Key Takeaways for American Airlines Group Inc. Stock as of July 2026

- Ten buys, two outperforms, twelve holds: Wall Street’s mean target sits at $19 for American Airlines stock, 14% above the July 10 close of $17.

- TIKR’s mid-case model puts a $53 target on American Airlines Group by December 2030, a 211% total return worth 29% annualized over the next 4.5 years.

- Trading at $17, American Airlines stock prices in little of the EBITDA inflection ahead: margin is expected to climb from 5% in the March quarter to 15% by June 2027, a gap that reads undervalued against the Street’s own numbers.

- Following the Federal Aviation Administration’s (FAA) July 10 decision to extend Chicago O’Hare flight cuts through October 2027, American Airlines locked in capacity discipline at its second-largest hub, a structural tailwind for the pricing power behind that margin recovery.

American Airlines Stock Gains Capacity Discipline as FAA Extends O’Hare Flight Cuts

American Airlines Group (AAL) just gained an unusual ally in its push to protect pricing power: the federal government. On July 10, 2026, the FAA extended flight restrictions at Chicago O’Hare through October 2027, capping the airport at 2,708 daily arrivals and departures instead of the 3,080 operations American and United had planned for this summer, a 12% cut to scheduled capacity at one of American’s largest hubs.

That decision followed a rough stretch of on-time performance. Only 56% of O’Hare departures and 58% of arrivals ran on schedule last summer as construction and overscheduling collided, and the FAA said it would rather hold operations near last year’s levels than risk a repeat. American called the move “a prudent decision that will help maintain operational stability, improve reliability, reduce delays, and support a more predictable travel experience.”

The capacity discipline lands as American works to prove its pricing gains can outlast the fuel shock that hit results earlier this year. On the company’s Q1 earnings call, CEO Robert Isom pointed to the demand strength behind the numbers: “We recorded the 9 highest revenue intake weeks in our history… First quarter revenue grew 10.8%, and we expect this demand strength to continue as we anticipate the second quarter will deliver revenue growth of approximately 15%.”

That growth came even after a $320 million revenue hit from winter storms and a $400 million jump in fuel costs versus the forward curve. EBITDA still rose to $740 million in the quarter, up 32% year over year, though margin held at just 5% as the fuel spike ate into the recovery CFO Devon May had planned for. May told investors the airline had already built 40% to 50% fuel-cost recapture into its second-quarter plan, with that rate expected to climb toward 90% by year end.

Wall Street took notice before the O’Hare news broke. Wells Fargo raised its American Airlines stock price target to $17 from $12 on June 30, 2026, citing easing fuel costs and industry capacity rationalization tied in part to Spirit Airlines’ liquidation. Locking in reduced Chicago flying only reinforces that same capacity story heading into American’s July 23 second-quarter report.

Wall Street Turns More Bullish on American Airlines Stock After Fuel Shock

Twenty-six analysts cover American Airlines stock as of July 10, 2026, split between 10 buy ratings, 2 outperforms, 12 holds and 2 sells. The mean target price sits at $19, roughly 14% above the current $17 share price, built on a high estimate of $25 and a low of $10 across 24 price targets.

That mean target has climbed from $13 a year ago, tracking Wells Fargo’s June 30 move to raise its own target to $17 from $12 on easing fuel costs and tighter industry capacity.

