Key Takeaways:

- Wells Fargo’s asset cap was officially removed on January 14, 2025, ending seven years of regulatory constraints.

- The bank has transformed into a fundamentally different institution with new leadership across 150 of its top 220 positions.

- Multiple growth opportunities are now available across consumer banking, wealth management, and commercial lending.

- Unlock our Free Report: 5 stock screeners inspired by top investors like Warren Buffett to help you find high-upside stock ideas (Sign up for TIKR, it’s free) >>>

Wells Fargo (WFC) reached a pivotal milestone this month with the Federal Reserve’s removal of the $1.95 trillion asset cap that had constrained the bank’s growth for seven years.

This regulatory breakthrough marks the culmination of extensive risk management improvements, positioning the banking giant for expansion across multiple business lines.

WFC stock has nearly tripled in market value over the past five years, outpacing the broader market by a wide margin. However, let’s examine whether you should own Wells Fargo stock at its current price.

1. WFC Stock to Benefit From Multiple Growth Drivers

The asset cap removal reflects Wells Fargo’s comprehensive transformation since the arrival of CEO Charlie Scharf in 2019. The bank has rebuilt its leadership team, with 15 of 17 operating committee members being new to the company. Approximately 150 of the top 220 executives represent fresh talent brought in to drive the institution forward.

“We’re a very different company than we were 5, 6 years ago,” noted CFO Mike Santomassimo during a recent investor conference. The bank has successfully closed 11 consent orders since 2019, with five additional orders terminated in the first quarter of 2025 alone, demonstrating substantial progress in risk management and regulatory compliance.

This operational overhaul provides Wells Fargo with the foundation to capitalize on its extensive franchise advantages, including 4,000 branches nationwide, strong brand recognition, and comprehensive product offerings spanning consumer banking, wealth management, and commercial services.

The removal of the asset cap unlocks growth opportunities across Wells Fargo’s diversified business portfolio. On the consumer side, the bank has been investing heavily in branch refurbishment, completing approximately 750 locations this year as part of a broader modernization effort covering 1,500-2,000 branches.

The consumer lending business shows particular promise, with the credit card portfolio demonstrating strong momentum since leadership changes in 2019. The bank has launched 11 new card products and replatformed its entire offering, driving sustainable growth in new accounts while maintaining disciplined credit standards.

Wells Fargo’s wealth management business is experiencing a renaissance after years of advisor attrition. The bank now attracts top-tier advisory teams across the industry and operates through multiple channels, including branch-based advisors, independent registered investment advisors, and traditional wealth management offices. This diversified approach provides unique competitive advantages in capturing affluent customer relationships.

Check out Wells Fargo’s full analyst estimates and growth forecast (It’s free) >>>

2. WFC Stock to Benefit From Commercial Banking Expansion

The commercial banking segment could be a key growth driver for WFC stock in the post-asset cap environment. Wells Fargo has been systematically adding hundreds of commercial bankers across key markets where the bank believes it holds below-market share relative to its capabilities.

The Corporate Investment Banking division has also been rebuilding, adding dozens of senior investment bankers to fill coverage gaps across equity capital markets, debt capital markets, and merger advisory services. While balance sheet limitations previously constrained this business, the removal of the asset cap provides flexibility to finance trading positions and expand client relationships.

Increased balance sheet allocation is expected to immediately benefit trading revenue, enabling the bank to compete more effectively in financing-type activities that drive broader client relationships.

3. A Strong Balance Sheet

Wells Fargo enters this growth phase from a position of credit strength. It maintains disciplined underwriting standards across all portfolios, with management noting that payment rates in credit card portfolios are running slightly higher than modeled expectations.

Commercial credit performance remains stable with no systematic issues emerging across industry sectors. Even amid recent market volatility and economic uncertainty, credit trends have remained consistent with previous quarters.

The bank’s reserve approach incorporates multiple economic scenarios, with significant weighting toward downside cases, providing an appropriate cushion for potential economic headwinds while maintaining conservative credit provisions.

