Key Takeaways for Moody’s Stock as of July 2026

- Twelve buy ratings and four outperforms outweigh seven holds among the 20 analysts covering Moody’s, with a mean target of $540 sitting just 11% above the July 10 close of $487.

- TIKR’s mid-case model puts Moody’s at $763 by December 2030, a 57% total return from today’s price and roughly 11% annualized over four and a half years.

- Normalized EPS climbed 13% year over year to $4.33 in the quarter ended March 31, and Moody’s now guides full-year 2026 earnings to a $16.40 to $17 range.

- Moody’s reports Q2 results on July 22, with private credit revenue in the ratings business already up 80% heading into the print.

Moody’s Stock Rides a Record $2 Trillion Issuance Quarter

Moody’s (MCO) posted first-quarter 2026 revenue of $2.1 billion, up 8% year over year, following its April 22 earnings call. Adjusted diluted EPS climbed 13% to $4.33, and the company raised its full-year buyback guidance by $500 million to roughly $2.5 billion.

That capital return step followed a quarter in which rated debt issuance surpassed $2 trillion for the first time, a threshold that pulled forward record transactional revenue in Moody’s Investors Service (MIS), the ratings segment.

Private credit related revenue inside Ratings grew more than 80% year over year, as investors increasingly demand independent assessments of loans held in private credit funds.

CEO Rob Fauber tied that demand directly to artificial intelligence adoption on the e: “As AI adoption accelerates, it is driving demand for Moody’s decision-grade connected intelligence in high-stakes environments.” That framing extended past ratings, since Moody’s also expanded distribution of its research through Model Context Protocol integrations with Microsoft 365 Copilot, ChatGPT Enterprise and Claude.

Moody’s Analytics (MA), the data and software segment, grew revenue 8% as well, with recurring revenue reaching 98% of segment revenue and annual recurring revenue climbing 8% to $3.6 billion.

Moody’s reaffirmed full-year 2026 normalized EPS guidance of $16.40 to $17.00 and reports second-quarter results on July 22, a print investors will watch for confirmation that private credit and AI-driven demand held through the quarter.

Wall Street Splits Bullish on Moody’s Stock With a $540 Mean Target

Twenty analysts cover Moody’s stock, and the consensus leans bullish: 12 buy ratings and four outperforms against seven holds, with no sell or underperform ratings on the books as of July 10. The mean price target sits at $540, just 11% above the current price of $487, while the high estimate of $610 points to a much wider range of outcomes than the median of $533 suggests.

That split follows a string of insider share sales by CEO Rob Fauber and General Counsel Richard Steele under pre-set 10b5-1 trading plans, transactions that accompanied rather than followed the stock’s retreat from its 52-week high of $547.

Wall Street Expects Normalized EPS Growth to Continue for Moody’s Stock

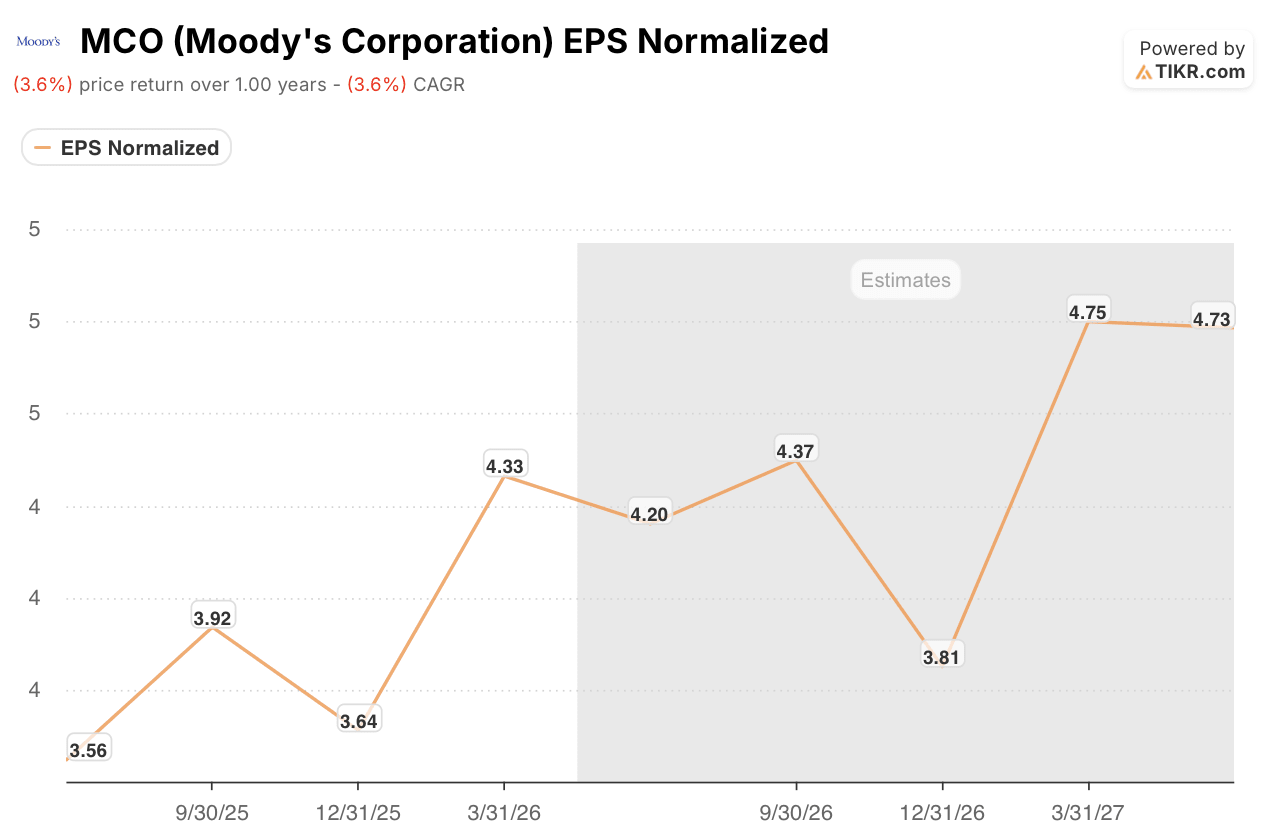

Moody’s normalized EPS reached $4.33 in the quarter ended March 31, up 13% year over year, extending double-digit annual growth in three of the last four quarters.

The Street models normalized EPS at $4.20 for the second quarter, up 18% from a year earlier, then $4.37 for the third quarter, a 12% increase.

Full-year 2026 guidance remains at $16.40 to $17 in normalized EPS, a range Moody’s reaffirmed after the first quarter, and the estimate table already shows normalized EPS reaching $4.75 by the first quarter of 2027, a 10% increase from a year earlier.

Whether AI-driven demand across ratings and analytics can keep normalized EPS growth in double digits through 2027, once the easier comparisons from private credit’s 80% surge fade, is the question the Street has not yet answered.

TIKR Values Moody’s Stock at $763, Pricing In Sustained EPS Growth

TIKR’s mid-case model values Moody’s at $763 by December 2030, a 57% total return from the current price of $487, or roughly 11% annualized over four and a half years.

That annualized return sits well above the mean Wall Street target’s one-year gain, positioning Moody’s stock for a re-rating that extends far past the next 12 months.

The target is reachable because normalized EPS is already compounding in double digits and buybacks are set to hit $2.5 billion this year. AI-driven demand across ratings and analytics keeps expanding the earnings base that return compounds from.

Should You Invest in Moody’s Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Moody’s Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Moody’s Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MCO stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!