Key Stats for Dollar Tree Stock

- This Week Performance: -6%

- 52-Week Range: $61.8 to $142.4

- Current Price: $127

What Happened?

Dollar Tree‘s strategic transformation into a pure-play value retailer is proving its worth, with DLTR trading at $126.95 while delivering a 64% return in 2025, powered by record Halloween sales exceeding $200 million and a multi-price assortment generating 3.5x more profit per unit than standard items.

BMO Capital Markets delivered the sharpest blow on February 14, downgrading DLTR from “Market Perform” to “Underperform” and slashing its price target from $110 to $95, arguing the company lacks a compelling digital strategy and may have overlooked dis-synergies that threaten its margin expansion goals.

Despite the downgrade, Dollar Tree’s Q3 FY2025 results told a fundamentally stronger story, with net sales surging 9.4% to $4.7 billion, comparable sales accelerating to 4.2%, and adjusted EPS climbing 12% to $1.21, all driven by disciplined multi-price execution and 40 basis points of gross margin expansion to 35.8%.

The market is actively re-rating Dollar Tree from a stagnant discount retailer into a multi-price growth platform, as the company attracted 3 million new households in Q3 alone, with 60% earning over $100,000, signaling that the brand is transcending its core low-income customer base.

CFO Stewart Glendinning stated on the Q3 earnings call that “the stickering is sort of largely gone,” contextualizing the end of tariff-related restickering headwinds that compressed the SG&A rate by 160 basis points and weighed on traffic during the August to September peak disruption period.

Furthermore, of 28 brokerages covering DLTR, nine maintain “Buy” or higher ratings against only seven “Sell” ratings, with a median price target of $124.50, while the company itself has repurchased $1.5 billion in shares year-to-date at an average of $90 per share, representing roughly 8% of beginning shares outstanding.

Looking ahead, Dollar Tree’s algorithm targeting 12% to 15% adjusted EPS CAGR through 2028, supported by multi-price penetration that still covers only 15% of store sales dollars, positions the company to compound profitability well above traditional discount retail peers over the next three to five years.

Wall Street’s Take on DLTR Stock

BMO’s February 14 downgrade to “Underperform” with a $95 target introduces near-term pressure, but Dollar Tree’s Q4 earnings on March 16 will likely serve as the definitive reset, either validating or undermining the bear case against its multi-price transformation.

The fundamental picture shows stabilization rather than acceleration, with FY2026 EPS estimated at $5.75 (+4.3% YoY) and EBITDA margins recovering to 11.9% after compressing from 10.6% to 7.1% over the prior two fiscal years, suggesting the worst of the cost headwinds is now behind the business.

Wall Street currently shows 7 Buys, 2 Outperforms, 12 Holds, and 3 Sells against a mean price target of $125.30, implying just 1.4% downside from the current $126.95 price, with analysts holding conviction rather than chasing momentum as the company approaches its first post-Family Dollar full-year report.

The analyst target range spans $75.00 on the low end to $165.00 on the high end, with the bear case hinging on digital strategy gaps and dis-synergy risks flagged by BMO, while the bull case requires multi-price penetration to drive sustained comp acceleration and margin expansion through FY2028.

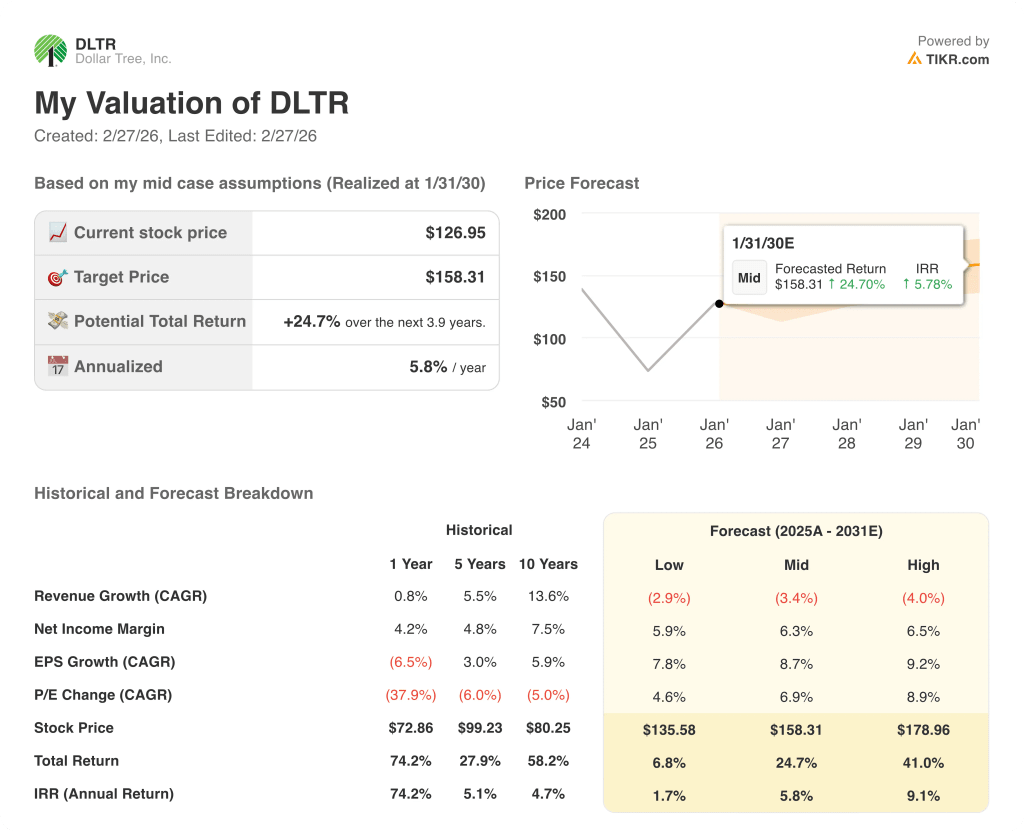

What Does the Valuation Model Say?

Given Dollar Tree’s trajectory toward 12% to 15% adjusted EPS CAGR through FY2028, a mid-case valuation model prices DLTR at $158.31, implying a 24.7% total return over 3.9 years at a 5.8% annualized IRR, a credible but modest return profile contingent on clean execution.

The most consequential risk remains revenue compression, with FY2026 estimates showing a 37% YoY revenue decline to $19.4 billion reflecting the Family Dollar divestiture, which could create confusion around comparable growth rates and pressure valuation multiples if traffic trends fail to recover meaningfully.

Overall, DLTR appears fairly valued at current prices, trading at just 1.3% above its mean analyst target, with the March 16 Q4 earnings call representing the critical inflection point where management’s Q4 comp guidance of 4% to 6% either confirms the multi-price growth thesis or forces a broader sentiment reset.

Should You Invest in Dollar Tree, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DLTR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Dollar Tree Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DLTR stock on TIKR for Free →