Ally Financial Inc. (NYSE: ALLY) trades near $40/share, up slightly this year as earnings and margins stabilize. The company remains disciplined in loan growth and cost control, while its expanding digital bank continues to strengthen its funding base.

Recently, Ally reported solid Q3 2025 results, highlighting improved credit trends and stable net interest income despite a softer auto lending market. Management also announced plans to expand its digital offerings and strengthen deposit growth, signaling confidence in long-term profitability. These updates suggest Ally is adapting well to a slower rate environment while maintaining focus on shareholder returns.

This article explores where Wall Street analysts think Ally’s stock could trade by 2027. We have combined consensus price targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

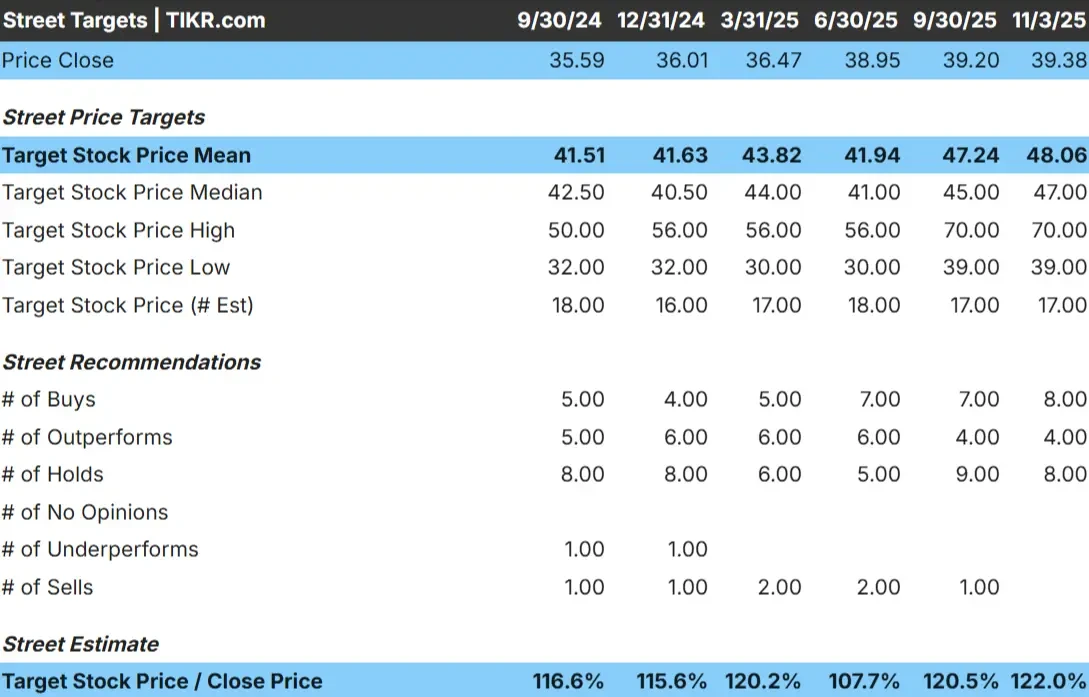

Ally Financial trades near $40/share today. The average analyst price target is around $48/share, suggesting roughly 22% upside over the next year. Forecasts remain fairly consistent, signaling cautious but improving sentiment:

- High estimate: ~$70/share

- Low estimate: ~$39/share

- Median target: ~$47/share

- Ratings: 8 Buys, 4 Outperforms, 8 Holds

Analysts expect gradual gains as funding costs stabilize and credit performance continues to improve. For investors, this points to modest upside potential. Ally may not soar, but steady execution and consistent capital returns could lift the stock as rate pressures ease.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Ally Financial: Growth Outlook and Valuation

Ally’s fundamentals reflect a healthy, disciplined business model built for resilience:

- Revenue is expected to grow about 5% annually through 2027

- Operating margins remain strong around 43%

- Shares trade near 8x forward earnings, below their historical average

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 8x forward P/E suggests Ally could reach about $50/share by 2027

- That implies around 28% total return or roughly 12% annualized gains.

For investors, these figures support the case for steady long-term compounding rather than explosive growth. With its solid capital base, healthy liquidity, and strong commitment to dividends and buybacks, Ally looks like a dependable value opportunity in an otherwise uncertain lending environment.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Ally’s digital-first banking model continues to be a competitive advantage. Its strong online deposit base provides a low-cost funding source, helping the company maintain healthy margins even as rates fluctuate. Non-interest income from insurance and investment products also adds stability, reducing reliance on auto lending cycles.

Management remains focused on efficiency and shareholder returns, with steady dividends and consistent buybacks reflecting confidence in long-term earnings power. For investors, these strengths suggest Ally has the fundamentals to compound value steadily as the economy normalizes and credit conditions remain contained.

Bear Case: Credit and Competition Risks

Despite these positives, Ally’s earnings remain exposed to consumer credit cycles. A rise in delinquencies or weakness in used-car pricing could weigh on loan profitability. The auto market’s sensitivity to economic slowdowns adds another layer of risk that investors should monitor closely.

Competition is also tightening, both from large national banks and digital-first fintech lenders. As loan pricing becomes more competitive, sustaining margins could be challenging. For investors, this means short-term volatility is possible even if long-term fundamentals stay intact.

Outlook for 2027: What Could Ally Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 8x forward P/E suggests Ally could trade near $50/share by 2027. That would represent roughly 28% upside from current levels, or about 12% annualized returns.

While not a high-growth story, this outlook assumes steady earnings recovery and continued capital discipline. For investors, it paints a picture of reliable, compounding returns driven by efficiency, stable credit, and shareholder-friendly policies.

Ally may not deliver outsized gains, but it remains a well-managed, income-generating value stock that can reward patience as credit markets stabilize and the digital banking platform continues to expand.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>