Westpac Banking Corporation (WBC) enters 2026 with a steadier operating profile, a stronger capital base, and a business mix that is becoming more predictable than it was at the start of the cycle. The stock has staged a meaningful recovery over the past year, supported by cleaner credit trends and better margin visibility as deposit pricing pressures ease. Investors are watching whether this momentum carries into the next stage of the cycle, especially as the rate environment shifts from tailwind to neutral.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)>>>

The bank’s recent results highlighted a more disciplined balance-sheet approach, with management focused on maintaining stable returns while navigating a competitive lending market. After several reporting periods marked by cost volatility, Westpac has emphasized tightening operating discipline and prioritizing higher-return capital projects. That shift has helped rebuild confidence in the bank’s medium-term earnings power.

Westpac’s story now centers on execution: delivering stable net interest margins, keeping credit losses contained as household stress rises, and showing clearer cost progress across the enterprise. With the valuation near the middle of its historical range, investors are calibrating expectations for a bank that is not aiming for rapid growth but for a more durable earnings base. The next few quarters will show whether Westpac can convert this positioning into consistent performance.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

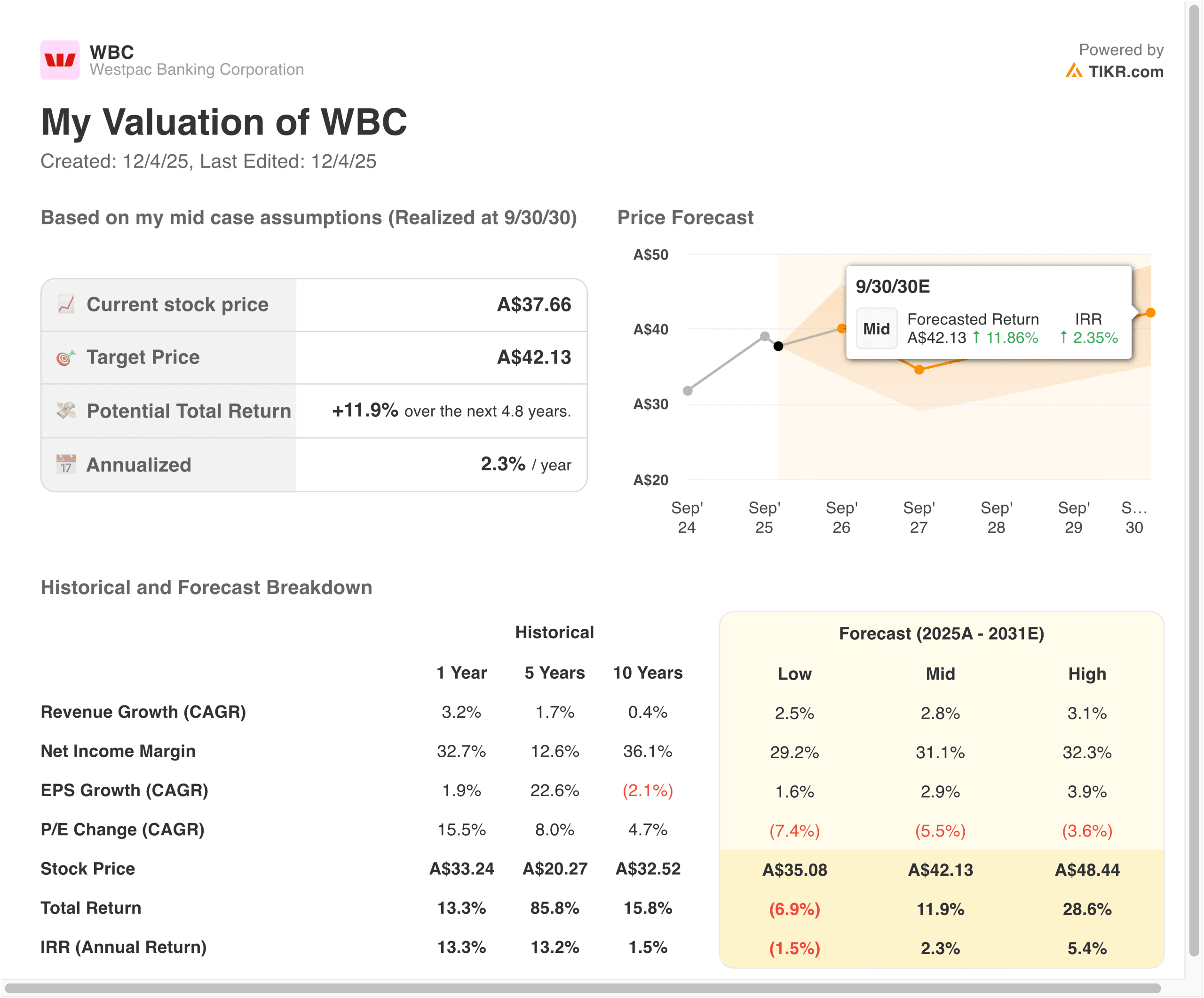

Westpac’s latest results show modest revenue growth alongside stronger profitability, reflecting a more stable net interest margin and disciplined asset pricing. Revenue expanded 3.2% year over year, while the net interest margin held firmer than feared as deposit repricing pressures eased. The bank continued shifting its lending mix toward segments with more reliable returns, helping smooth rate-cycle volatility.

