Key Stats for United Parcel Service Stock

- Past-Week Performance: -5%

- 52-Week Range: $82 to $122.4

- Current Price: $96.8

What Happened?

United Parcel Service (UPS), the world’s largest package delivery company, is executing the most aggressive network downsizing in its 118-year history, deliberately shedding roughly $5 billion in Amazon revenue to rebuild around higher-margin freight, with shares sitting 21% below their 52-week high at $96.84.

On January 27, UPS guided 2026 consolidated revenue to $89.7 billion and operating margin to approximately 9.6%, announcing plans to cut up to 30,000 jobs, close 24 facilities in the first half, and remove another 1 million Amazon packages per day from its network.

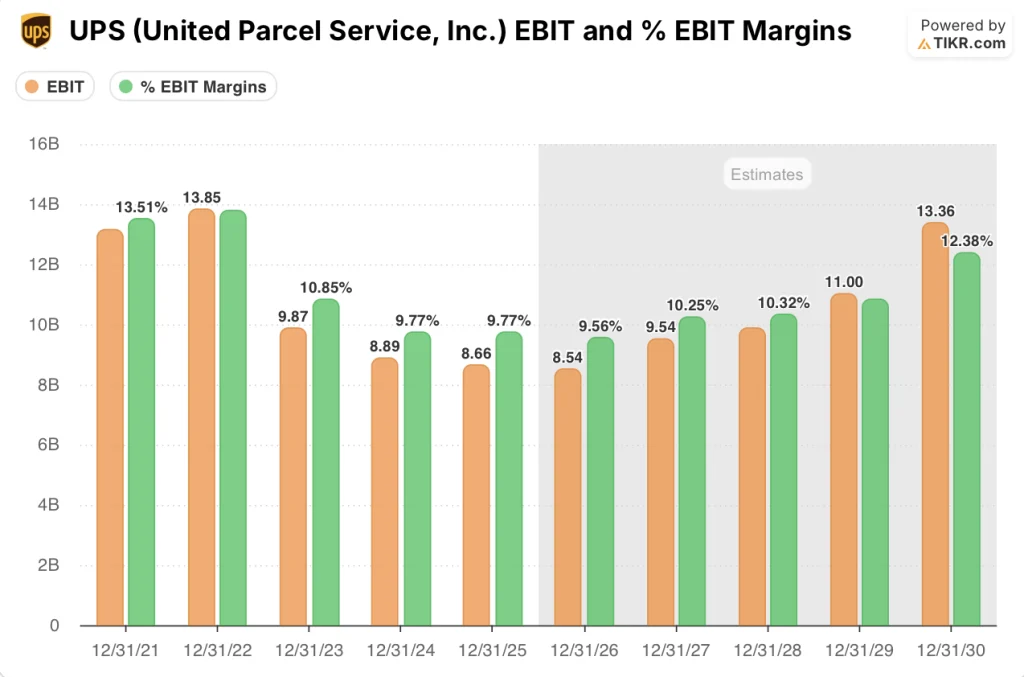

Cost per piece in UPS’s 127 automated facilities runs 28% below conventional buildings, and the company closed 93 buildings in 2025 while still posting its eighth consecutive year as industry leader in on-time peak-season service, a combination no direct competitor has matched.

CEO Carol Tomé stated on the Q4 2025 earnings call that “June of 2026 will be the inflection point,” tying the claim directly to the completion of the Amazon glide-down and the outsourcing of Ground Saver last-mile delivery back to the U.S. Postal Service.

Exiting 2026 with a leaner driver workforce, 68% of U.S. volume processed through automated facilities, $6.5 billion in projected free cash flow, and a Digital Access Program that scaled from $139 million at inception to $4.1 billion in 2025, UPS is repositioning from volume carrier to premium logistics network built for sustained margin expansion into 2027 and beyond.

Wall Street’s Take on UPS Stock

Shedding $5 billion in low-margin Amazon volume forces a short-term revenue plateau, but it directly removes the highest-cost, lowest-yield freight from UPS’s network, setting the stage for structural EBIT margin recovery.

