Key Stats for Circle Stock

- Friday’s Performance: 5%

- 52-Week Range: $50 to $263

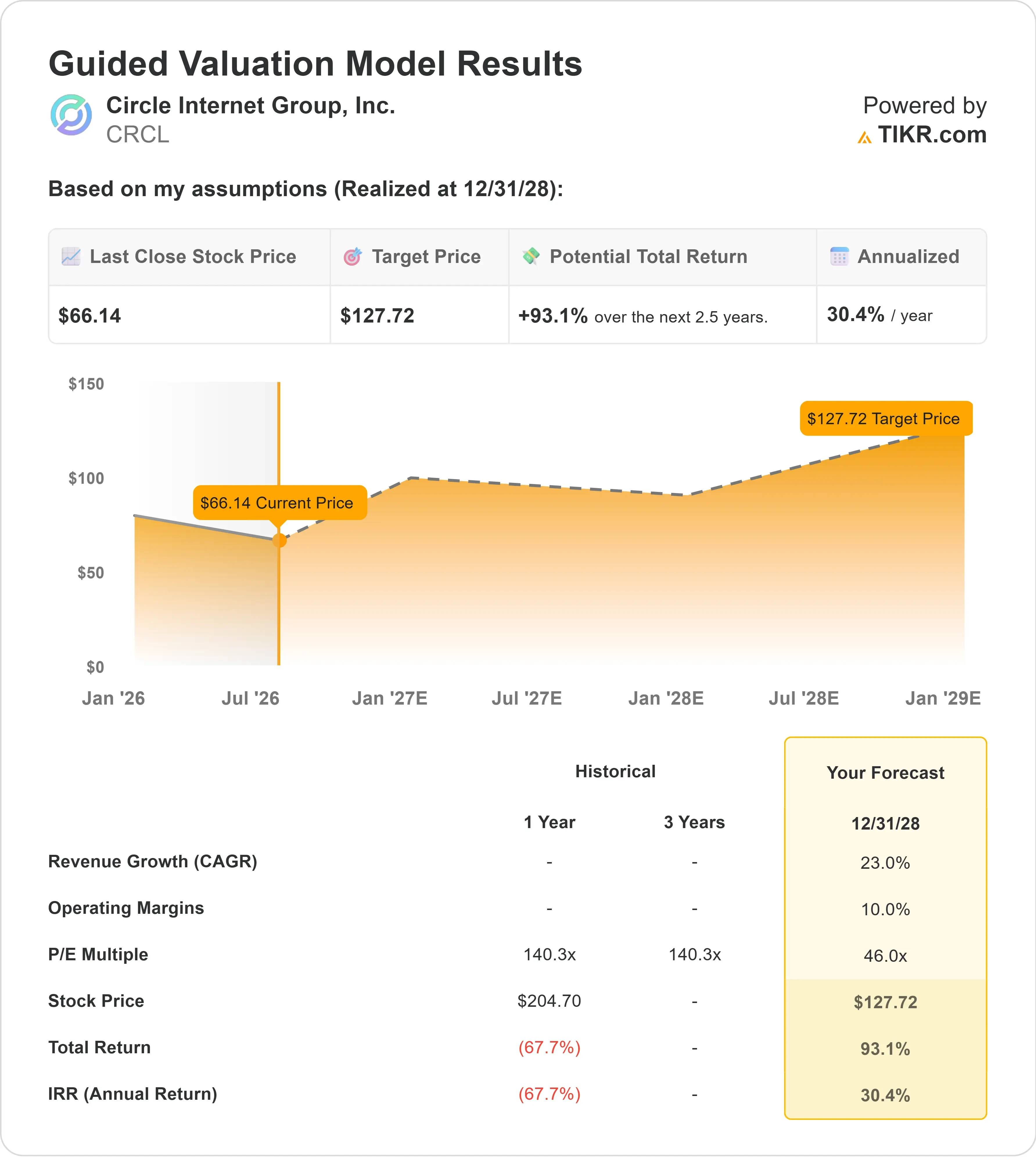

- Valuation Model Target Price: Around $128

- Implied Upside: 93%

Analyze your favorite stocks like Circle Internet Group with TIKR (It’s free) >>>

What Happened?

