Key Stats for Carvana Stock

- Past-Week Performance: -6.3%

- 52-Week Range: $148.3 to $486.9

- Current Price: $299.6

What Happened?

WHAT HAPPENED

What started as a near-death story has become the fastest-growing company in used-car retail, with Carvana (CVNA), the online vehicle marketplace known for its glass-tower vending machines, posting 596,641 units sold in FY 2025, up 43%, at an 11% adjusted EBITDA margin that no traditional dealer has matched.

Carvana’s board approved a 5-for-1 stock split on March 13, sending shares up 2.8%, with stockholder approval scheduled for May 5 and split-adjusted trading set to begin May 7 under the existing CVNA ticker, a signal management reads investor demand for broader retail accessibility.

Reconditioning, the physical process of inspecting and repairing vehicles before sale, drove Q4 adjusted EBITDA to a record $511M even as non-vehicle costs pressured retail GPU by $255 per unit, while the company’s operating return on assets exceeded 20% for the year, a threshold associated with elite long-term compounders.

CEO Ernie Garcia stated on the Q4 2025 earnings call that “in the last 12 months, we increased customer selection by 20,000 cars… we are delivering cars to our customers a full day faster… we have reduced the interest rates our customers pay on their loans by about 1% relative to benchmark on average,” tying each gain directly to the company’s widening separation from the traditional dealer model.

Carvana’s path to its 3-million-unit, 13.5% adjusted EBITDA margin target rests on three converging forces: $18B-plus in committed loan purchase capacity that funds its financing flywheel, real estate already sized for 3 million annual units, and fixed cost leverage management estimates will contribute roughly 2 percentage points of margin expansion on its own.

Wall Street’s Take on CVNA Stock

The 5-for-1 split resolves a retail accessibility problem, but the real re-rating catalyst is the revenue inflection already in motion: $20.3B in 2025 actuals, per TIKR, tracking toward $26.9B in 2026 on 32.1% estimated growth, powered by the same reconditioning and logistics flywheel Garcia described at Morgan Stanley Technology Conference.

TIKR estimates revenue compounding at 22.8% annually through 2030 in the mid case, supported by Carvana’s stated fixed cost leverage thesis, which management quantified at roughly 2 percentage points of EBITDA margin expansion even before operational efficiency gains flow through.

Eighteen of 25 analysts covering CVNA rate it buy or outperform, with a mean price target of $428.50 representing 43% upside from the March 23 close of $299.60, as the Street prices in continued unit growth and margin recovery following Q4’s reconditioning cost overhang.

The spread between the $300 low and $519 high target reflects a binary read on reconditioning execution: bears anchored at $300 are essentially pricing the cost pressure as structural, while bulls at $519 are pricing the Garcia-described 3-to-6-month operational reset as credible.

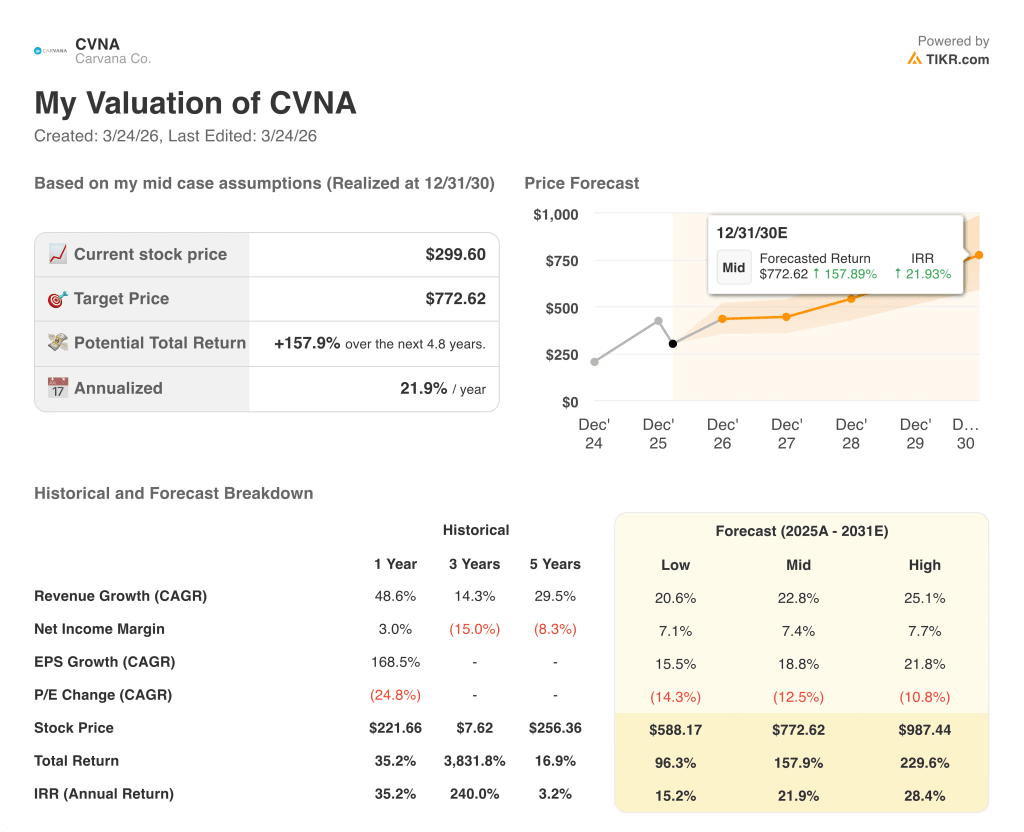

What Does the Valuation Model Say?

Moreover, the TIKR mid-case model prices CVNA at $772.62 by December 2030, embedding a 22.8% revenue CAGR and EBITDA margin expansion from 11% to 12.4%, driven by fixed cost leverage on a platform already owning real estate for 3 million annual units with facilities built for 1.5 million.

The market is pricing a recovering used-car retailer; the financials describe a platform compounder, with FCF set to more than double from $0.89B to $1.87B in 2026 alone.

That FCF inflection, paired with Carvana’s $12B-plus in committed loan purchase agreements securing its financing margin, gives the TIKR $772.62 target its most defensible foundation.

Further, Garcia’s confirmation at Morgan Stanley on March 2 that reconditioning teams had their best stretch in over a year signals the Q4 cost miss was cyclical, not structural.

Reconditioning cost per unit deteriorating beyond Q1 breaks the margin expansion assumption; if EBITDA margin stalls below 11% through mid-2026, the $772.62 TIKR target loses its anchor.

Q1 2026 retail GPU is the number to watch at the next earnings release: management guided a sequential increase despite elevated non-vehicle costs, and any miss reopens the structural cost debate.

Should You Invest in Carvana Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CVNA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carvana Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CVNA stock on TIKR for Free →