Key Stats for Teradyne Stock

- This Week Performance: +1.6%

- 52-Week Range: $65.8 to $344.9

- Current Price: $302.4

What Happened?

Teradyne (TER), a maker of automated chip-testing equipment whose customers include Nvidia’s supply chain, crossed 60% AI-driven revenue in Q4 2025 and now guides Q1 2026 revenue to a record $1.2 billion midpoint, a 75% year-over-year jump, while the stock trades at $292 after surging 23.7% on February 3 following that guidance.

Last month, CEO Greg Smith and new CFO Michelle Turner reported Q4 revenue of $1.083 billion against a consensus estimate of $971 million, with non-GAAP earnings per share of $1.80 versus the $1.35 estimate, as AI-related demand in compute, networking, and memory drove Semiconductor Test, the company’s largest division at roughly 80% of sales, to $883 million in the quarter.

Compute, the product line serving AI accelerator and data center chip customers, grew 90% in FY 2025 and now represents roughly half of Teradyne’s SoC revenue, up from just 10% in 2023, while Teradyne holds an estimated 50% share of the custom-ASIC chip-testing market where rivals like Advantest compete for the same concentrated pool of hyperscaler customers.

Smith also stated on the Q4 2025 earnings call that “in 2026, we expect year-over-year growth across all of our businesses, with strong momentum in compute driven by AI,” a claim supported by confirmed progress toward qualifying Teradyne’s tester on a major merchant GPU customer’s production line in H1 2026, which management expects to generate initial production revenue in H2 2026.

Teradyne’s long-term target model, anchored to an ATE market it expects to reach $12 billion to $14 billion from roughly $9 billion in 2025, calls for roughly $6 billion in revenue and non-GAAP EPS of $9.50 to $11.00, roughly 2.5x 2025 levels, supported by the planned MultiLane joint venture targeting AI data center interconnect test, the Universal Robots subsidiary’s March 16 UR AI Trainer launch with Scale AI, and $785 million returned to shareholders in FY 2025 signaling financial confidence in the trajectory.

Wall Street’s Take on TER Stock

The Q1 2026 record revenue guidance of $1.2 billion midpoint, anchored by AI-driven chip testing demand already exceeding 70% of expected revenue, sets a new earnings baseline that makes FY 2026 consensus estimates look achievable rather than aggressive.

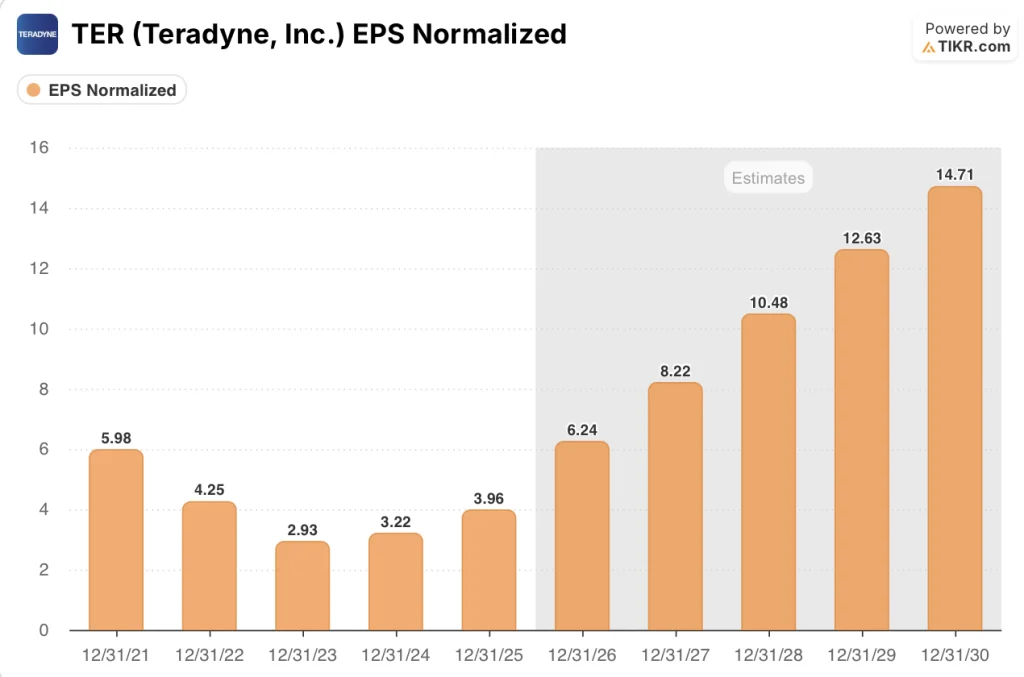

The TIKR model projects FY 2026 normalized EPS of $6.24, a 57.7% jump from the $3.96 FY 2025 actual, as AI-driven compute test demand, which already exceeded 60% of Q4 2025 revenue and is guided above 70% in Q1 2026, drives revenue 31.0% higher to $4.18 billion while operating leverage on Teradyne’s largely fixed cost base expands EBITDA margin from 26.3% to 31.4%.