Circle’s investment story centers on whether USDC can evolve from a cryptocurrency trading tool into core infrastructure for regulated payments and financial markets. That case gained credibility Friday, pushing Circle Internet Group stock up about 5% to $66 after the company cleared a major regulatory hurdle. Shares jumped 10% in premarket trading before giving back part of the advance, showing that investors welcomed the news while remaining cautious about how quickly it will improve earnings.

The stock rose specifically because the Office of the Comptroller of the Currency granted final approval for Circle National Trust, placing the new entity under direct federal supervision. Upon opening, the trust bank will provide digital-asset custody for Circle and its affiliates, with potential expansion to a limited number of banks and other institutional customers. It cannot accept traditional deposits or make loans, but federal oversight could make financial institutions more comfortable using Circle’s infrastructure, while management of the reserves backing USDC remains a planned future capability.

Recent management commentary added to the longer-term growth story. At Bernstein’s Strategic Decisions Conference, CEO Jeremy Allaire said USDC’s monetary base was approaching $80 billion, with nearly $15 trillion in on-chain transaction volume, and described stablecoins as a “winner take most market structure.” He also highlighted Cash App’s USDC integration and said Circle plans to generate future revenue from Arc, its blockchain network for financial applications, and Circle Payments Network, which connects institutions for cross-border settlement.

Competition and analyst disagreement remain central to the investment case. Tether’s USDT had around $183 billion of token-related liabilities at the end of the first quarter, more than twice Circle’s $77 billion of USDC in circulation, but USDC still represented 63% of stablecoin transaction volume during the quarter. Clear Street maintained a Buy rating and a $157 target after the bank approval, while Wolfe Research retained an Underperform rating and a $65 target; ARK Invest also bought 217,896 Circle shares worth about $14 million one day before the announcement. Those contrasting signals capture the core debate around CRCL: whether Circle’s regulatory position and high transaction usage can overcome Tether’s greater scale and turn USDC adoption into durable profits.

Value Circle Internet Group instantly (Free with TIKR) >>>

Could Circle Internet Group Be Undervalued?

Under the valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 23%

- Operating Margins: around 10%

- Exit P/E Multiple: around 46x

The 23% revenue-growth assumption is close to TIKR’s forward two-year consensus estimate of around 22%. Reaching that pace depends largely on continued growth in USDC circulation because Circle generates most of its revenue from income earned on the cash and short-term government securities backing the stablecoin.

Circle’s latest reported results support the adoption story but also show why network growth does not translate directly into equal profit growth. USDC circulation ended the first quarter at $77.0 billion, up 28%, while on-chain transaction volume increased 263% to $21.5 trillion. Total revenue and reserve income rose 20% to $694 million, adjusted EBITDA increased 24% to $151 million, and net income declined 15% to $55 million as higher compensation and continued investment offset part of the revenue growth.

See analysts’ growth forecasts and price targets for Circle Internet Group (It’s free) >>>

