Key Takeaways:

- The 2-Minute Valuation Model values Thermo Fisher stock at $490 per share in 2 years, but analysts have a price target of $570 per share.

- That means analysts see 38% upside for the stock from today’s price of $414 per share.

- Thermo Fisher is projected to grow EPS by 27% over the next 3 years as growth accelerates.

- The stock trades below its historical valuation despite strong fundamentals and improving growth.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Thermo Fisher Scientific (TMO) stands as the world’s leading life sciences and laboratory equipment provider, serving pharmaceutical, biotechnology, academic, government, and industrial customers globally.

Thermo Fisher enables scientific discovery and innovation in healthcare, environmental science, and industrial applications with a comprehensive portfolio that includes analytical instruments, reagents, consumables, software, and services.

With TMO stock now trading at $414 per share, investors are questioning whether this life sciences giant represents a compelling value opportunity after recent price weakness.

Despite the company’s premium business quality and strong competitive position, the stock trades at a substantial discount to its historical valuation multiples.

Let’s analyze whether this valuation gap creates an attractive entry point for long-term investors.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings-per-share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why Thermo Fisher Stock Looks Undervalued

Forecast

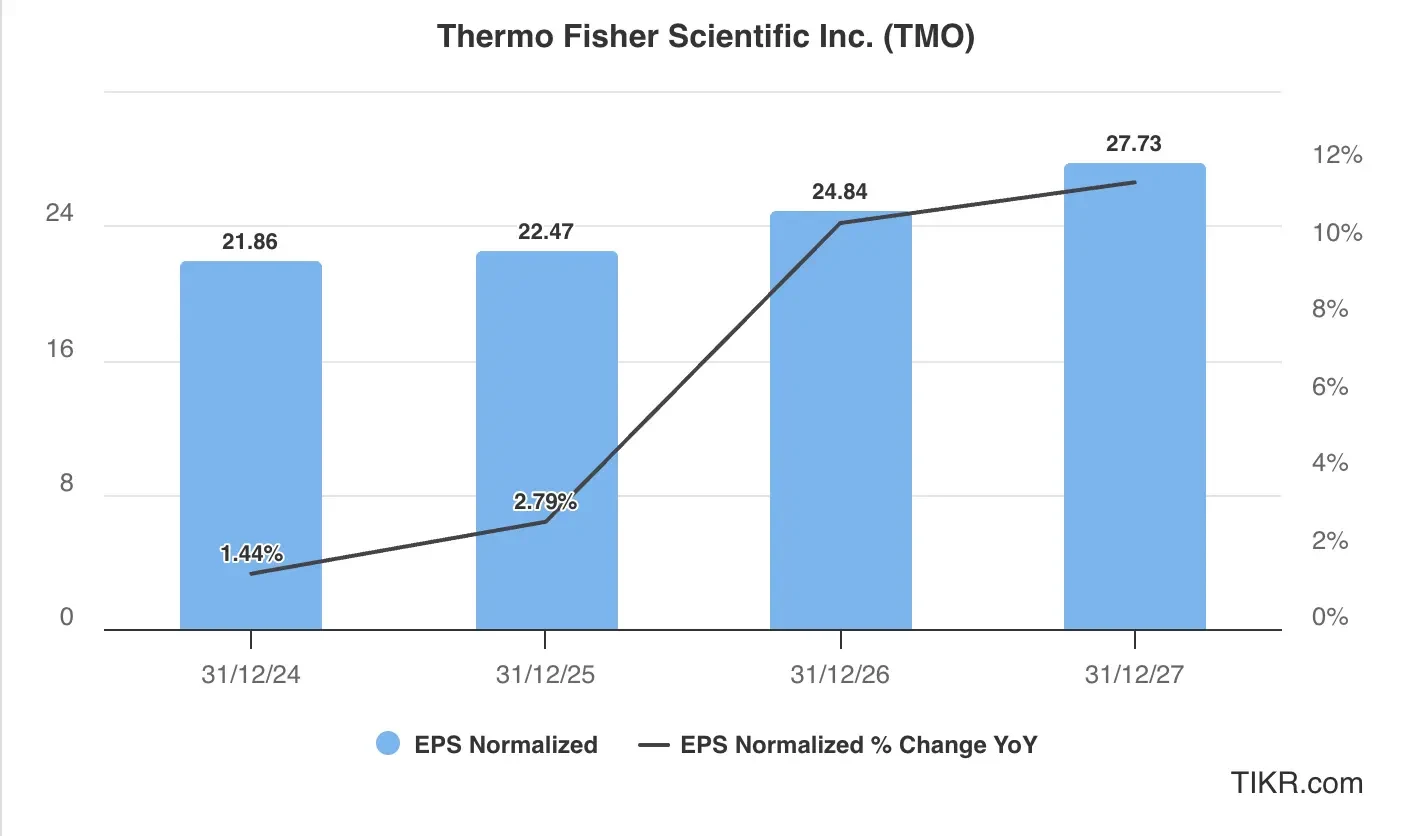

Based on analyst estimates in the EPS chart below, Thermo Fisher is expected to achieve double-digit annual earnings-per-share growth over the next two years.

EPS is projected to grow from $21.86 in 2024 to $27.73 by 2027. This represents a 27% total increase, with growth rates substantially improving after a period of normalization in 2024-2025.

This earnings growth for Thermo Fisher stock is likely to be driven by:

- Biopharma and pharmaceutical recovery: After customer inventory destocking and reduced capital spending, pharmaceutical and biotechnology customers are expected to resume normalized spending patterns.

- Precision medicine expansion: Thermo Fisher’s instruments and reagents are essential for the growing precision medicine market, enabling targeted therapeutic approaches based on genetic and molecular profiles.

- Operational efficiency initiatives: The company continues implementing its PPI (Practical Process Improvement) Business System to drive margin expansion across the organization.

- Strategic M&A: Thermo Fisher has a proven track record of value-creating acquisitions that enhance its technology portfolio and market positioning.

- China recovery: After weakness in the Chinese market, improving conditions in this important growth region should accelerate performance.

For our valuation, we’ll estimate that TMO stock will reach $27 in EPS in 2027.

