Key Takeaways:

- The 2-Minute Valuation Model values Dutch Bros stock at $80 per share in 2 years.

- That’s a potential 11% upside from today’s price of $72 per share.

- BROS stock is projected to grow EPS by an impressive 127% over the next 3 years.

- Despite strong growth, the stock’s premium valuation limits near-term upside potential.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Dutch Bros (BROS) has rapidly emerged as one of the fastest-growing coffee chains in America. It challenges established players with a drive-thru-focused model and energetic brand culture. The company continues to expand aggressively across the United States, targeting thousands of locations in the coming years.

With BROS stock now trading at $72 per share, investors question whether this growth story justifies the stock’s premium valuation.

Let’s analyze whether Dutch Bros stock can deliver the kind of returns that would make it worth adding to your portfolio today.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings per share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why Dutch Bros Stock Looks Overvalued

Forecast

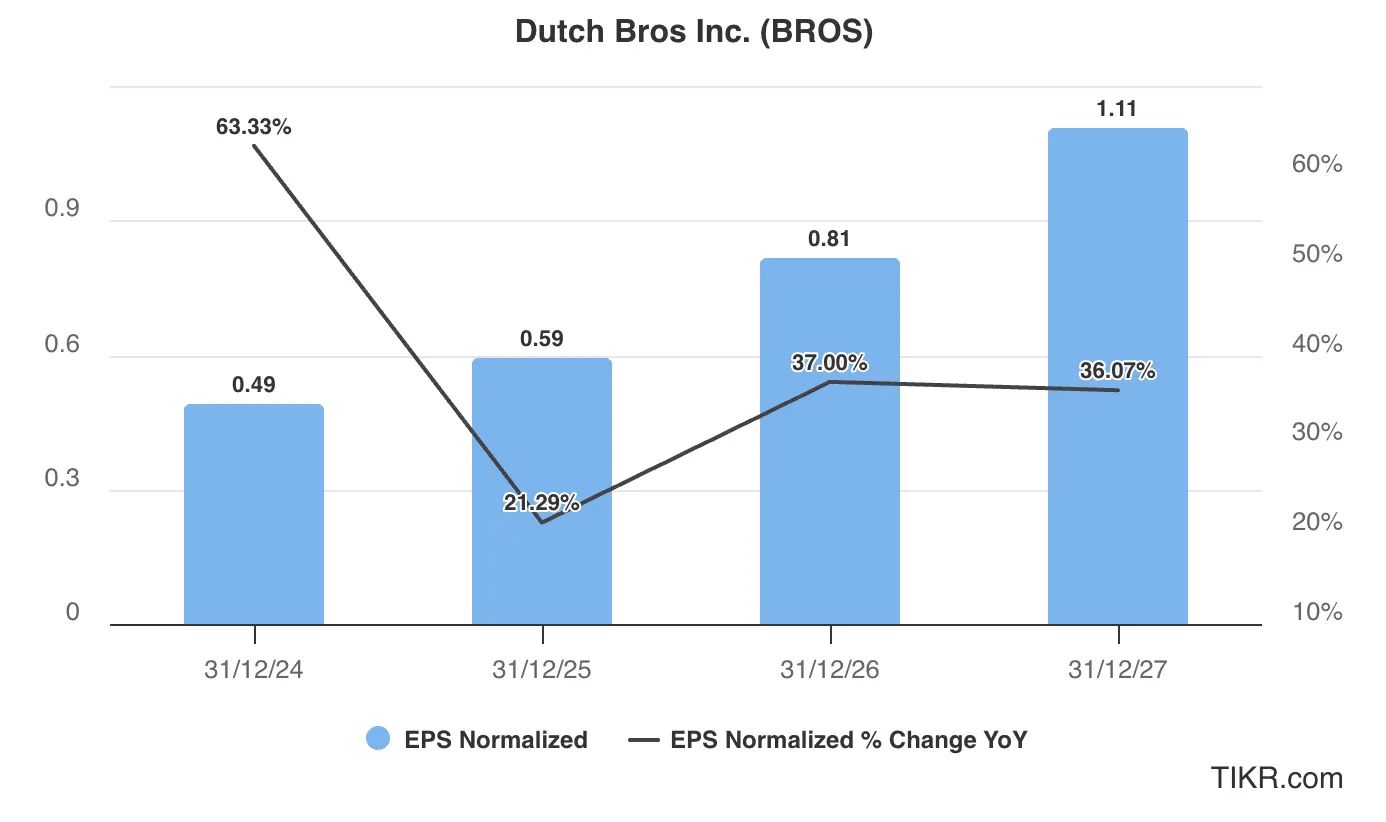

Based on analyst estimates shown in the chart below, Dutch Bros is expected to achieve remarkable earnings growth over the next three years.