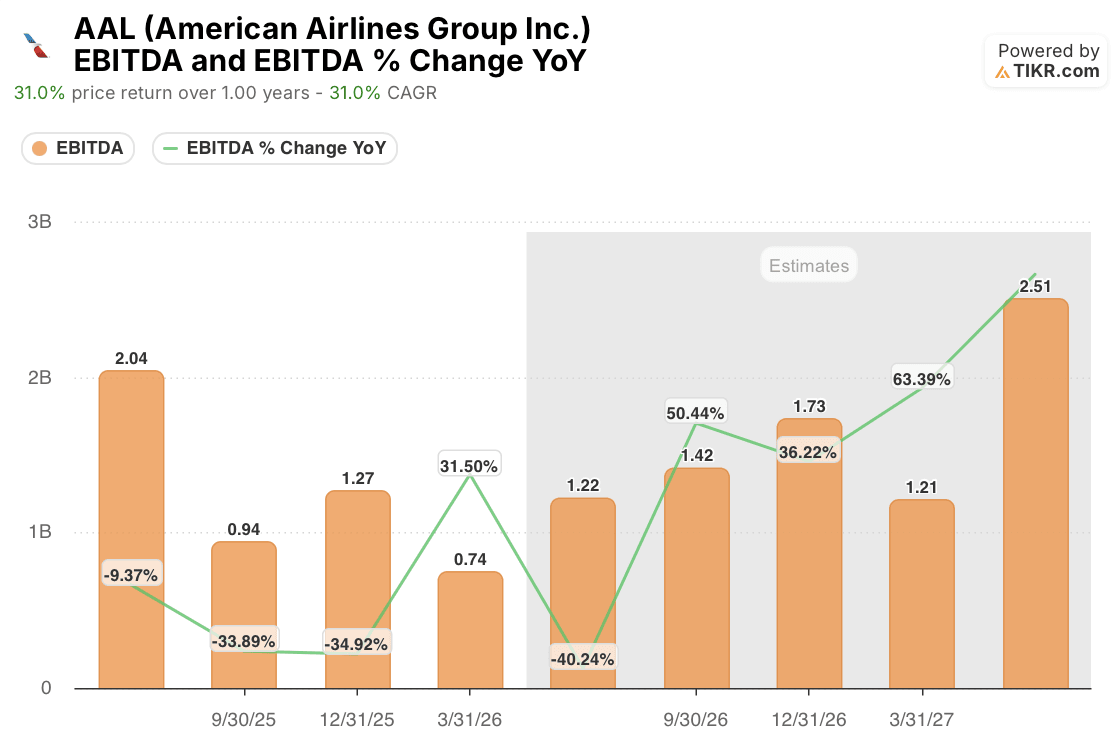

Wall Street Expects American Airlines Stock’s EBITDA to Double Within a Year

American Airlines stock’s EBITDA reached $740 million in the quarter ended March 31, 2026, up 32% year over year, though margin held at just 5% as fuel costs outran the recovery already underway. Wall Street expects EBITDA to rise to $1.22 billion in the June quarter, down 40% against last year’s unusually strong comparison, before margin climbs back to 7%.

That year-over-year comparison flips by September, with EBITDA projected to grow 50% to $1.42 billion, then 36% to $1.73 billion by year end, pushing margin to 9% and 11% respectively.

The estimates keep accelerating into 2027, with EBITDA projected to grow 105% year over year to $2.51 billion by June, tripling margin to 15% from where it sits today. Whether American can sustain that climb hinges on one open question: can fuel-cost recapture keep pace as capacity discipline tightens across the industry into the back half of 2026?

TIKR’s $53 Target on American Airlines Stock Holds if the EBITDA Inflection Lands

TIKR’s mid-case model values American Airlines Group at $53 by December 2030, a 211% total return from the current price of $17, worth 29% annualized over the next 4.5 years.

A return of that size would place American Airlines stock well ahead of the muted, single-digit annualized gains investors typically expect from a mature, capital-intensive airline.

That target is reachable if the EBITDA path plays out as guided. Margin recovery from the DFW and Philadelphia rebanking, tighter capacity following the O’Hare cap extension, and continued fuel-cost recapture all point the same direction.

American Airlines’ own guidance for 40% to 50% recapture in the second quarter, rising toward 90% by year end, lines up with the margin expansion baked into TIKR’s model.

Should You Invest in American Airlines Group Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up American Airlines Group Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track American Airlines Group Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AAL stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!