Wells Fargo maintains its 2025 net interest income guidance of 1-3% growth, although management expects results to be toward the lower end of this range, given current rate expectations. The bank’s strong capital position, with a CET1 ratio of 11.1% well above the 9.8% regulatory minimum, provides flexibility for growth investments.

Management has generated $12 billion in gross expense savings over recent years while simultaneously investing in growth initiatives, demonstrating the institution’s ability to self-fund expansion through productivity improvements.

Technology investments, including artificial intelligence applications in call centers and process automation, are expected to accelerate efficiency gains beyond historical levels.

Valuation Setup for WFC Stock

Despite the massive run-up in WFC stock, its valuation remains compelling relative to its growth trajectory.

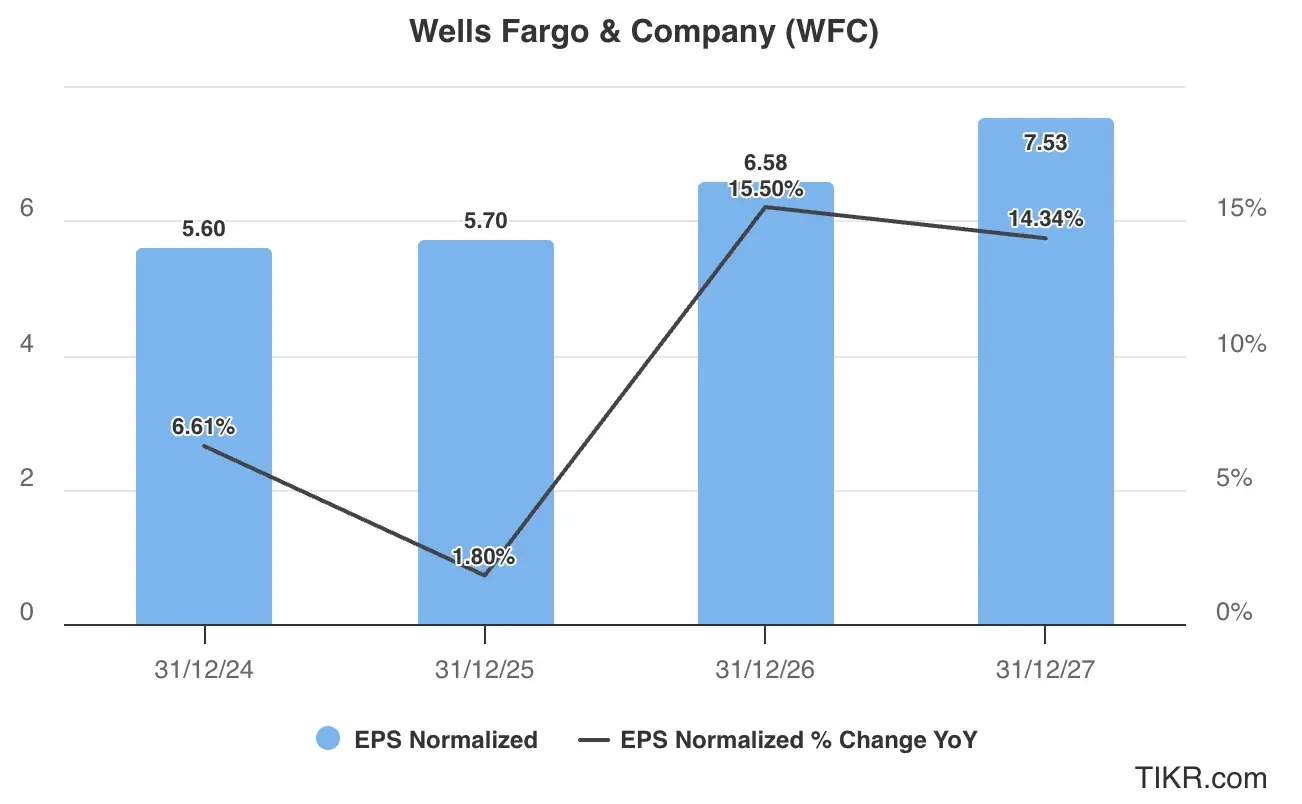

Analysts tracking Wells Fargo stock expect its sales to rise from $82.3 billion in 2024 to $89.5 billion in 2027, an annual increase of 28%. Comparatively, adjusted earnings are forecast to expand from $5.60 per share to $7.53 per share in this period.

