Key Stats for Arm Holdings Stock

- 52 Week Range: $100 to $453

- Current Price: around $322

- Street Target Price (Mean): around $297

- Street Target Price (High): around $500

- Market Cap: around $337 billion

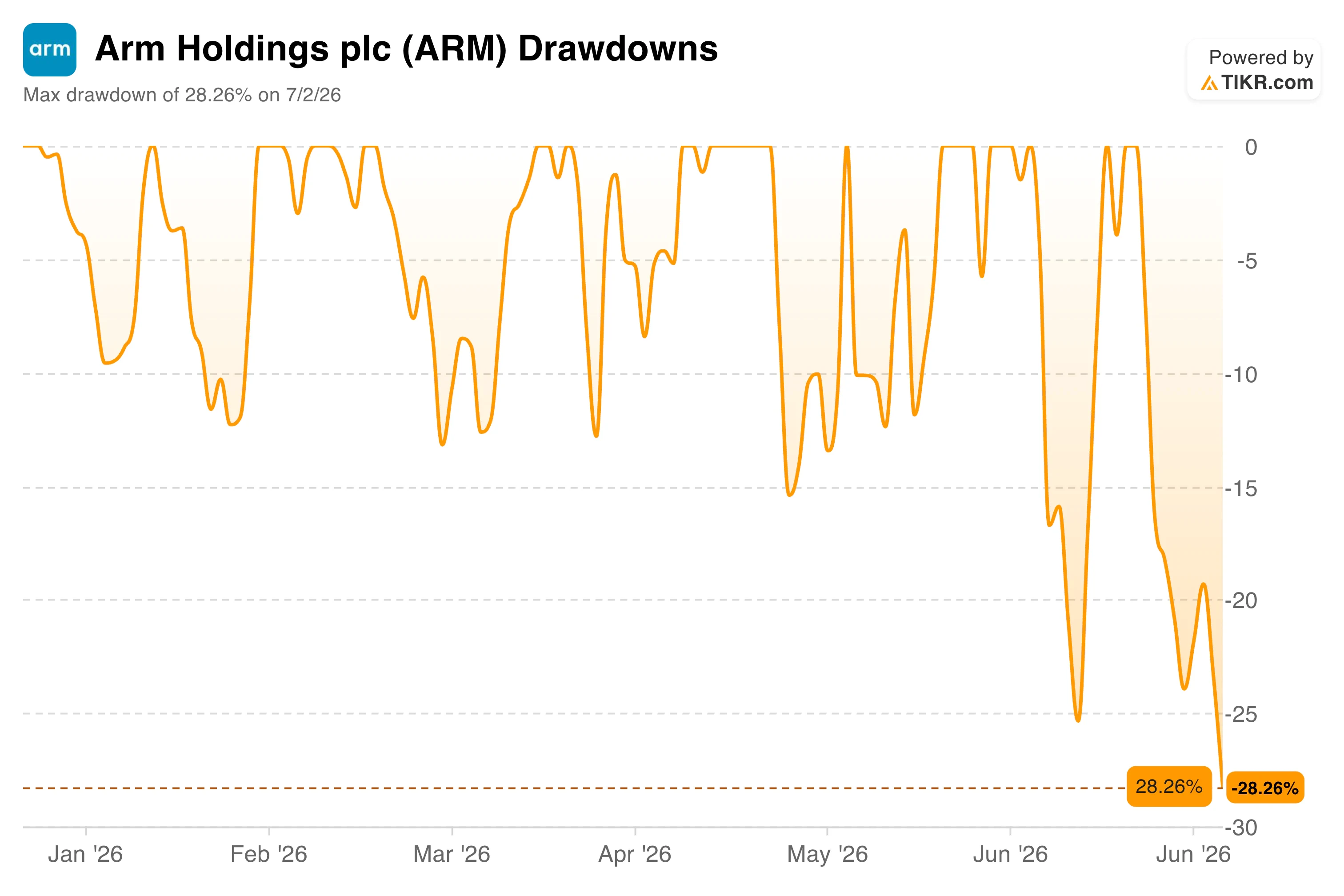

- Max Drawdown: around 28% from 52-week highs

- Fiscal Q4 Revenue: $1.49 billion, up 20% year over year

- Fiscal Q4 Licensing Revenue: $819 million, up 29% year over year

Analyze your favorite stocks like Arm Holdings with TIKR (It’s free) >>>

A Record Quarter That the Stock Did Not Reward

ARM’s (ARM) fiscal fourth-quarter results were about as strong as a chip company can post. Revenue reached $1.49 billion, up 20% year over year and ahead of consensus, while licensing revenue jumped 29% to $819 million and royalty revenue grew 11% to $671 million.

Data center royalties more than doubled. Full-year revenue hit a record $4.92 billion, marking the third straight fiscal year of growth above 20%.

None of that stopped the stockf from falling 7% the next day. The issue was not the quarter itself but what management said about the road ahead.

CEO Rene Haas told investors that customer demand for Arm’s new AGI CPU had already reached over $20 billion within six weeks of launch, yet the company has only secured manufacturing capacity to fulfill the first $1 billion of that demand. Management also flagged that smartphone unit growth could turn negative due to a memory chip shortage affecting the broader handset supply chain.