Check out Thermo Fisher’s full analyst estimates (It’s free) >>>

Valuation Multiple

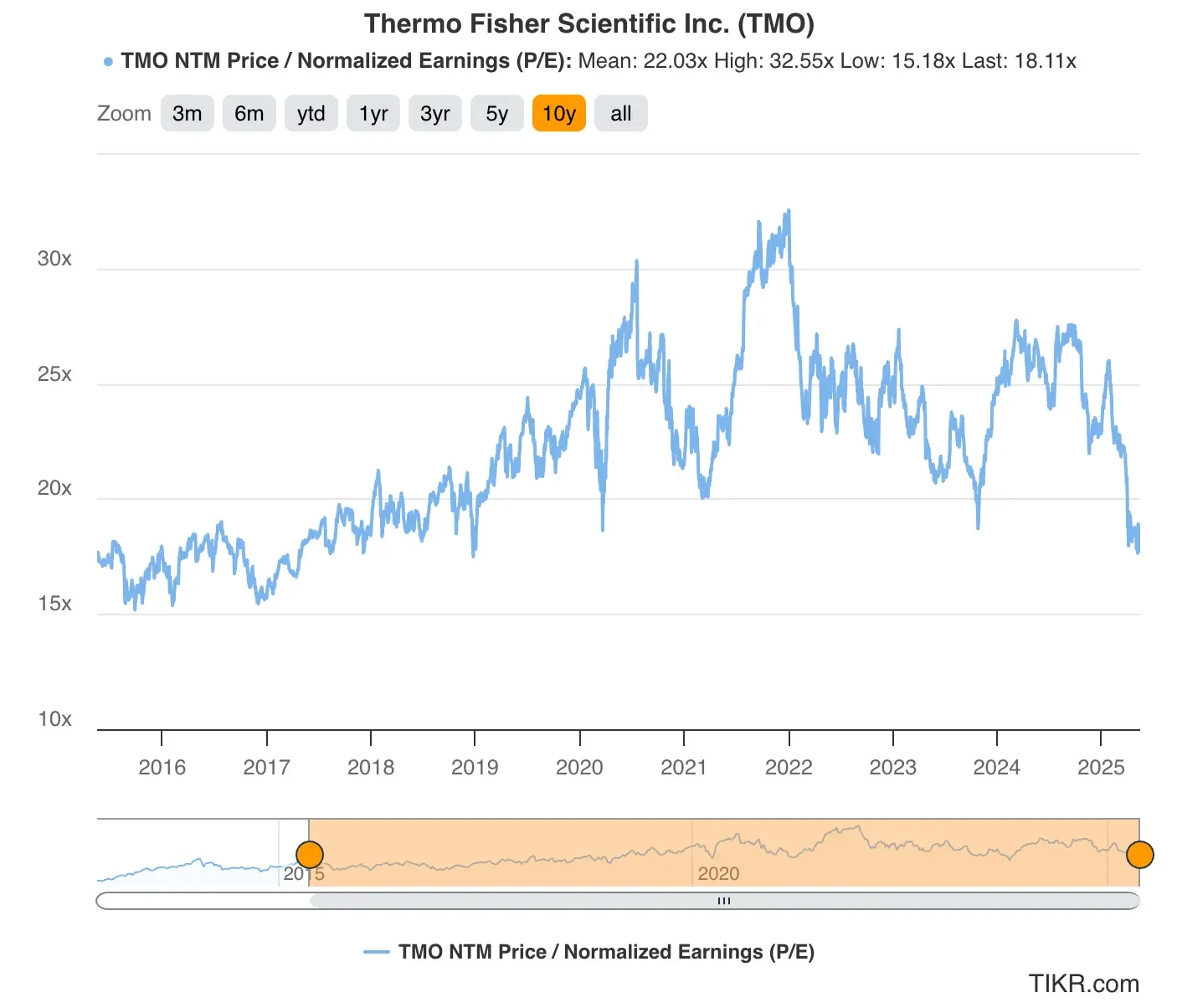

Thermo Fisher stock trades today at around 18x forward earnings, which is below its 10-year historical average P/E of 22x, as shown in the valuation chart.

This represents one of the lower valuations in the company’s recent trading history, creating a value opportunity in a premium quality business.

For our valuation, we’ll use a conservative forward P/E multiple of 18x. This is below the historical average, but still acknowledges the company’s improved growth profile.

High-quality companies often trade at a P/E multiple that’s about 2x their annual earnings growth. If earnings growth rebounds to over 10% annually by 2026, it’s reasonable to think the stock could return to its historical average P/E of 22x, rather than the 18x multiple we’ll use in our valuation.