TIKR estimates put UPS EBIT margin at 9.6% in 2026, tightening only marginally from 9.8% in 2025 despite the Amazon exit headwind, then expanding to 10.3% by 2027 as 30,000 operational positions are eliminated, 24 additional buildings close, and the USPS absorbs Ground Saver last-mile stops.

UPS’s 9.6% 2026E EBIT margin already runs roughly 290 basis points above FedEx’s 6.7% 2026E EBIT margin, and the gap widens to 300 basis points by 2027 as UPS’s automation investment, now covering 68% of U.S. volume, compounds into structural unit cost advantage.

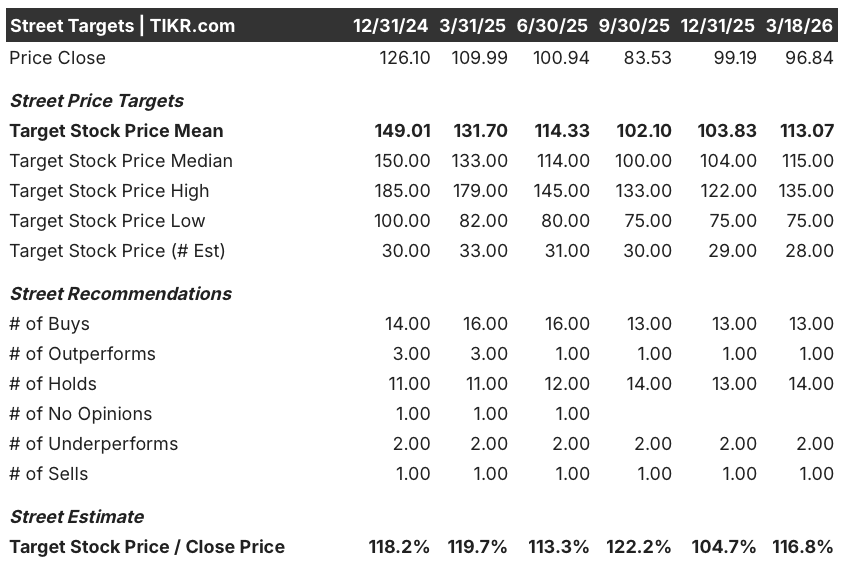

Moreover, thirteen buys, one outperform, fourteen holds, two underperforms, and one sell from 31 analysts produce a mean price target of $113.07, implying 16.8% upside from $96.84, with the consensus anchored on H2 2026 margin recovery and enterprise and SMB volume growth accelerating to mid-single digits.

The spread between the $75 bear target and the $135 bull target is wide enough to demand attention: the $75 floor prices in prolonged tariff disruption and a failed Amazon transition, while the $135 ceiling assumes H2 2026 operating margin expansion and the full $400 million to $500 million Ground Saver cost benefit arriving on schedule.

What Does the Valuation Model Say?

The TIKR mid-case target of $175.95 by December 2030, implying a 13.3% annualized return from $96.84, assumes a 4.0% revenue CAGR and a 7.7% net income margin, both grounded in CFO Brian Dykes’s guided trajectory of mid-single-digit enterprise and SMB growth and cost per piece normalizing below revenue per piece.

The market is pricing UPS at trough EBIT margin, ignoring that automated facilities already run 28% cheaper per piece than conventional ones.

The operational proof is already in the numbers: UPS closed 93 buildings in 2025 while holding its eighth straight year of industry-leading peak service, validating the TIKR model’s $175.95 mid-case target.

CEO Carol Tomé called June 2026 the inflection point, a management signal that the trough is dated and defined, not open-ended.

If the Driver Choice Program take-rate disappoints or the USPS Ground Saver transition stalls into H2 2026, the fixed-cost reduction timeline breaks and the 10.3% 2027E EBIT margin assumption collapses.

Therefore, Q1 2026 earnings will be the first test: watch U.S. Domestic operating margin against the guided mid-single-digit floor, and track Driver Choice Program acceptance numbers for confirmation the cost structure is tracking.

Should You Invest in United Parcel Service?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Parcel Service alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UPS stock on TIKR for Free →