EPS is projected to grow from $0.49 in 2024 to $1.11 by 2027, representing a 127% total increase over three years.

Despite a challenging macro environment in 2025, earnings are forecast to expand by 21% this year. Moreover, EPS growth is on track to accelerate by 37% in 2026 and 36% in 2027.

This earnings growth for Dutch Bros stock is likely to be driven by:

- Aggressive store expansion: The company is rapidly increasing its footprint, with plans to grow from approximately 850 shops today to over 1,500 by 2027.

- Same-store sales growth: Dutch Bros continues to experience strong comparable store sales, reflecting its popularity and customer loyalty.

- Margin improvement: As the store base matures and corporate infrastructure scales, operating leverage should drive higher margins.

- Menu innovation: The company regularly introduces new beverages and food items that drive traffic and increases average ticket size.

For our valuation, we’ll use a slightly conservative 2027 EPS estimate of $1 for Dutch Bros stock.

Check out Dutch Bros’ full analyst estimates (It’s free) >>>

Is BROS Stock Trading at a Premium?

Dutch Bros stock currently trades at around 116x forward earnings, below its three-year historical average of 120x, as shown in the P/E chart.

While the stock’s valuation has moved lower in recent months, it continues to trade at a lofty multiple in May 2025.

For our valuation, we’ll use a relatively conservative forward P/E multiple of 80x, slightly below where the stock trades today, acknowledging the volatile macro environment.

It’s typical for high-quality businesses today to trade at a P/E ratio that’s 2x annual earnings growth. With earnings expected to grow about 37% annually in 2026 and 2027, an 80x forward P/E multiple looks pretty generous for the stock.

Fair Value of Dutch Bros Stock

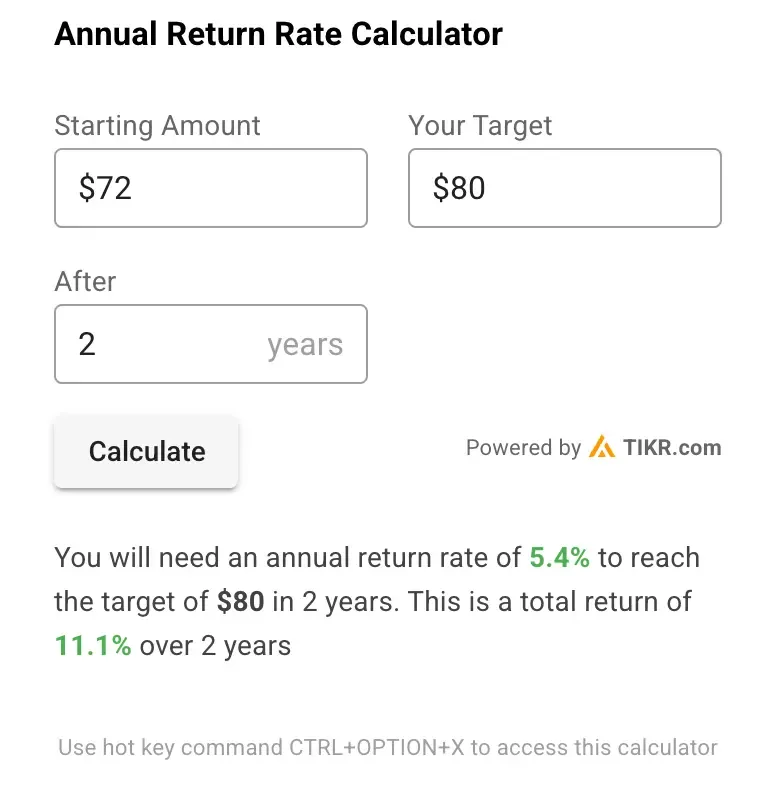

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $1

- Conservative forward P/E multiple: 80x

Expected Normalized EPS ($1) * Forward P/E ratio (80x) = Expected Share Price ($80)

The 2-year expected Dutch Bros stock price we would get from this valuation is $80 per share.

With BROS stock currently trading at around $72 per share, this implies a potential upside of 11% over the next two years or a 5% annualized return.

Dutch Bros stock will likely deliver below-average market returns at this price, given that the broader market’s average annual returns over the long term have been around 10%.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

What is the Target Price for Dutch Bros Stock?