WFC stock currently trades at a forward price-to-earnings multiple of 13x, which is above its 10-year average multiple of 12x.

If WFC stock is priced at a multiple of 12x and reaches its projected $7.53 in normalized EPS, it will trade around $90/share in June 2027, indicating an upside potential of 17% from current levels. If we adjust for dividend payments, cumulative returns will be more than 20%.

Quickly value any stock with TIKR’s Valuation Model (It’s free) >>>

Average Analyst Price Target for WFC Stock

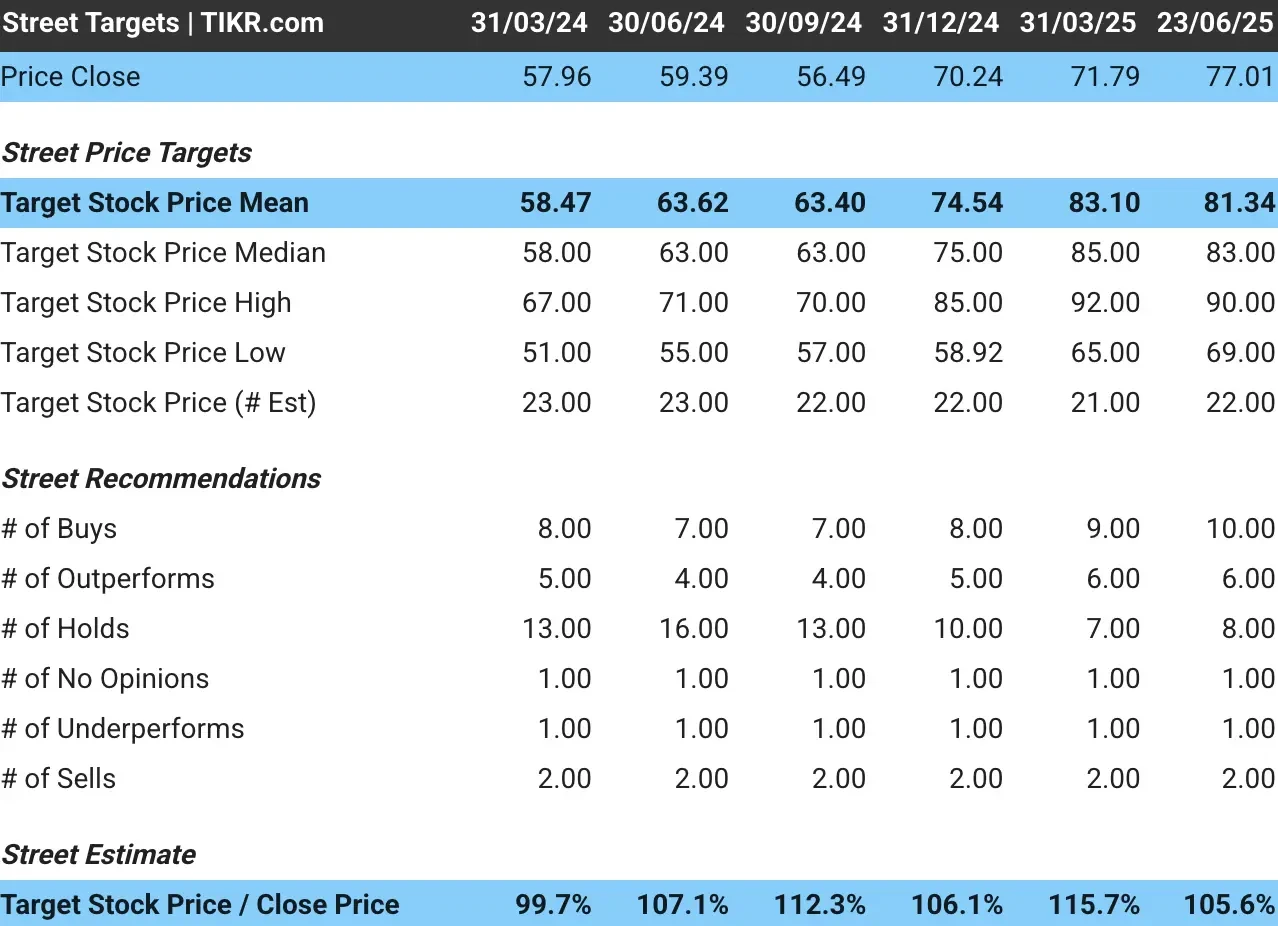

Wall Street remains bullish on WFC stock, with a consensus price target of $81/share. Analysts expect the stock to rise around 6% from current levels over the next 18 months.

Notably, WFC stock currently has a high target price of $90 and a low target price of $69.

Of the 27 analysts tracking Wells Fargo stock, 16 recommend “Buys”, eight recommend “Hold”, and three recommend “Sell.”

TIKR Takeaway for WFC Stock

Wells Fargo’s asset cap removal represents more than a regulatory milestone; it marks the transition from remediation to growth for one of the largest financial institutions in America. The bank has methodically rebuilt its operational foundation while maintaining strong market positions across consumer and commercial banking.

With excess capital, improving operational efficiency, and multiple growth vectors now unconstrained, Wells Fargo appears positioned for sustained expansion.

The 15% return on tangible common equity target may prove conservative given the bank’s comprehensive franchise advantages and newly available growth opportunities.

For investors seeking exposure to a disciplined, well-capitalized bank with significant operating leverage to U.S. economic growth, Wells Fargo presents a compelling opportunity as it enters its next growth phase.

