JB Hi-Fi Limited (JBH) operates one of Australia and New Zealand’s largest consumer electronics retail platforms through JB Hi-Fi Australia, JB Hi-Fi New Zealand, The Good Guys, and the premium e&s brand. The group sells technology, appliances, and home products via a dense store network complemented by strong online, commercial, and omnichannel capabilities. Scale, supplier relationships, and a low-cost operating model underpin its value proposition.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The stock has been range-bound over the past year as investors weighed resilient execution against softer discretionary demand and margin pressure from promotions. Shares have pulled back from mid-year highs, reflecting caution about category normalization following prior cycles, even as the company continues to return capital through dividends.

Heading into FY26, the setup is defined by balance. The valuation appears reasonable relative to history, the balance sheet remains net cash, and management is prioritizing inventory discipline and cost control. The mid-case framework assumes modest top-line growth, stable margins, and continued cash returns rather than multiple expansion.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

FY25 results showed steady progress, with total sales rising about 10% to roughly A$10.6 billion, driven by growth across JB Hi-Fi Australia, New Zealand, and The Good Guys, with the e&s acquisition contributing incrementally. EBIT increased in the high-single digits to about A$694 million, while NPAT grew mid-single digits to roughly A$462 million, reflecting disciplined cost management amid competitive pricing.

