T-Mobile US, Inc. (NASDAQ: TMUS) trades near $205/share, down roughly 12% over the past year. Despite the pullback, the company continues to deliver strong free cash flow and solid profitability, showing that its core business remains resilient even in a mature wireless market.

Recently, T-Mobile reported strong postpaid customer growth in its latest quarter and continued returning capital to shareholders through an expanded buyback program. The results show that its 5G investments and customer-focused strategy are paying off, while management’s confidence in long-term cash generation remains clear.

This article explores where Wall Street analysts think T-Mobile could trade by 2027. We’ve pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

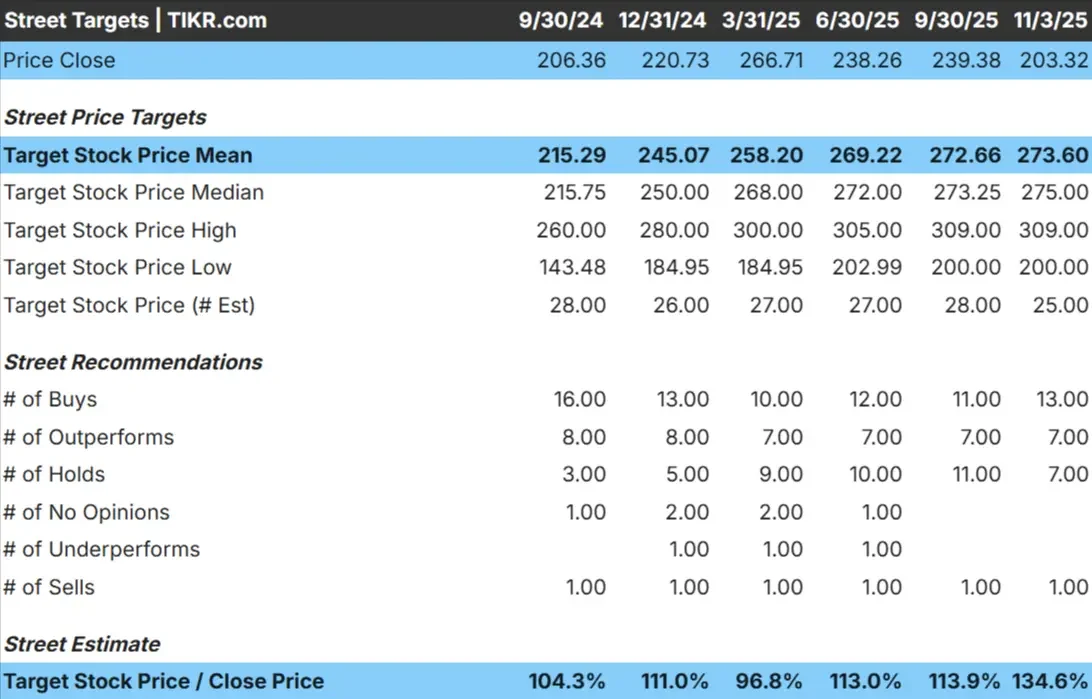

T-Mobile trades near $205/share today. The average analyst price target is $274/share, suggesting roughly 34% upside over the next year. Forecasts show a confident but balanced outlook among analysts:

- High estimate: ~$309/share

- Low estimate: ~$200/share

- Median target: ~$275/share

- Ratings: 13 Buys, 7 Outperforms, 7 Holds, 1 Sell

For investors, analysts see meaningful upside as the company continues delivering steady earnings growth, margin expansion, and strong free cash flow. With T-Mobile returning billions through buybacks and maintaining leadership in 5G coverage, it remains one of the best-positioned telecom names for long-term compounding.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

T-Mobile: Growth Outlook and Valuation

T-Mobile’s fundamentals continue to strengthen:

- Revenue is projected to grow ~6–7% annually through 2027

- Operating margins are expected to reach ~24%

- Shares trade at ~19× forward earnings, slightly below their 5-year average of ~30×

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 18.9× forward P/E suggests the stock could reach ~$330/share by 2027.

- That represents about 62% total upside, or roughly 25% annualized returns.

For investors, these figures imply T-Mobile remains attractively valued for a large-cap telecom stock. Its earnings momentum, disciplined cost structure, and consistent buybacks create a setup that could drive steady returns well above the broader market over the next few years.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

T-Mobile’s leadership in 5G coverage and ongoing growth in fixed wireless broadband continue to set it apart in the U.S. telecom space. The company is expanding its broadband footprint faster than expected, reaching millions of new households each year.

At the same time, T-Mobile’s cost efficiency and integration success from the Sprint merger are fueling margin gains. The company’s focus on customer retention, premium service plans, and consistent network upgrades supports its ability to grow earnings even as the wireless market matures.

For investors, these factors suggest T-Mobile is positioned for steady compounding. Its combination of network strength, disciplined spending, and shareholder returns provides a clear edge over peers heading into 2027.

Bear Case: Slower Growth and Competition

Even with strong fundamentals, the risks are worth noting. The U.S. wireless market is maturing, and growth could slow if subscriber additions or broadband net gains taper off. Competitive pressure from Verizon and AT&T could also intensify, especially if they respond with deeper pricing discounts.

Another concern is capital intensity. Maintaining network leadership requires ongoing investment, and any increase in spectrum or infrastructure spending could temporarily weigh on free cash flow.

For investors, the key risk is that T-Mobile’s growth moderates just as expectations remain high. That could limit upside if earnings or subscriber growth underperform in 2026–2027.

Outlook for 2027: What Could T-Mobile Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests T-Mobile could trade near $330/share by 2027, representing about 62% total upside, or roughly 25% annualized returns.

That outcome assumes mid-single-digit revenue growth, modest margin expansion, and continued share repurchases. If management delivers on these targets, investors could see one of the strongest total return profiles in large-cap telecom.

For investors, T-Mobile looks like a high-quality compounder that blends growth, cash generation, and shareholder-friendly execution. While risks from competition and capital costs remain, the long-term setup still favors steady value creation through 2027.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>