Key Takeaways:

- Conagra Brands stock offers a rare combination of a 7.2% dividend yield and a historically defensive business model built around household food staples.

- While dividend growth has paused, analysts believe the stock could deliver over 12% annual returns through 2028 if margins recover and the stock’s valuation multiple improves.

- With nearly 40% upside potential and strong free cash flow coverage, Conagra may appeal to income investors looking for stability and long-term value.

- Unlock our Free Report: 5 undervalued compounders with upside based on Wall Street’s growth estimates that could deliver market-beating returns (Sign up for TIKR, it’s free) >>>

Conagra Brands isn’t the most exciting stock, but it’s a steady part of millions of kitchens.

The company owns well-known food brands like Hunt’s, Birds Eye, Healthy Choice, and Slim Jim. These are products people keep buying regardless of how the economy is doing. But over the last two years, rising costs have hurt profits and pushed the stock down nearly 40% from its highs.

Because of that drop, Conagra now trades at a discount and offers a 7.2% dividend yield, the highest it’s been in over 5 years. With earnings expected to improve and the dividend supported by strong cash flow, this might be a solid chance to grab a reliable income stock at a low price.

Analysts Think the Stock is Strongly Undervalued Today

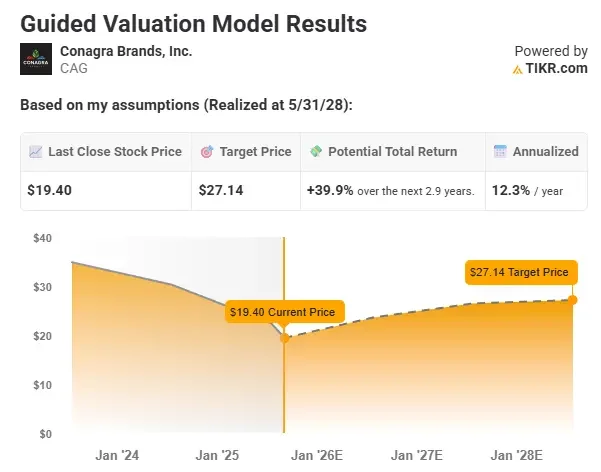

Conagra shares trade around $19. Based on analysts’ estimates, the stock could be worth $27/share by mid-2028, which would imply a total return of about 40% or 12.3% annual returns.

With a 7.2% dividend yield and room for upside, Conagra looks like a high-yield stock trading below fair value.

Value any stock in less than 60 seconds with TIKR (It’s free) >>>

Conagra’s Dividend Yield

Conagra’s dividend yield is sitting at 7.2%, the highest it’s been in the last 10 years and well above its 5-year average of 4.1%.

The high dividend yield today is due to Conagra’s stock dropping over 40% in the past 3 years after rising costs and shrinking margins hurt earnings. Prices for ingredients, packaging, and transportation spiked, and while Conagra raised prices across its brands, it wasn’t enough to fully offset the impact.

At the same time, demand softened. Consumers became more cautious with grocery spending, leading to volume declines across Conagra’s portfolio.

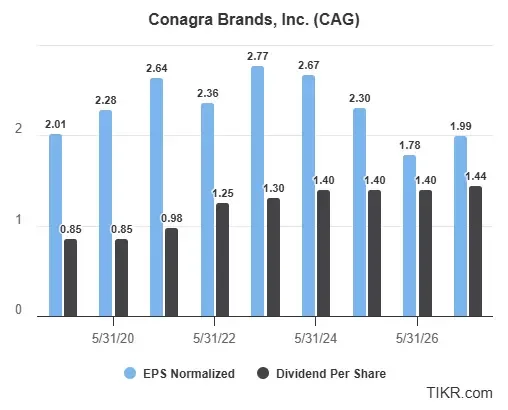

Even with all that, Conagra has kept its $1.40 per share dividend steady. Analysts expect earnings to gradually recover over the next two years as costs normalize and pricing sticks. If that plays out, the current 7.2% yield could look especially attractive in hindsight.

Find high-quality dividend stocks that look even better than Conagra today. (It’s free) >>>

Conagra’s Dividend Safety

While Conagra’s earnings have fallen in recent years, they are expected to stabilize and gradually recover. Analysts project EPS to rise from a low of $1.78 in fiscal 2026 to nearly $2.00 by 2027. That recovery reflects easing cost pressures, better supply chain efficiency, and stronger pricing across its portfolio. If these trends continue, earnings should once again cover the dividend with more room to spare.

Conagra has kept its $1.40 dividend intact even as profits declined, with the payout ratio expected to climb above 75% in 2026. Looking ahead, if earnings improve as expected, the payout ratio could fall closer to 70% by 2027. This would be a high payout ratio, but it’s reasonable for a consumer staples business.

With strong brands and stable demand, Conagra remains positioned to support the dividend and reward patient investors if earnings recover.

See Conagra’s full growth forecast and analyst estimates. (It’s free) >>>

TIKR Takeaway

Conagra isn’t growing fast, but the current yield and valuation leave room for solid total returns.

Right now, the stock’s sitting at $19.40, which looks cheap compared to its estimated value. TIKR’s model has a fair value closer to $27 by 2028, which would be about 40% upside.

If earnings bounce back and you collect the 7.2% dividend yield along the way, you’re looking at potential returns of over 12% a year.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!