Key Takeaways:

- The 2-Minute Valuation Model values Home Depot stock at $410 per share in 2 years.

- That’s a potential 13% upside from today’s price of $363 per share.

- Home Depot’s EPS is projected to grow a total of about 20% over the next three years.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

As the world’s largest home improvement retailer, The Home Depot (HD) has established itself as a dominant force in the retail landscape. With over 2,300 stores across North America, Home Depot has consistently demonstrated resilience through economic cycles while delivering value to shareholders.

After exceptional growth during the pandemic-driven home improvement boom, Home Depot is now navigating a normalized demand environment.

Let’s see why Home Depot stock could be overvalued today, even though it’s still an excellent business.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings per share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why Home Depot Stock Looks Overvalued

Forecast

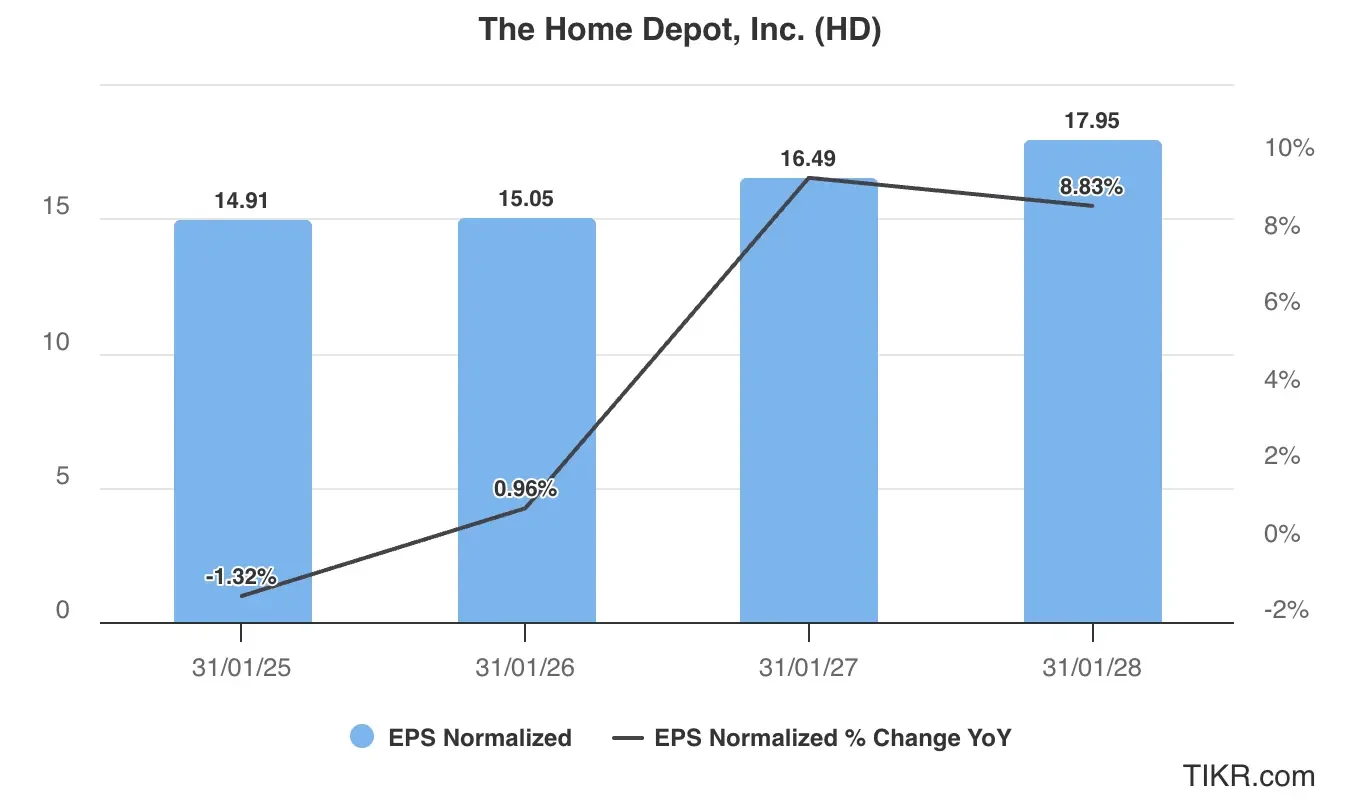

Home Depot’s projected earnings profile shows initial weakness in fiscal 2026 followed by accelerating growth. This pattern suggests that Home Depot is likely experiencing near-term pressure from the housing market slowdown and normalization of pandemic-driven demand.

