Key Takeaways:

- Datadog’s AI-native customer cohort is growing rapidly, contributing about 8.5% of ARR and fueling significant future growth.

- With 83% of customers using two or more products and rapidly accelerating adoption of newer offerings like Flex Logs, Datadog’s platform strategy is driving strong expansion.

- Despite trading at a premium valuation, analysts see over 35% upside potential for DDOG stock, with an average price target of $143.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Datadog (DDOG) has established itself as the leader in cloud observability, helping enterprises monitor and secure their mission-critical applications.

With the rise of AI workloads and continued cloud migration, Datadog’s growth opportunity is continuing to expand.

If you’re searching for a software company that combines strong fundamentals with future growth potential, here are three compelling reasons to consider DDOG stock right now.

Find the best stocks to buy today with TIKR. (It’s free) >>>

1. Strong AI Tailwinds Driving Growth

Datadog is uniquely positioned to capitalize on the AI boom. Already, AI-native customers make up 8.5% of Datadog’s ARR, up from just 3.5% a year ago, and contributed about 6 points of the company’s year-over-year revenue growth in Q1 of 2025.

This opportunity isn’t limited to the handful of tech giants. Datadog now has over 10 AI-native companies spending more than $1 million annually, and this customer cohort continues expanding rapidly.

With AI adoption exploding, companies need better ways to monitor their models, and Datadog’s platform is built for exactly that.

As Datadog CEO Olivier Pomel explained, AI is shifting value from writing code to understanding, operating, and securing it.

2. Industry-Leading Platform Adoption and Expansion

Datadog’s land-and-expand strategy continues to drive impressive results. At the end of Q1, 83% of customers were using two or more products (up from 82% last year), while 51% were using four or more products (up from 47%), and 28% were using six or more products (up from 23%).

This multi-product adoption translates directly to higher customer spend and stickier relationships. Datadog’s newer products are showing impressive traction:

- Flex Logs reached $50 million in ARR in just six quarters, which is the fastest product ramp in company history.

- Database Monitoring is approaching $50 million ARR with over 5,000 customer adoptions and 60% year-over-year growth.

With newer offerings in security, LLM observability, and data quality (through recent acquisitions of Metaplane and Eppo), Datadog is continuously expanding its addressable market.

This development engine is powered by substantial R&D investment, which at 30% of revenue is significantly higher than that of competitors.

Check out DDOG’s full analyst estimates (It’s free) >>>

3. Strong Enterprise Momentum and Bookings Growth

Datadog is winning larger deals at an accelerating pace. In Q1, it signed 11 deals with a total contract value of $10 million or more, up from just one such deal in the year-ago quarter. Dollar bookings for new logos also increased by over 70% year-over-year.

This enterprise momentum showcases Datadog’s ability to displace legacy vendors and consolidate observability spending.

One major U.S. car manufacturer signed a seven-figure deal to deploy 13 Datadog products across dozens of business units, replacing a dozen existing tools.

Similarly, a major Latin American bank and a large American pet supplies retailer each consolidated multiple tools onto Datadog’s platform, with expected cost savings exceeding $1 million annually.

These large enterprises are choosing Datadog for its ability to provide unified observability across diverse environments, from on-premises to multi-cloud to IoT and mobile applications. As companies become more complex and hybrid, Datadog’s comprehensive platform becomes increasingly valuable.

Why Datadog Stock Looks Undervalued Today

At around 63x forward earnings, DDOG stock trades at a premium, but analysts still see significant upside.

Value stocks quicker with TIKR (It’s free, no card required) >>>

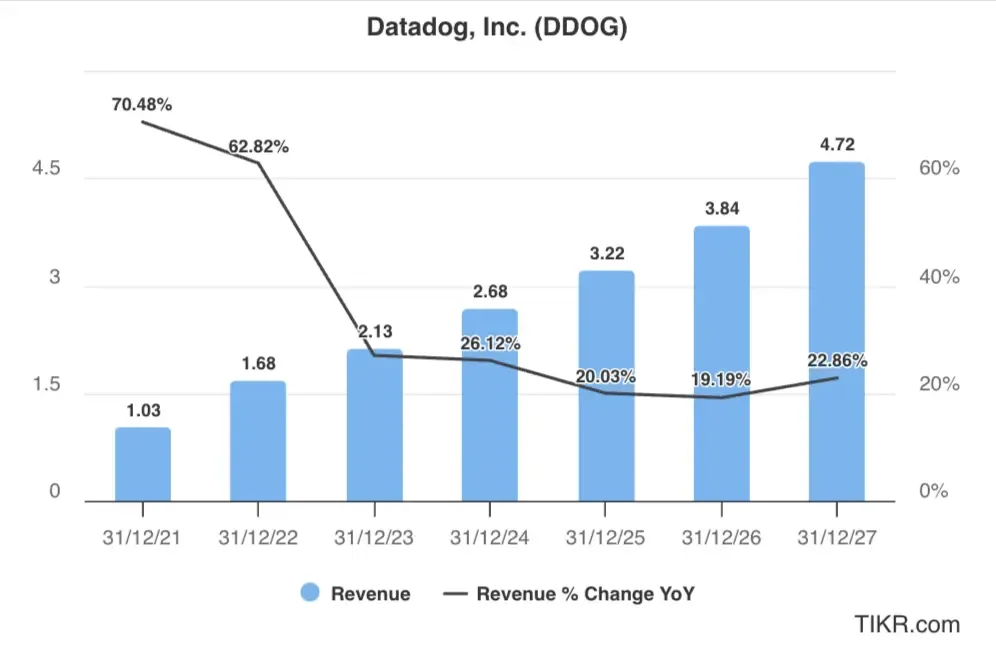

Analysts tracking DDOG stock expect adjusted earnings to expand from $1.82 per share in 2024 to $2.63 per share in 2027. If the tech stock is priced at 60x forward earnings, it will trade around $150 in early 2027.

The average price target of $143 for Datadog stock suggests that the stock has over 35% potential upside from its current price. That’s probably why analysts are heavily weighted toward Buy ratings.

TIKR Takeaway for DDOG Stock

While Datadog’s growth has slowed down from its COVID-era peak, its expansion into new product areas, growing enterprise adoption, and AI tailwinds provide multiple growth vectors.

With a gross margin of 80%, industry-leading R&D investment, and a strong free cash flow margin of 32%, Datadog stock offers a compelling combination of growth and profitability that positions it well for the long term.

Is DDOG stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!