Bombardier Inc. (BBD.B) has staged one of the most impressive industrial comebacks in Canada. Once burdened by debt and uneven execution, the company now designs and builds some of the world’s leading business jets, anchored by its Global and Challenger platforms, and supports a growing aftermarket services business.

After divesting rail and commercial aircraft units earlier this decade, Bombardier is now a focused, pure-play private aviation company competing against Gulfstream and Dassault in a high-margin niche.

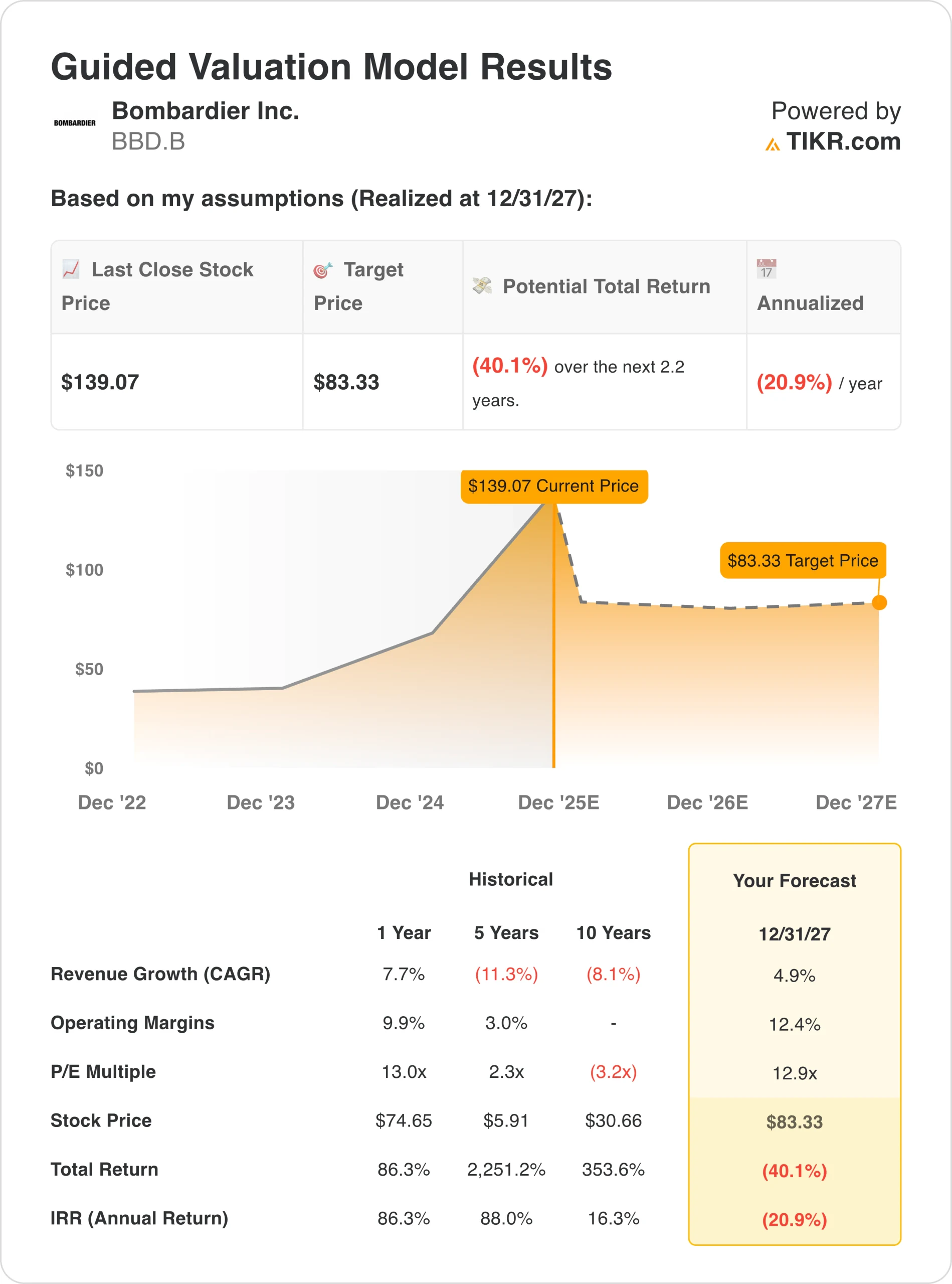

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

In 2025, that focus is paying off as the company delivered 59 aircraft in the first half, kept year-over-year volume steady, and grew revenue by 19% in Q1 to US$1.5 billion and another US$2.0 billion in Q2. Services revenue climbed 16% to US$590 million, and the backlog jumped to US$16.1 billion, Bombardier’s largest in more than a decade, after securing a massive 50-jet order (plus 70 options) from a new customer.

CEO Éric Martel credited “rock-solid fundamentals” and years of balance-sheet repair for giving Bombardier the flexibility to expand globally while weathering supply-chain and tariff pressures.