Fair Value of TMO Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $27

- Conservative forward P/E multiple: 18x

- Expected dividends over the next 2 years: $5

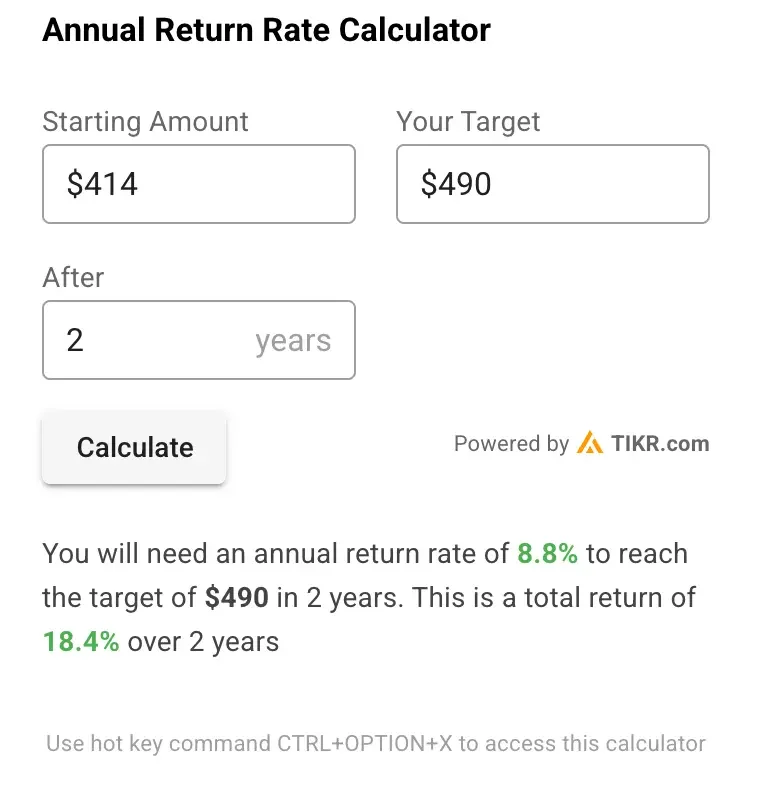

Expected Normalized EPS ($27) * Forward P/E ratio (18x) + Expected Dividends ($5) = Expected Share Price ($490)

The 2-year expected TMO stock price we would get from this valuation is $490 per share.

With Thermo Fisher stock currently trading at around $414 per share, this implies a potential upside of 18% over the next two years or a 9% annualized return.

A 9% annual return might not sound exciting, but the stock could potentially deliver higher returns.

If we used a 22x P/E multiple instead of an 18x multiple in our valuation, the stock would be valued at $599/share, indicating a potential 45% upside today.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

What is Analysts’ Price Target for Thermo Fisher Stock?