| Metric | Value |

|---|---|

| Revenue Growth (1Y CAGR) | ~10% |

| Revenue Growth (5Y CAGR) | ~6% |

| Net Income Margin | ~4–5% |

| EPS Growth (5Y CAGR) | ~8% |

| Free Cash Flow Conversion | Strong, consistently positive |

| Current Share Price | ~A$96.6 |

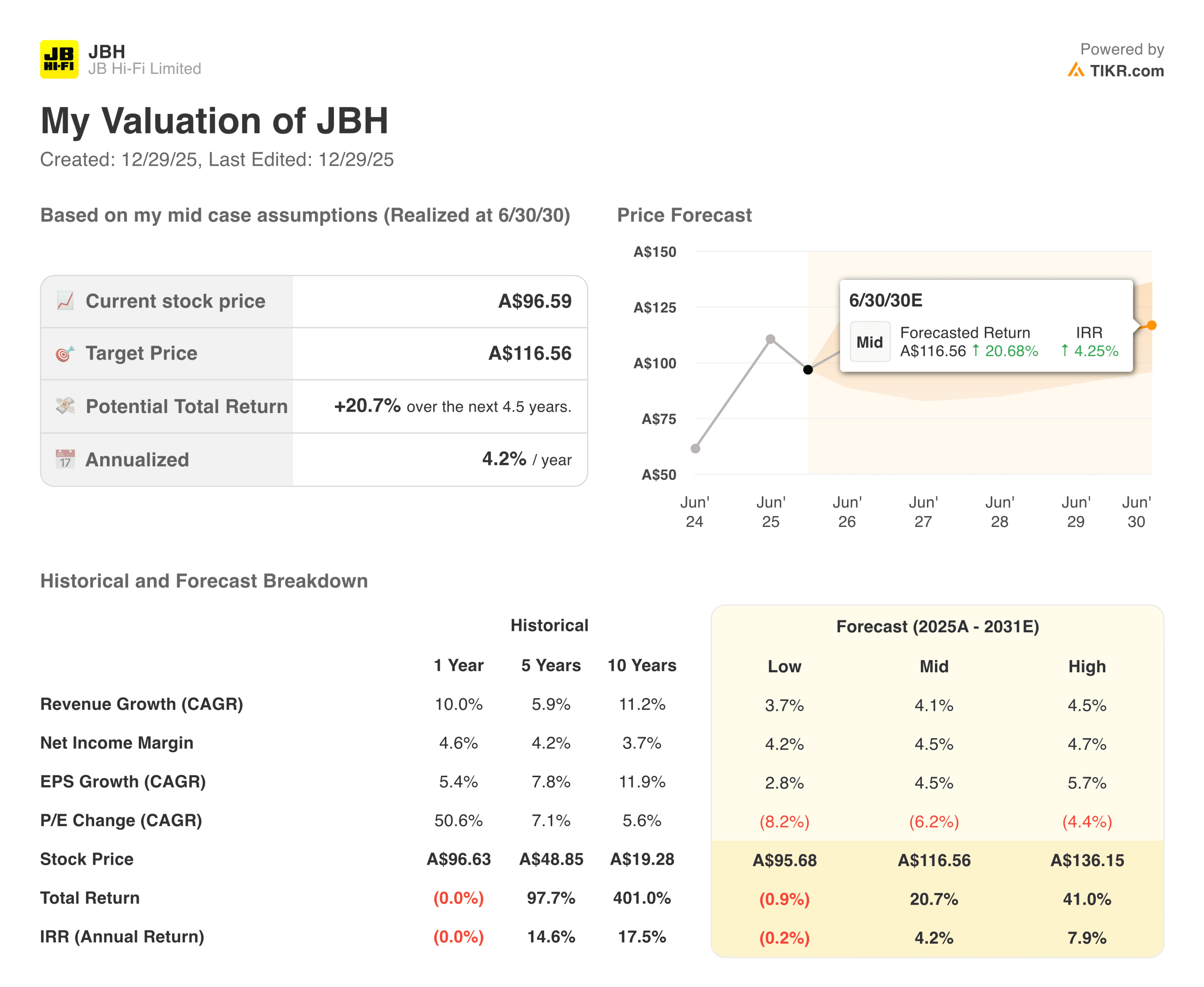

| Mid-Case Target Price (2030E) | ~A$116.6 |

| Total Upside (Mid-Case) | ~20.7% |

| Annualized Return (Mid-Case) | ~4.2% |

Margins were also broadly stable, with gross margin compressing modestly due to mix and promotions, but cost of doing business improved relative to sales, helping to protect EBIT margin near the mid-6% range. Earnings per share increased by approximately 5%, driven by operating leverage and controlled expenses.

Cash generation remained a core strength. Operating cash flow exceeded A$700 million, free cash flow stayed strong after capex, and the group finished the year with a net cash position. The board lifted shareholder returns with a higher dividend payout range and a special dividend, signaling confidence in ongoing cash flows.

Look up JB Hi-Fi’s full financial results & estimates (It’s free)>>>

Broader Market Context

Consumer electronics retail remains competitive as households remain price-sensitive and discretionary budgets stay tight. Promotions and product cycles drive traffic, while retailers with scale and supplier access tend to fare better during demand normalization. Interest rates and cost-of-living pressures continue to shape purchasing behavior.

For JB Hi-Fi, these dynamics favor execution over expansion. The company’s scale, omnichannel reach, and inventory control help mitigate volatility, but sustained margin expansion is unlikely without a demand inflection. The near-term outlook depends more on cost discipline and mix than on aggressive sales growth.

1. Scale and Cost Discipline

JB Hi-Fi’s scale remains a clear competitive advantage in the Australian electronics retail market. High sales density, centralized procurement, and long-standing supplier relationships enable the group to price aggressively while maintaining profitability. This advantage is significant in softer-demand environments, when smaller competitors struggle to maintain margins without sacrificing volume.

Cost discipline continues to set JB Hi-Fi apart from its peers, as the company has kept store labor, rent leverage, and overhead growth tightly controlled, even as it invests selectively in systems and customer experience. That operating discipline gives management room to absorb promotional pressure without materially damaging earnings. Over time, this consistency has helped JB Hi-Fi remain profitable across multiple retail cycles.

2. Inventory and Working Capital

Inventory management remains a core operational focus. While inventory levels increased during FY25 to support new stores, acquisitions, and peak trading periods, turnover metrics stayed healthy relative to historical norms. Management emphasized tighter demand forecasting and faster replenishment cycles to reduce the risk of excess stock and margin-eroding markdowns.

Working capital discipline supports strong cash generation. Payables growth tracked inventory increases, limiting balance sheet strain and keeping net working capital stable. This control is critical in an environment where inventory errors can quickly become cash-flow problems. JB Hi-Fi’s ability to scale inventory without stressing liquidity reinforces the resilience of its operating model.

Value stocks like JB Hi-Fi in less than 60 seconds with TIKR (It’s free) >>>

3. Capital Returns and Strategy

Capital returns remain central to the JB Hi-Fi investment case. The board increased the dividend payout range to 70–80% of NPAT and declared a special dividend in FY25, signaling confidence in recurring cash flows. With a net cash balance sheet, the company retains the flexibility to reward shareholders without relying on leverage.

Strategically, management continues to favor disciplined execution over aggressive expansion. Store rollouts are targeted, digital investments are incremental, and acquisitions are approached cautiously. This measured approach reflects a mature retail cycle and prioritizes return on invested capital over headline growth. For long-term investors, that restraint reduces risk while supporting consistent shareholder returns.

The TIKR Takeaway

JB Hi-Fi screens as a steady compounder rather than a high-growth story. Using a mid-case framework that assumes modest revenue growth, stable margins, and continued cash returns, the stock offers around 21% total upside by 2030, driven primarily by earnings and dividends rather than valuation re-rating.

Should You Buy, Sell, or Hold JB Hi-Fi Stock in 2025?

Investors may focus on margin stability, inventory discipline, and capital returns as the key variables. The story hinges on execution in a competitive retail environment, with downside protection from cash flow and balance sheet strength, and upside tied to steady earnings growth rather than multiple expansion.

How Much Upside Does JB Hi-Fi Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!