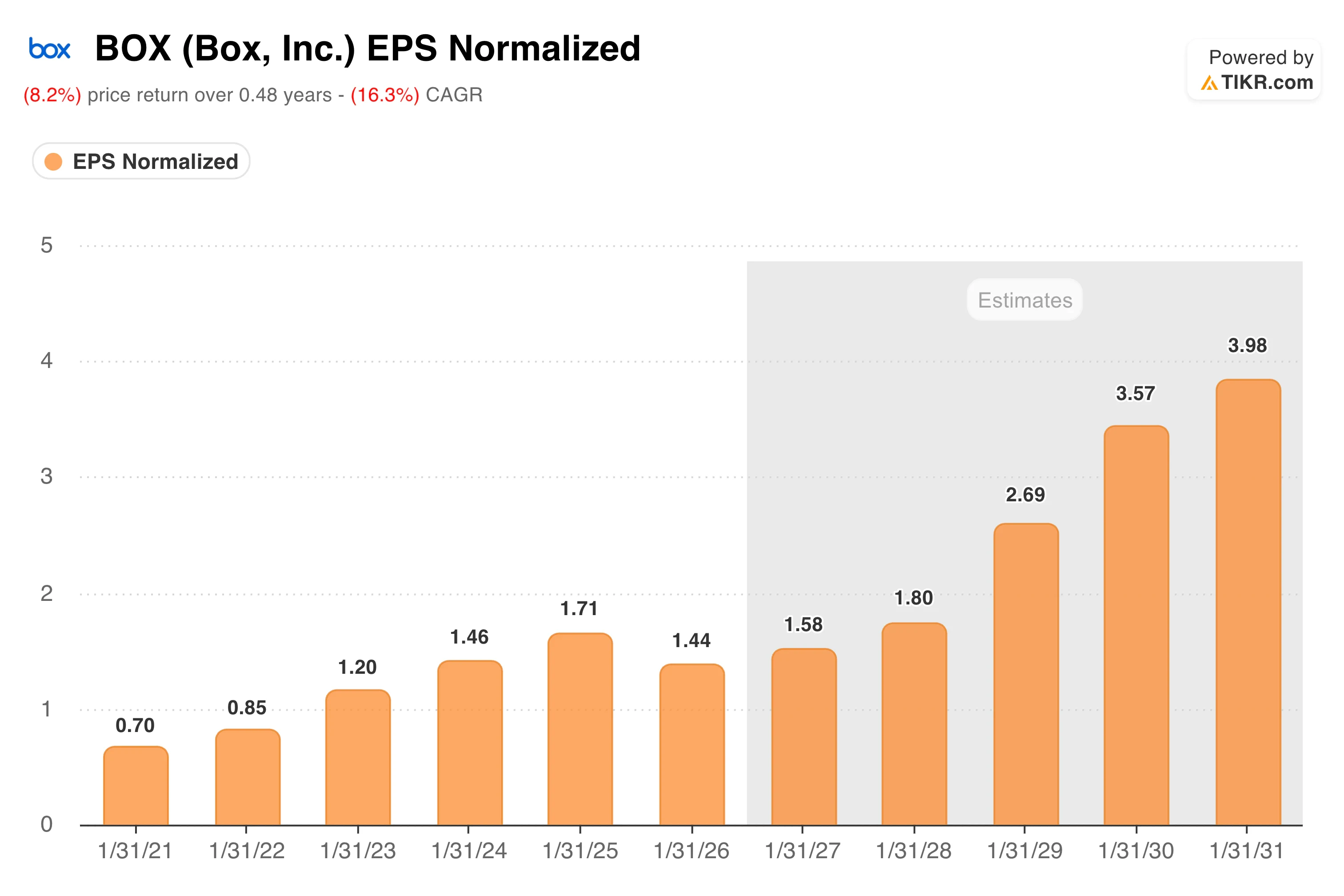

The EPS chart tells a nuanced story. Earnings dipped in FY2026 as Box accelerated investment in its AI platform, but free cash flow continued to grow throughout the year.

The consensus estimate path shows EPS recovering and compounding toward roughly $4.00 by FY2031 as Enterprise Advanced scales and margin leverage returns. The investment spend looks deliberate rather than distressed.

Track the quarterly results and the trajectory of BOX stock on TIKR for free →

The Model Sees 43% Upside. Here’s What It Requires.

TIKR’s valuation model targets around $38 for Box in the mid case, implying a total return of around 43% over roughly four and a half years, or about 8% annualized.

The mid case assumes around 6% annual revenue growth, net income margins expanding to roughly 18%, and modest EPS growth of around 7% per year.

The high case reaches around $58, implying nearly 10% annualized returns. That scenario requires revenue growth closer to 7% and net income margins approaching 19%, which would demand that Enterprise Advanced continue to scale and that AI consumption revenue add a meaningful layer on top of the existing subscription base.

The bear case risk is real. Box competes directly against Microsoft SharePoint and OneDrive, which come bundled into the Microsoft 365 suite that most enterprises already pay for. Google Drive presents the same bundling challenge from the other direction.

Box’s answer is that security, compliance, and AI workflow depth differentiate it from generalist storage products, and the enterprise customer base has so far validated that argument through steady renewals and modest but improving net retention.

Should You Invest in Box, Inc.?

Box is not a high-growth story, but at 16x forward earnings and under 10x free cash flow, it does not need to be. The AI platform is gaining real traction, the balance sheet is clean, and the cash generation is durable.

The risk is that Microsoft and Google continue bundling content management deeper into their existing suites, making it harder for Box to justify a standalone price. Investors comfortable with that competitive dynamic will find the valuation genuinely attractive.

Pull the full TIKR model for BOX, including EBITDA estimates through 2030, on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!