Key Stats for Lululemon Stock

- Friday’s Price Change: -20%

- Current Share Price: $265

- 52-Week High: $423

- LULU Stock Price Target: $323

What Happened?

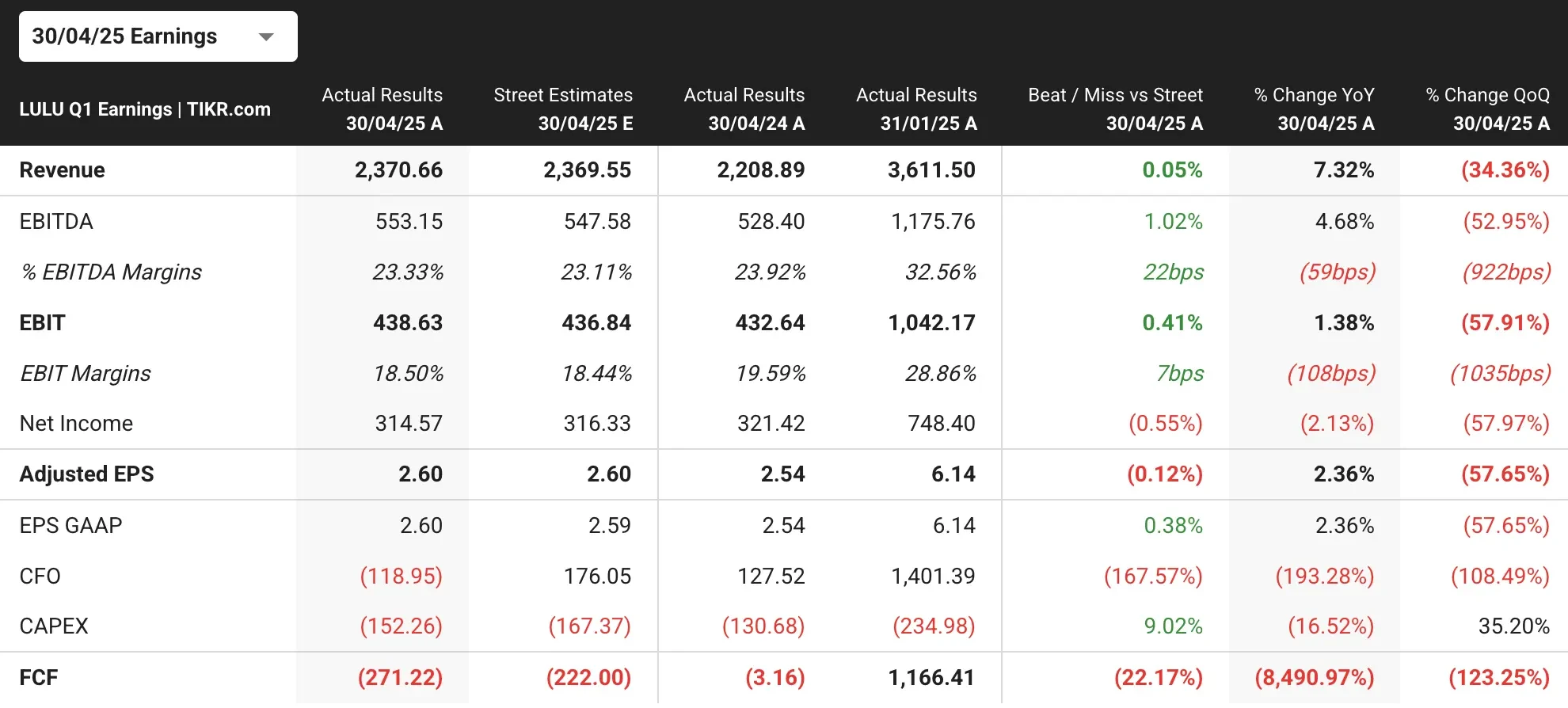

Lululemon (LULU) stock plummeted nearly 20% on Friday, marking one of the worst single-day declines in the company’s history. The athleisure retailer reported mixed first-quarter results and slashed its full-year earnings guidance due to tariff pressures and slowing U.S. growth.

Lululemon reported adjusted earnings per share of $2.60, in line with estimates. Comparatively, revenue stood at $2.37 billion, slightly above consensus estimates of $2.36 billion.

However, the company cut its full-year earnings guidance to a range of $14.58 to $14.78 per share, down from the previous forecast of $14.95 to $15.15 per share.

The guidance reduction was primarily attributed to the impact of tariffs, which the retailer expects will reduce full-year gross margins by approximately 110 basis points, compared to 2024, significantly worse than the previously anticipated 60-basis-point decline.

Management also cited challenging conditions in the U.S. market, where revenue grew only 2% and comparable sales decreased 2%, reflecting cautious consumer spending patterns.

CFO Meghan Frank indicated that Lululemon plans to implement strategic price increases on a small portion of its product assortment to help offset the impacts of tariffs. These price hikes will roll out in the second half of the current quarter and into Q3.

See Lululemon’s full analyst estimates, earnings results, and earnings transcript (It’s free) >>>

What the Market Is Telling Us About LULU Stock

The massive selloff in LULU stock reflects investors’ concern about Lululemon’s ability to maintain its premium pricing power and growth trajectory in a challenging retail environment.

The company’s exposure to tariffs is significant, with management assuming 30% incremental tariffs on China and 10% on other sourcing countries. These tariffs will impact Lululemon’s supply chain, which spans Vietnam (40%), Cambodia (17%), and several other Asian countries.

The weak U.S. performance is troubling for investors, as domestic growth has been a key driver of Lululemon’s success.

CEO Calvin McDonald’s admission that he is not happy with U.S. growth trends and his observation that consumers are being more cautious with purchases signal a potential shift in the brand’s core market dynamics.

Despite maintaining its full-year revenue guidance of $11.15 billion to $11.3 billion, the compression in expected profitability suggests LULU is facing margin pressure from multiple fronts.

The disconnect between revenue growth expectations and earnings projections suggests that Lululemon may need to compromise profitability to maintain its market share and growth momentum.

With operating margins expected to decline 160 basis points year-over-year, investors are questioning whether the premium athletic apparel market can sustain the growth rates and profitability levels that have historically justified a valuation premium for LULU stock.

Find the best stocks to buy today that are even better than LULU. (It’s free) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!