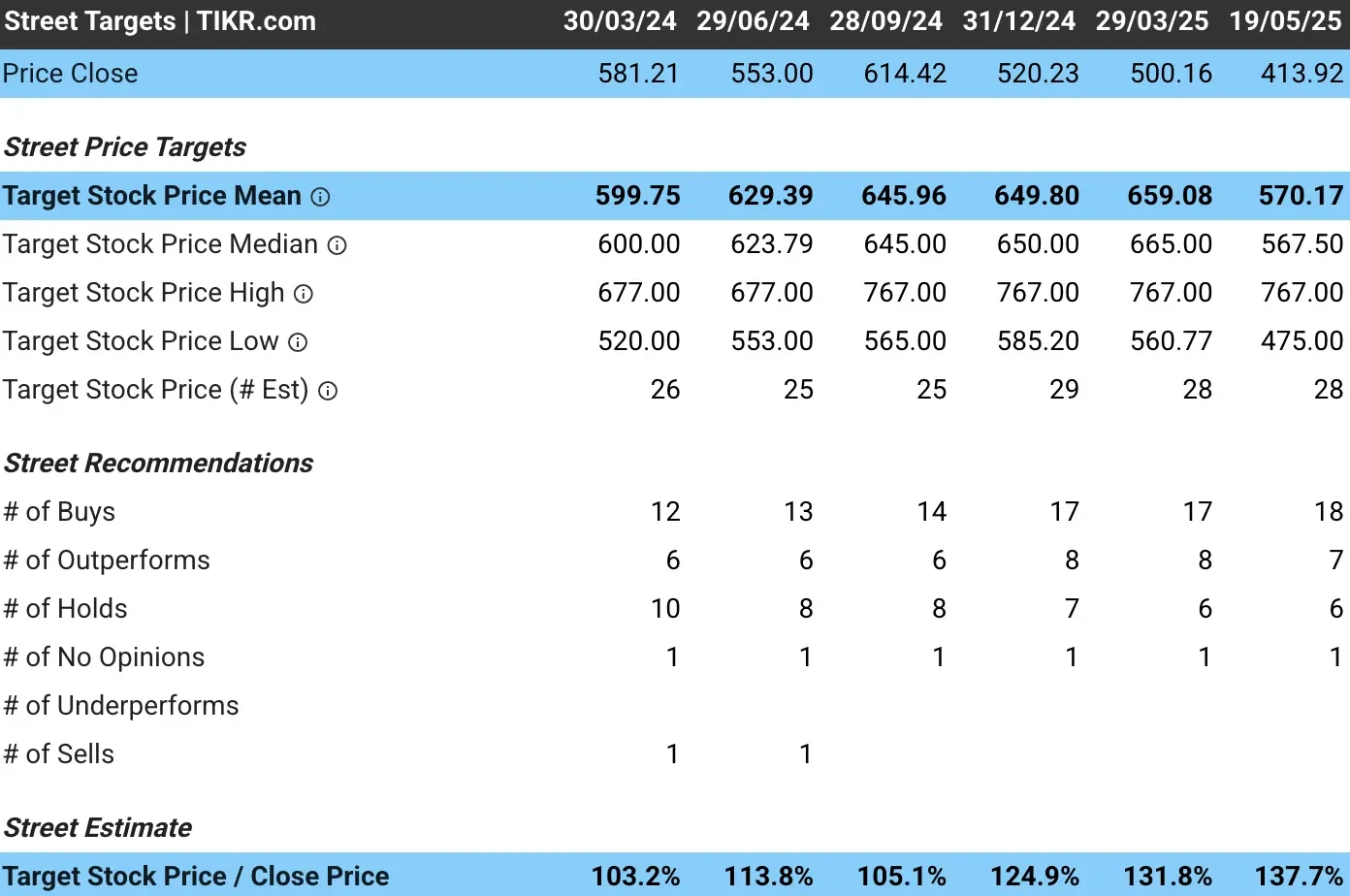

Analysts think that Thermo Fisher stock is significantly undervalued today.

Analysts have an average price target of around $570 per share for TMO stock, indicating they see about 38% upside today for Thermo Fisher based on its current share price:

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact the healthcare giant’s growth trajectory:

- Persistent biopharma weakness: Prolonged reduction in pharmaceutical and biotechnology customer spending could delay the expected growth acceleration.

- Competitive pressure: Intensifying competition in key product categories could pressure margins and market share.

- Integration challenges: While Thermo Fisher has a strong M&A track record, integration risks always exist with future acquisitions.

- Currency headwinds: As a global company, significant strengthening of the U.S. dollar could impact reported results.

- Regulatory environment: Changes in healthcare regulations or research funding priorities could affect customer demand patterns.

TIKR Takeaway

At its current valuation, Thermo Fisher presents an attractive value proposition for patient, quality-focused investors.

The company combines substantial competitive advantages, technological leadership, and consistent execution with a valuation below historical averages despite improving growth prospects.

The stock’s appeal lies in its combination of defensive characteristics, serving essential research and healthcare markets with high switching costs, and exposure to secular growth trends in life sciences, diagnostics, and precision medicine.

Thermo Fisher’s diversified business model and strong balance sheet provide downside protection while the company navigates the current environment.

While the projected 18% return over two years is not exceptional in absolute terms, it offers an attractive risk-reward profile for such a high-quality business.

For investors seeking exposure to the life sciences sector with a margin of safety, Thermo Fisher at current levels provides an opportunity to purchase a premium franchise at a discount valuation.

As growth accelerates in 2026-2027 and investor sentiment improves, the stock could see additional upside beyond our base case through multiple expansion toward its historical average.

Is TMO stock a buy for contrarian value investors? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!