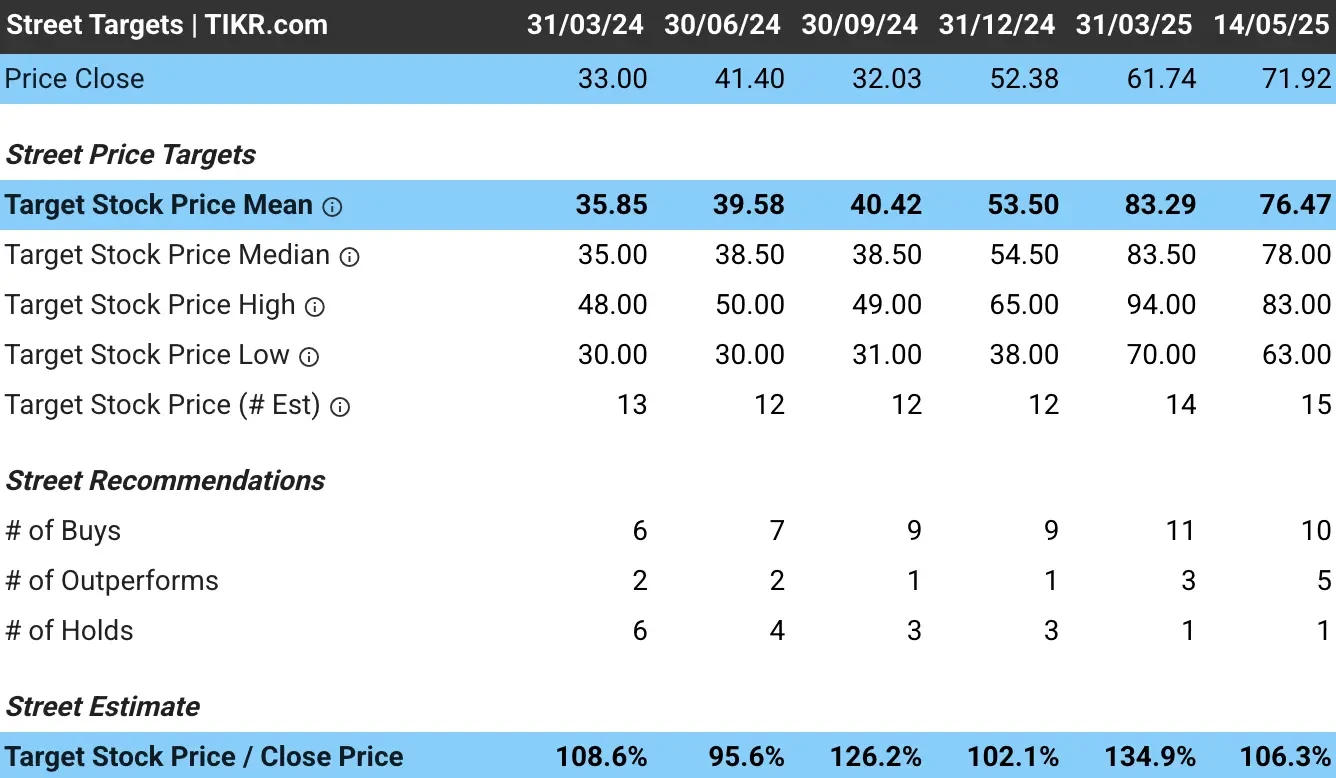

Analysts think that BROS stock only has a little upside today.

Analysts have an average price target of around $76 per share for Dutch Bros stock, indicating they see about 6% upside today based on its current share price:

Some analysts see even greater upside, with price targets ranging as high as $83 per share, suggesting potential upside of around 15% from current levels.

Still, with high estimates calling for 15% upside, it’s very possible that the stock can underperform at its current valuation.

Risks to Consider

Despite the strong growth outlook that the business is expected to see, investors should be aware of several risks that could impact Dutch Bros’ growth trajectory:

- Valuation sensitivity: At 115x forward earnings, disappointing growth figures could lead to significant multiple compression.

- Increased competition: The specialty coffee market is highly competitive, with established players like Starbucks and emerging chains vying for market share.

- Rising costs: Inflationary pressures affecting labor, ingredients, and construction could pressure margins and slow expansion.

- Geographic concentration: The company is still heavily concentrated in western states, and success in new markets isn’t guaranteed.

TIKR Takeaway

Dutch Bros stock presents a mixed investment case at its current valuation. While its growth story remains compelling, with strong unit economics and a clear expansion runway, the stock’s premium valuation limits near-term upside potential.

The projected 11% return over two years, translating to a 5% annual return, falls short of what many investors might expect from a high-growth company.

This suggests that the current stock price already reflects much of Dutch Bros’ growth potential for the next few years.

For long-term investors who believe in the company’s ability to successfully execute its ambitious expansion plans and eventually grow into its valuation, Dutch Bros could still be an attractive addition to a growth portfolio. However, those seeking immediate returns might want to wait for a more favorable entry point.

Is Dutch Bros stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!