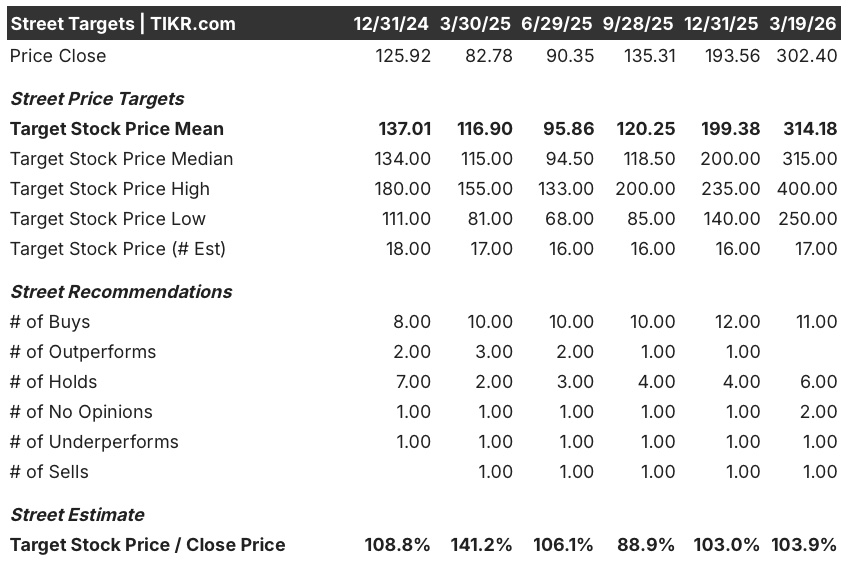

Eleven of 17 analysts covering Teradyne rate it a buy, with a mean price target of $314.18 against a current price of $302.40, implying modest near-term upside of roughly 3.9%, but that consensus was set before the company confirmed merchant GPU qualification progress in H1 2026 and a near-doubling of free cash flow to $950 million.

The gap between the Street’s low target of $250 and the high of $400 reflects exactly one binary: whether merchant GPU production revenue materializes in H2 2026 and whether the digestion period management flagged for H2 stays shallow or deepens.

What Does the Valuation Model Say?

The TIKR mid-case target of $434.39, implying a 43.6% total return through December 2030 at a 7.9% IRR, assumes 18.2% revenue CAGR and 22.0% EPS CAGR from 2025 through 2031, driven by the confirmed compute share gains, the MultiLane joint venture’s data center interconnect test revenues, and the e-commerce robotics ramp that management expects to triple in FY 2026.

Teradyne’s free cash flow is set to more than double to $950 million in FY 2026, a 110.5% jump that challenges the market’s cyclical-equipment label as a misread of the underlying business.

The MultiLane joint venture targeting AI data center interconnect test, plus confirmed HDD customer wins and compute SLT wins in 2025, give the TIKR model’s $4.18 billion FY 2026 revenue estimate concrete anchors beyond the headline GPU cycle; TIKR’s mid-case target is $434.39.

Moreover, Smith’s framing of a “4-quarter boom” from Q3 2025 through Q2 2026 is not a warning; it is a sequencing signal that the next leg, memory capacity expansion and co-packaged optics test in 2027, has not yet started.

If the merchant GPU qualification slips beyond H1 2026 or the anticipated H2 digestion proves longer than one quarter, the FY 2026 EPS estimate of $6.24 carries meaningful downside, and the current 48x forward multiple offers limited cushion.

Management confirmed GPU production revenue in H2 2026; watch the Q2 2026 earnings call for the first disclosed merchant GPU revenue figure and whether it is tracking toward a material contribution by year-end.

Should You Invest in Teradyne, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TER stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Teradyne, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TER stock on TIKR for Free →