| Metric | FY 2024 | FY 2025 | Trend |

|---|---|---|---|

| Revenue Growth | 1.7% | 3.2% | Improving |

| Net Income Margin | 12.6% | 32.7% | Significantly stronger |

| EPS Growth | 22.6% (5yr CAGR) | 1.9% (YoY) | Stable earnings base |

| P/E Change | 8.0% (5yr CAGR) | 15.5% (YoY) | Rising valuation support |

| Total Return | 85.8% (5yr) | 13.3% (YoY) | Strong multi-year compounding |

| IRR | 13.2% (5yr) | 13.3% (YoY) | Consistent |

Earnings quality improved as cost discipline became a clearer priority. Operating expense growth slowed meaningfully, with management signaling that simplification initiatives will remain a core focus through 2026. EPS grew 1.9% year over year and has compounded at 22.6% over the past five years, supported by steady returns and smaller impairment charges across the portfolio. This has helped ease concerns that elevated inflation would meaningfully erode bank profitability.

The balance sheet remains a strong point. Westpac reported a CET1 ratio comfortably above regulatory minimums, giving the bank flexibility to maintain dividends and consider buybacks when conditions allow. Credit quality trends remain benign, with impaired loans stable and early-stage delinquencies rising only modestly. This backdrop supports a more predictable earnings base heading into 2026.

Look up Westpac Banking’s full financial results & estimates (It’s free)>>>

Broader Market Context

Australia’s banking landscape remains competitive, with lenders fighting for share in mortgages, small business lending, and deposits. Rate cuts expected in 2026 could compress margins, but they may also support better credit outcomes by easing household pressure. This creates a mixed but more balanced backdrop than the high-rate environment of 2024–2025.

Regulators continue to highlight capital strength, operational resilience, and responsible lending as focal points for the sector. Westpac enters this period with a stronger capital buffer and a more conservative credit posture, which should help stabilize earnings even if growth remains modest. Investors are weighing whether this foundation is enough to drive consistent returns in a slower economic environment.

1. Margin Stability and Competitive Positioning

Westpac’s margin story hinges on managing deposit competition while maintaining discipline on loan pricing. The past year showed that margins can hold up even when competition intensifies, largely due to better deposit mix and repricing strategies that emphasize long-term stability over short-term volume. Management has signaled that protecting margin resilience will remain a top priority, which is critical as rate cuts eventually cycle through earnings. Investors should expect margin performance to remain a key driver of sentiment throughout 2026.

The competitive environment remains intense, especially in mortgages, where pricing continues to compress across the industry. Westpac has chosen to prioritize return rather than chase volume, and that is beginning to show in steadier profitability. The question for investors is whether this discipline can offset cyclical pressures. If deposit costs remain well-managed and loan mix continues shifting toward higher-return categories, Westpac could maintain a firmer margin profile than peers.

2. Credit Quality and Household Resilience

Credit conditions have remained favorable despite rising household stress indicators. Westpac has seen only modest increases in early-stage arrears, with impaired loans staying stable across most categories. Strong employment levels and stable collateral values continue to support credit outcomes. As the rate environment normalizes, investors will look for signs that loss rates remain contained.

Household leverage remains elevated, and the bank recognizes that a softer consumer backdrop could create pockets of credit pressure. However, Westpac’s conservative underwriting approach and diversified book position it well to manage any cyclical challenges. The next several quarters of data will be important in confirming whether credit normalization remains gradual rather than abrupt.

Value stocks like Westpac Banking Corporation in less than 60 seconds with TIKR (It’s free) >>>

3. Capital Returns and Long-Term Earnings Potential

Westpac’s capital position remains a core strength, giving management the capacity to sustain dividends and consider buybacks when conditions align. The bank has consistently emphasized prudent capital deployment, prioritizing balance-sheet durability while still aiming to reward shareholders. As earnings stabilize, capital returns may become a more important component of the investment case.

Earnings growth is not expected to be rapid, but it may be more predictable than in prior cycles. Technology investment, efficiency gains, and portfolio simplification provide a pathway for incremental earnings improvements. Investors will watch whether management executes consistently enough to deliver steady compounding, even in a low-growth macro environment.

The TIKR Takeaway

TIKR’s valuation model points to moderate upside for Westpac over the next several years, driven by stable margins, disciplined credit management, and strong capital positioning. The bank is not a fast-growing story, but rather a steady operator aiming to deliver consistent returns with lower earnings volatility. For investors focused on stability and income, Westpac’s profile remains aligned with a more predictable long-term setup.

Should You Buy, Sell, or Hold Westpac Stock in 2025?

Westpac offers a steadier earnings base compared with earlier cycles, supported by margin discipline and strong capital levels. The medium-term outlook depends on consistent execution and the macro rate path. Investors may want to watch upcoming quarters for clearer confirmation that earnings stability can hold through a changing rate environment.

How Much Upside Does Westpac Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!