FAQs

1. What is the market cap of WFC stock?

The market cap of WFC stock is $250 billion, as of June 23, 2025.

2. How much has WFC stock returned in the last five years?

In the last five years, Wells Fargo stock has returned close to 200%.

3. What is the price target for WFC stock?

The average WFC stock price target is $81.34.

4. Is Wells Fargo a Buy, Sell, or Hold?

Out of the 27 analysts covering Wells Fargo stock, 16 recommend a “Buy”.

5. Does WFC stock pay shareholders a dividend?

Yes, Wells Fargo is expected to pay shareholders an annual dividend of $1.66 per share in 2025.

6. How often does WFC pay a dividend?

Wells Fargo pays shareholders a quarterly dividend.

7. Is WFC stock overvalued?

Given consensus price targets, WFC stock trades at a discount of 5.60% in June 2025.

8. What is the P/E ratio for WFC stock?

The forward P/E ratio for WFC stock is 13x.

Want to Invest Like Warren Buffett, Joel Greenblatt, or Peter Lynch?

TIKR just published a special report breaking down 5 powerful stock screeners inspired by the exact strategies used by the world’s greatest investors.

In this report, you’ll discover:

- A Buffett-style screener for finding wide-moat compounders at fair prices

- Joel Greenblatt’s formula for high-return, low-risk stocks

- A Peter Lynch-inspired tool to surface fast-growing small caps before Wall Street catches on

Each screener is fully customizable on TIKR, so you can apply legendary investing strategies instantly. Whether you’re looking for long-term compounders or overlooked value plays, these screeners will save you hours and sharpen your edge.

This is your shortcut to proven investing frameworks, backed by real performance data.

Click here to sign up for TIKR and get this full report now, completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!