The turnaround has also brought credibility on the financial side. In Q2, adjusted EBITDA reached US$297 million, and net income soared to US$193 million, while both S&P Global and Moody’s upgraded the company’s outlook. With liquidity of US$1.2 billion and leverage trending down, Bombardier reaffirmed 2025 guidance: revenue above US$9.25 billion, adjusted EBITDA above US$1.55 billion, and free cash flow of US$500–$800 million.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Bombardier’s second quarter underscored just how far the company has come since its near-collapse earlier this decade. Total revenue came in at US$2.0 billion, down modestly year-over-year due to the timing of deliveries but supported by a record quarter in its Services segment. That division’s US$590 million contribution (+16%) now accounts for nearly one-third of total revenue, providing recurring, higher-margin stability that smooths the cyclicality of new jet sales.

| Metric | Result | YoY Change | Commentary |

|---|---|---|---|

| Revenue | US$2.0 B | ▼ 8% | Lower deliveries offset by stronger pricing |

| Adjusted EBITDA | US$297 M | ▼ 11% | Services mix and margin compression |

| Adjusted EBIT | US$205 M | +7% | Higher efficiency and pricing power |

| Net Income | US$193 M | ▲ >$170 M | Reflects stronger operations and FX gains |

| Adjusted EPS | US$1.11 | +7% | Up from US$1.04 in Q2 2024 |

| Free Cash Flow | –US$164 M | vs –US$68 M | Inventory build for H2 deliveries |

| Backlog | US$16.1 B | ▲ US$1.9 B QoQ | Highest in a decade |

| Liquidity | US$1.2 B | Stable | Sufficient to fund production |

| Credit Rating | BB– (S&P) | Up 1 notch | Positive momentum continues |

Profitability remained strong. Adjusted EBITDA of US$297 million represented a double-digit margin of 15%, while reported EBIT climbed 7% to US$205 million. Free cash flow usage widened to US$164 million, as the company intentionally built inventory to support higher second-half production. On the capital front, Bombardier refinanced US$500 million of notes due 2027, pushing maturities out to 2033, and secured credit upgrades from both S&P and Moody’s, milestones that validate its improved balance sheet.

Review Bombardier’s full financial results & estimates (It’s free) >>>

Broader Market Context

Business aviation has stayed resilient despite macro uncertainty. Utilization levels remain well above pre-pandemic averages, driven by corporate fleet renewals and ultra-high-net-worth travel demand. Bombardier has also tapped into the defense aviation market, where government and surveillance orders are emerging as a new growth pillar. At the same time, its aftermarket services, from maintenance and retrofits to flight-operations support, have become essential to both profit stability and customer loyalty.

The company’s renewed discipline mirrors broader shifts in the aerospace industry: fewer speculative orders, leaner production cycles, and stronger pricing controls. Bombardier’s transformation into a high-margin, cash-flow-focused manufacturer has made it a compelling case study in operational reinvention, especially as investors compare it with diversified peers such as Airbus or Textron.

1. Record Backlog Reinforces Multi-Year Visibility

Bombardier’s US$16.1 billion backlog marks its strongest order book since the early 2010s. The headline deal, a 50-aircraft firm order plus 70 options worth up to US$4 billion, has given the company exceptional visibility through 2027. The resulting 2.3x book-to-bill ratio shows that new demand far outpaces deliveries, even amid rising prices.

This backlog reflects not just cyclical tailwinds but also a deliberate strategy to deepen customer relationships through fleet agreements, long-term maintenance plans, and integrated service packages. For Bombardier, backlog isn’t just about volume, it’s a sign of confidence in its performance, reliability, and post-delivery support network.

2. Services Business Becomes the Stabilizer

Services are the backbone of Bombardier’s earnings consistency. The company operates 10 service facilities across six countries, with new sites coming online in Abu Dhabi and London Biggin Hill. This global network supports more than 5,100 aircraft in service and generates high-margin recurring revenue.

In Q2, services grew 16% year over year to US$590 million, driven by expanded maintenance contracts and retrofit demand. Management continues to recruit technicians worldwide, aiming to convert Bombardier’s installed fleet into a lifetime revenue stream. The long-term ambition is clear: shift the business mix toward a 60/40 split between aircraft sales and aftermarket, stabilizing margins even when jet deliveries plateau.

Value stocks like Bombardier in less than 60 seconds with TIKR (It’s free) >>>

3. Balance-Sheet Repair and Ratings Momentum

Debt reduction remains central to the story. Bombardier’s successful refinancing of US$500 million of 2027 notes extended maturities to 2033 and trimmed interest costs. That move, coupled with consistent cash-flow discipline, earned an upgrade to BB- from S&P and a positive outlook from Moody’s, marking the company’s best credit standing in more than a decade.

Available liquidity stands at US$1.2 billion, and the company projects free cash flow of US$500–$800 million for 2025, supported by lower capex and steady service cash conversion. The improved rating also broadens institutional access and lowers refinancing risk, potentially enabling future capital returns once leverage targets are met.

The TIKR Takeaway

Bombardier has transitioned from a turnaround to a growth-compounder. Its backlog strength, growing service ecosystem, and disciplined execution are giving investors reason to believe the rally is justified. The next test will be converting backlog into consistent free cash flow while maintaining delivery momentum amid supply-chain and tariff headwinds.

From an investment perspective, Bombardier remains one of Canada’s most dynamic industrial stories. With operating leverage intact, services expansion underway, and debt metrics trending down, the setup for 2026 looks favorable. If the company can maintain its cost discipline and sustain an EBITDA margin of>15%, it could finally graduate from “recovery stock” to a long-term compounder.

Should You Buy, Sell, or Hold Bombardier Stock in 2025?

Bombardier’s execution continues to impress. With shares up 100% year-to-date, investors might expect some turbulence, but fundamentals justify the ascent. The backlog provides multi-year visibility, the balance sheet is healthier than at any point since 2010, and services growth adds stability. While short-term cost pressures could cause fluctuations, the structural story remains intact. For patient investors, Bombardier still offers altitude to climb.

How Much Upside Does Bombardier Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!