The Drawdowns chart below shows how sharply the stock has reacted to news like this all year. Arm has swung repeatedly between roughly flat and drawdowns exceeding 20%, and the current reading of 28% is close to the worst level of 2026 so far.

Value Arm Holdings instantly (Free with TIKR) >>>

Why the Growth Story Still Looks Intact

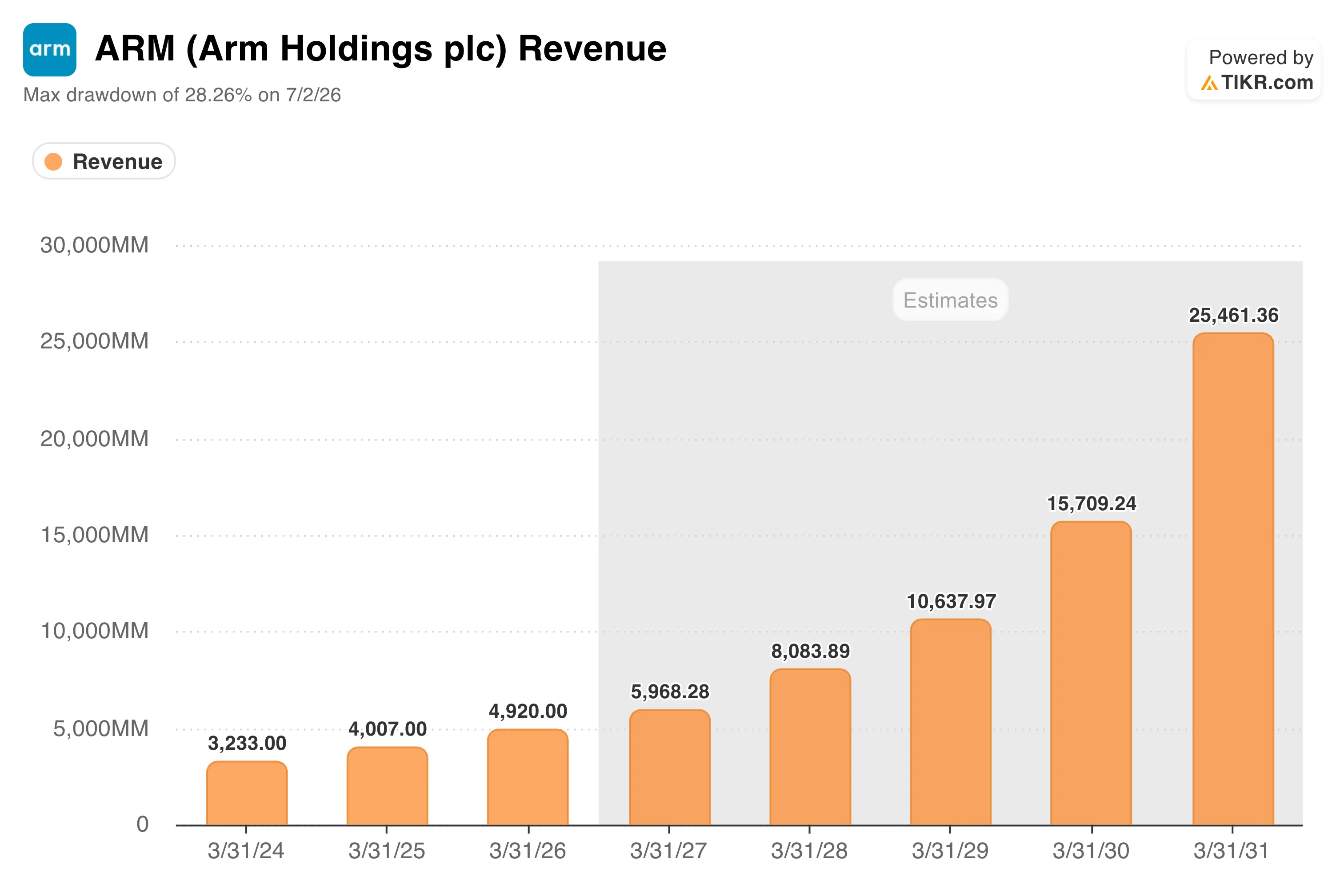

Strip away the supply headline, and the underlying growth trajectory has not changed. The Revenue chart below shows actual revenue climbing from around $3.2 billion in fiscal 2024 to just under $5 billion in fiscal 2026, with consensus estimates projecting that growth to accelerate sharply over the next five years, reaching around $25 billion by fiscal 2031.

That acceleration depends on royalty revenue continuing to compound as more chips ship with Arm’s newer architecture built in, and licensing revenue continuing to signal future design wins years in advance. Both trends were visible in this quarter.

Licensing revenue often acts as a leading indicator, since customers typically license Arm’s architecture years before shipping the resulting chips, and a 29% jump suggests a healthy pipeline of future royalty revenue regardless of near term supply friction.

What the Street Is Actually Pricing In

Given how much Arm’s valuation model output distorts when it assumes a decade of hypergrowth held constant, a Street Targets view offers a more grounded read on where consensus actually sits today.