However, the projected acceleration in fiscal 2027 and 2028 indicates that analysts are confident in the company’s ability to drive growth through operational excellence, market share gains, and the eventual recovery in housing and renovation activity.

This earnings growth for HD stock is likely to be driven by:

- Market Leadership: HD maintains a dominant position in the home improvement retail space, with scale advantages and brand recognition.

- Operational Excellence: The company consistently delivers industry-leading metrics in inventory management, supply chain efficiency, and store productivity.

- Professional Customer Focus: Home Depot has successfully expanded its penetration of the professional contractor market, which provides consistent demand and higher average transaction values.

- Omnichannel Capabilities: The company has built robust e-commerce and omnichannel capabilities that complement its physical store network, positioning it well in the evolving retail landscape.

We’ll make a conservative assumption in our valuation that Home Depot stock will report $17 in EPS in fiscal 2028.

Check out Home Depot’s full analyst estimates (It’s free) >>>

Is $HD Stock Overvalued Right Now?

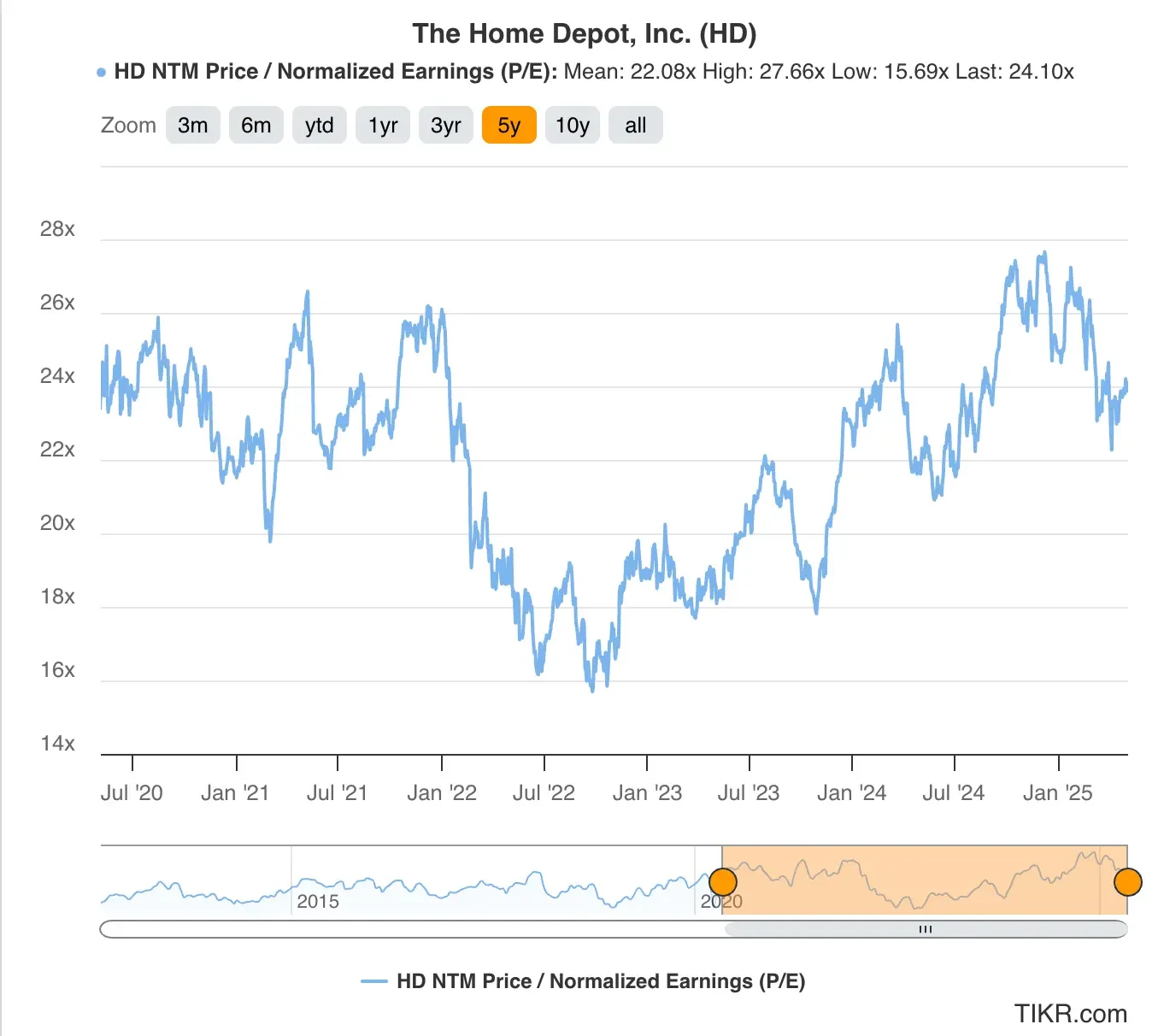

Home Depot stock is trading slightly above its 5-year historical average multiple, suggesting the market recognizes its competitive strengths and resilient business model.