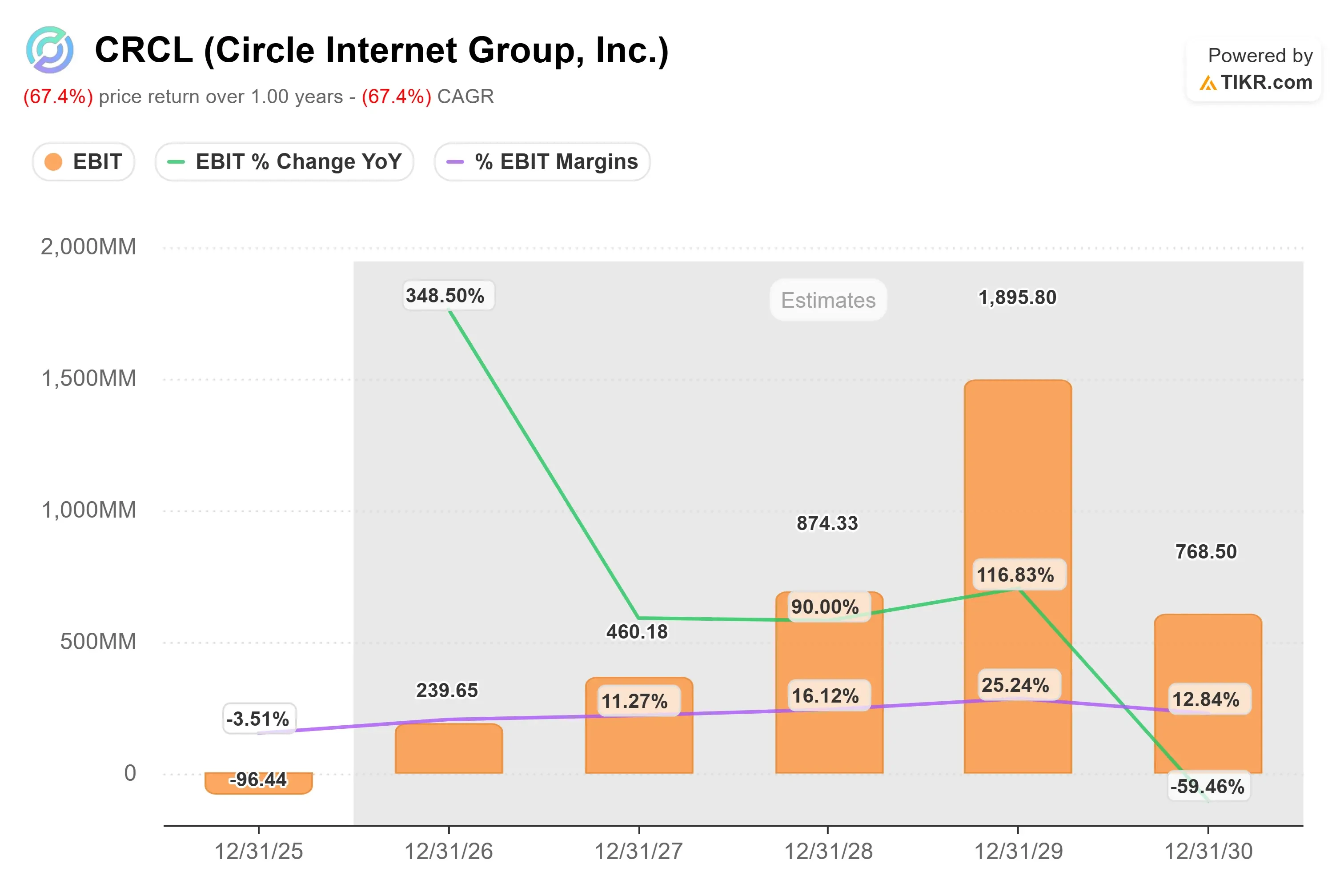

TIKR’s EBIT chart shows Circle moving from an EBIT loss of about $96 million and a negative 4% margin in 2025 to positive EBIT of around $240 million in 2026. Consensus estimates then point to EBIT margins of around 11% in 2027 and 16% in 2028, making the model’s 10% operating-margin assumption look relatively conservative. Still, that improvement depends on Circle retaining more of the economics generated by USDC because distribution and transaction costs rise alongside circulation. Arc, Circle Payments Network, custody, and cross-border settlement therefore need to generate enough fee revenue to support durable margin expansion.

The 46x exit P/E multiple is the model’s most demanding assumption because it requires Circle to retain a premium valuation through the end of 2028. That becomes more defensible if Circle protects USDC’s transaction leadership while building recurring revenue beyond interest-sensitive reserve income. It becomes harder to support if Tether, Stripe-owned Bridge, or other stablecoin issuers weaken Circle’s distribution advantage or force the company to share more economics with partners.

Based on these assumptions, TIKR’s model estimates Circle stock could reach around $128 by the end of 2028, implying about 93% total upside over 2.5 years. This represents an optimistic scenario rather than a conservative fair-value estimate because it depends on revenue growing around 23%, operating margins reaching 10%, and investors still awarding Circle a 46x earnings multiple.

USDC circulation remains the clearest growth driver because a larger stablecoin base increases reserve assets and expands Circle’s opportunity in payments and custody. Federal supervision through Circle National Trust could accelerate adoption among institutions that require regulated infrastructure. Arc and Circle Payments Network could diversify revenue through transaction fees and cross-border settlement rather than leaving Circle primarily dependent on reserve income. Margin expansion depends on those products growing faster than partner payments, compliance costs, and infrastructure investment.

At around $66, CRCL could offer meaningful upside, but stronger performance in 2026 requires evidence that regulatory progress and rising USDC usage are producing more diversified and durable profits.

How Much Upside Does Circle Stock Have From Here?

Investors can estimate Circle Internet Group’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Circle Internet Group in under 60 seconds with TIKR (It’s free) >>>