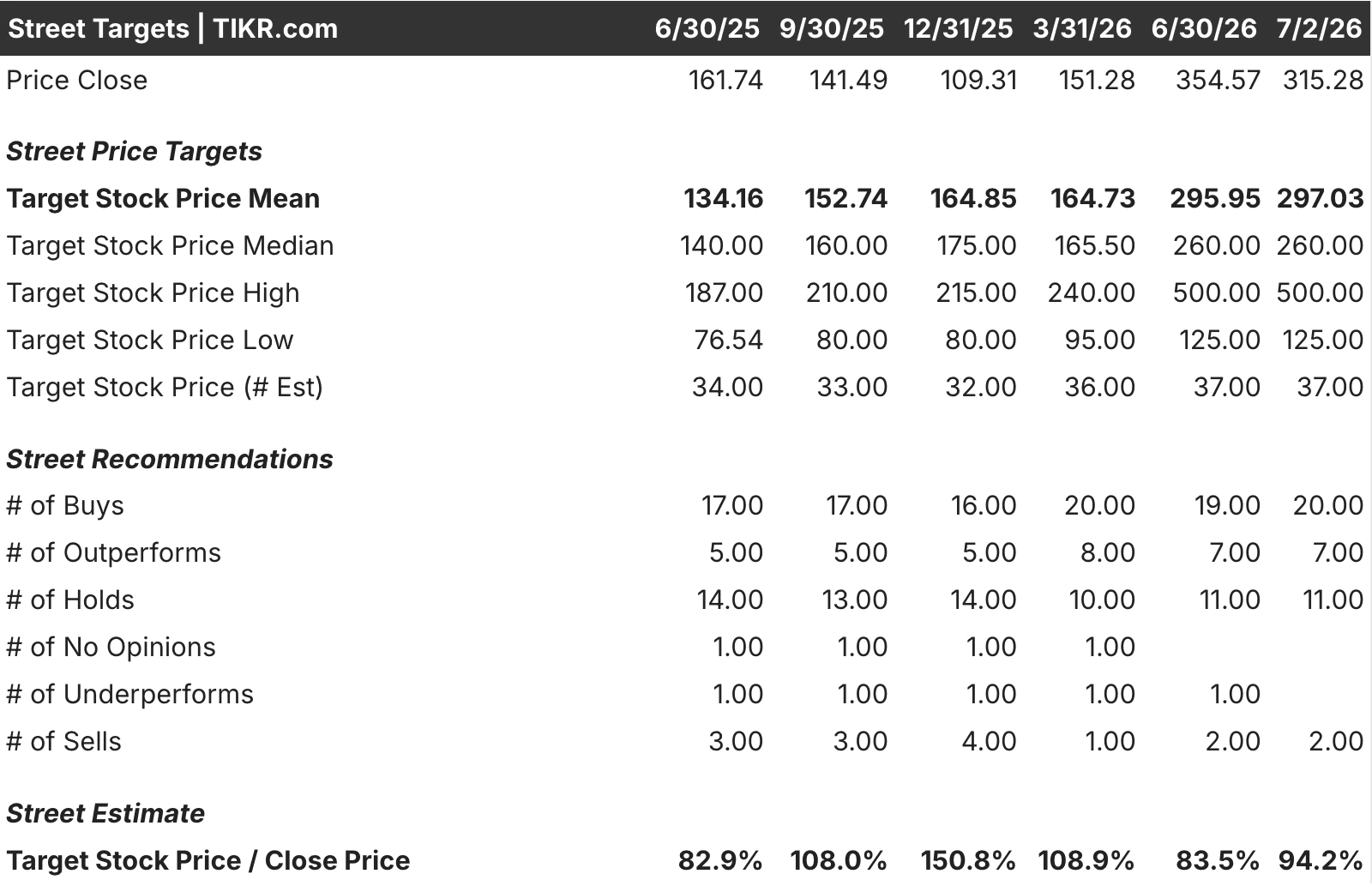

The mean analyst target has climbed from around $134 a year ago to around $297 today, tracking the stock’s own rally over that period.

What stands out is that Arm’s current price of around $315 is slightly above the mean target, suggesting the average analyst view is that the stock has run a bit ahead of fair value in the near term.

The high target of $500 reflects the bull case built on data center and AGI CPU adoption, while the low target of $125 reflects how wide the range of outcomes remains for a company still early in monetizing its newest products.

See analysts’ growth forecasts and price targets for Arm Holdings (It’s free) >>>

Should You Invest in Arm Holdings?

Arm’s fundamentals, licensing momentum, royalty acceleration, and data center adoption are all pointing in the same direction, and the recent selloff reflects a supply constraint rather than a demand problem.

The stock’s premium valuation leaves little room for execution missteps, and the current price, above the Street’s mean target, suggests near-term upside may be limited until manufacturing capacity catches up with demand.

Investors comfortable with a long runway and continued volatility may still find the growth case compelling, while those focused on near-term valuation support may want to wait for a clearer signal on capacity.

See analysts’ growth forecasts and price targets for Arm Holdings stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!