Over the last five years, HD stock has averaged a forward P/E multiple of 22x, with peaks above 27x. Currently, HD stock trades at about 24 times forward earnings.

We’ll use a forward P/E multiple of 23x for our valuation, which is above the historical average trading multiple but below the current multiple.

HD stock could maintain its current multiple if the business can sustain double-digit annual earnings growth after 2027.

Fair Value of HD Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $17

- Conservative forward P/E multiple: 23x

- Expected dividends over the next 2 years: $19

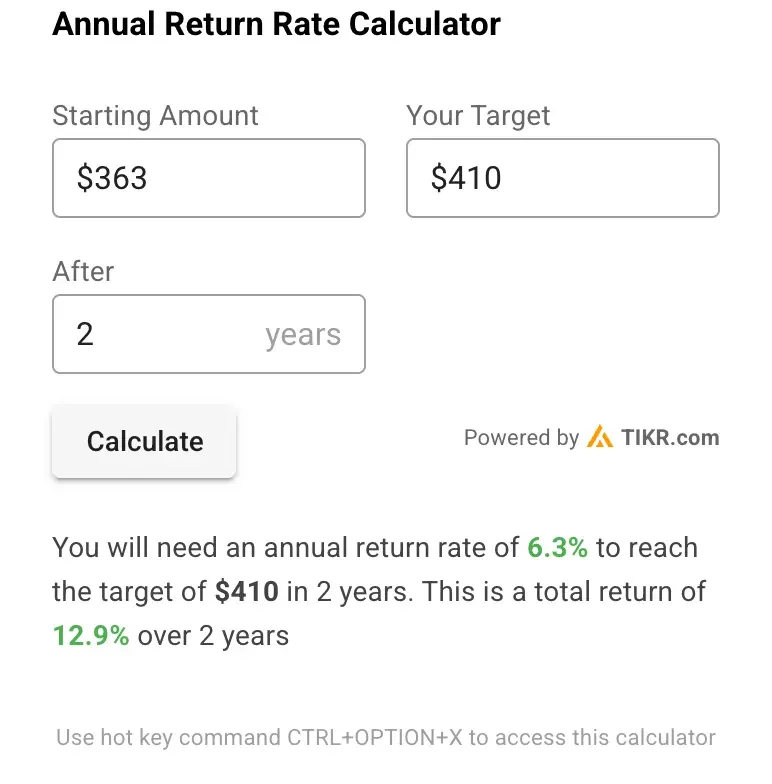

Expected Normalized EPS ($17) * Forward P/E ratio (23x) + Expected Dividends ($19) = Expected Share Price ($410)

The 2-year expected HD stock price we would get from this valuation is $410 per share.

With Home Depot stock currently trading at around $362 per share, this implies that the blue-chip stock could see a potential upside of 13% over the next two years or a 6% annualized return.

While HD stock offers upside potential over the next two years, it will likely underperform the broader markets.

For example, the S&P 500 index has generated an average annual return of 10% over the last six decades.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

What is the Target Price for HD Stock?

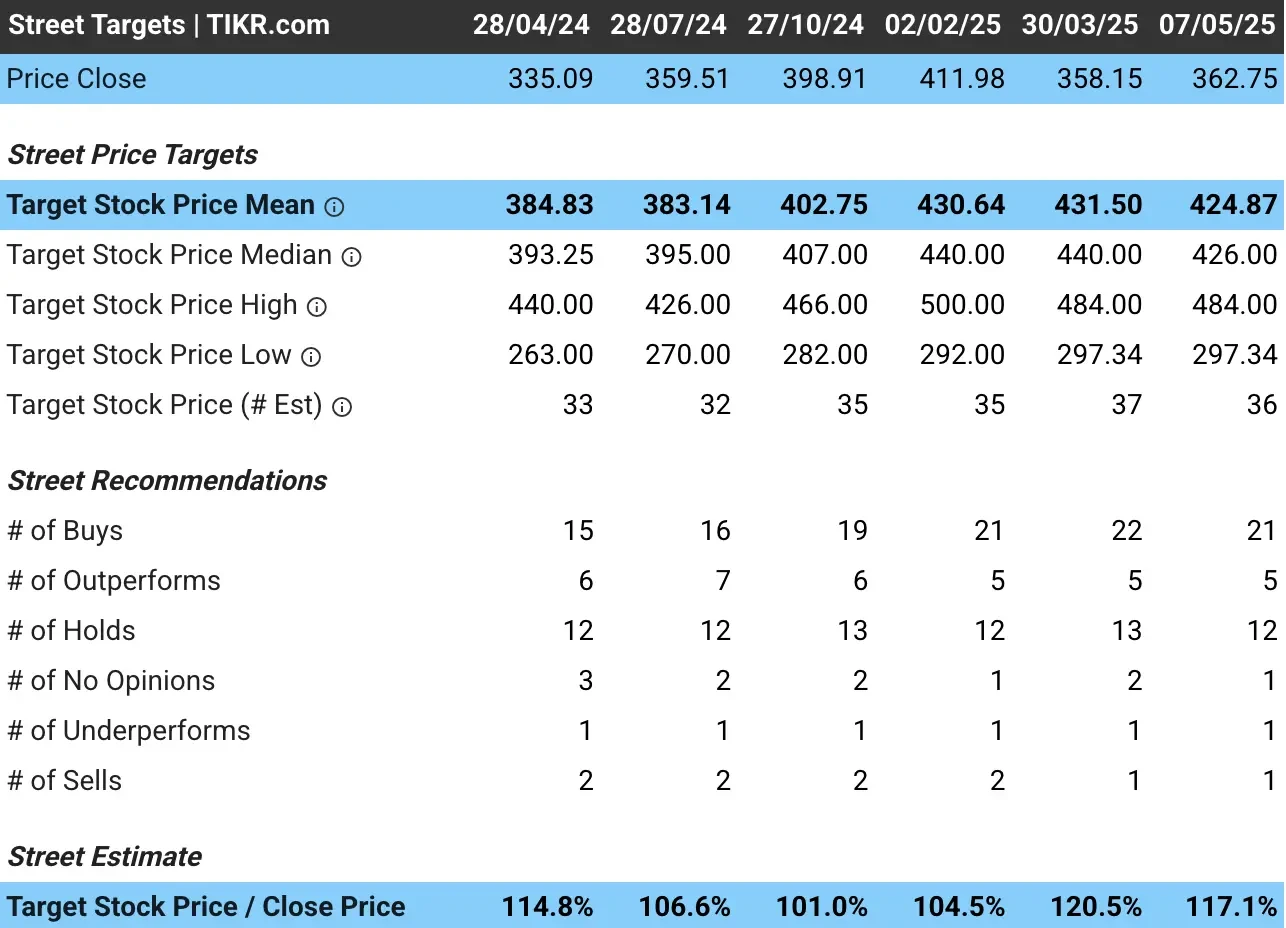

Analysts have an average price target of around $425 per share for Home Depot stock, indicating they see nearly 17% upside today for the home improvement giant based on its current share price:

Again, if HD stock saw 17% total returns over two years, it will likely underperform the broader markets, since the S&P 500 index has generated a 10% average annual return over the last six decades.

That leads us to believe that Home Depot could be slightly overvalued today.

Risks to Consider

Even though our valuation and analysts’ price targets suggest the stock could be worth around $410 per share, investors should be aware of several risks for the stock:

- Housing Market Sensitivity: The company’s performance is closely tied to housing market activity, which remains under pressure from elevated mortgage rates.

- Consumer Spending Environment: Macroeconomic uncertainties and inflation pressures could impact consumer willingness to undertake large home improvement projects.

- Competition: HD faces competition from traditional competitors like Lowe’s, specialized retailers, and e-commerce players expanding into home improvement.

- Valuation Risk: At current levels, HD’s valuation leaves limited room for error in execution or external economic pressures.

- Growth Saturation: With a mature store base in North America, HD faces challenges finding additional avenues for growth beyond market share gains and productivity improvements.

TIKR Takeaway

The Home Depot stock represents a high-quality retail investment with defensive characteristics and a history of shareholder value creation.

However, the stock might be a bit overvalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!